Response to consultation Paper on draft Guidelines on loan origination and monitoring.

Go back

In the paragraph 35.b - and to be added in Annex 1: credit granting criteria should guarantee a sufficient remaining income to allow, beside credit and contract reimbursement, to allow a decent life standard for the household.

In this respect, a KEY information to become compulsory in data collection is the household composition.

COFACE-Families Europe is also in favor to propose to include a “suitability check” of the type of credit proposed. It should be used to document the information and advice consumers should have received in the pre-contractual phase.

In paragraph 41., we recommend to insist on the process to only use quality proof information and “non-falsifiable” ones (not using data such as non-structured ones available on internet and social media).

In section 4.3.3

Institutions should demonstrate the way they are using data is compliant with GDPR and non-discrimination regulation. Principles such as “necessity” and “proportionality” should be operationally presented.

Paragraph 59: what is the rationale behind using the borrowers’ geographic location in the credit-decision making framework? This could also lead to discriminations based on “poor” neighbourhoods.

Paragraph 63.b.ii Does the principle of independence and minimisation of conflict of interest, which references economic interest, cover sales incentives?

Paragraph 76.f again talks about credit risk and creditworthiness as if they were similar processes. (See above) To this point, it should be added:

Ensure that creditworthiness and credit risk assessments do not lead to contradictory lending decisions".

To put it in other words: while a client may not have sufficient funds to repay a loan (negative creditworthiness assessment), the credit risk associated with lending at a certain interest rate may still be viable for the financial institution and in line with prudential regulation (creating a risk pool with borrowers of a similar profile and ensuring that overall, the borrowers which manage to repay cover for the loss of those who default)

Paragraph 76.g What is the definition of "independent"? For instance, would credit rating agencies be considered "independent"? For instance, is the Schufa score considered independent? It is key to define what an “independent” or “second opinion” looks like. From our perspective, it should be defined by law and supervised by public authorities. For instance, using a methodology for creditworthiness assessment which has been validated by a public institution using data which is also validated and approved by a public institution. Although the necessity for this “second opinion” would only be necessary if creditworthiness checks were made in a poor and unregulated manner by financial institutions. We would be in favour of simply making sure that creditworthiness checks are of high quality and independent from the start rather than relying on them as a “fall back” plan.

At the end of paragraph 76, add:

“Put in place preventive mechanisms for early detection of financial problems and set up a specific unit to explore solutions with customers in difficulty such as putting a loan reimbursement on hold, helping the customer with legal and administrative proceedings (obtaining social benefits, any benefits they may be entitled to given there difficult financial situation such as unemployment benefits etc), liaising and cooperating with not for profit or independent, recognized, high quality debt counselling and debt advice services.”"

First, given staff turn-over, it may not be possible to remunerate staff based on long-term criteria.

Second, does "quality" refer to complying with prudential requirements or does it refer to a specific number of non-performing contracts or defaults from borrowers? For instance, in pay day lending institutions, while their default rates are high, they still comply with prudential requirements.

The same question can be raised for point b, how is “credit quality” defined in that context?

In point c, what is the “best interest” of the consumer?

In order to make these recommendations or requirements operational, rigorous definitions need to be put in place to define when a credit is deemed of “high quality”. As was explained above, perhaps setting up a benchmark such as the level of NPL for certain products and how they compare to other products could be an objective way to measure credit quality. If the level of defaults for a specific product or in a specific institution is significantly higher than some defined benchmark, that would signal a “poor quality” product/credit.

Overall, the above requirements are very focused on credit risk and not so much on consumers and protecting their best interest (protecting them against loan sharks, payday lenders, debt collectors etc). More focus should be put on creditworthiness and what should be done to mitigate negative consequences of defaults and NPLs from the point of view of consumers."

It should also underline the necessary objective of creditworthiness assessment to guarantee a remaining income for a decent life considering the household composition (children or other members - parents...). Should this notion being the definition of “disposable income”, mentioned in the paragraph 98., we recommend to make this very clear in the guidelines. Actually, the 98. should not only refer to borrower’s income, but more appropriately, to borrower’s budget.

In this respect, paragraph 99. should also mention a ratio related to “remaining income for decent life” amount remaining per person in the borrower household. This is aligned with the content of paragraph 109. which mention “appropriate substantiation and consideration of the living expenses”, which does not mean anything if these expenditures are not connected with household composition (things might defer, if the amount of expenditures considered cover one adult or one adult and two children, for example). Using an automated analysis of inflow and outflow from the consumer's accounts via PSD2 may be relevant in this case, rather than trying to manually assess the expenditures of the borrower.

In this respect, 5.1.2. paragraph should include:

• employment should be understood more broadly as all type of professional activities. The current trend of moving away from traditional labour contracts (no end date) to temporary contracts should be taken into account as banks may consider that temporary contracts are more “risky” then other labour contracts, which would significantly impair many workers from accessing credit at decent conditions.

• household composition

• budget remaining amount (after incompressible expenditures such as contracts (rent - energy/water,...,+ financial commitments, liabilities) for decent life (food, health, education, mobility…)

• point f is too vague and should be removed as it is open ended, and could lead to abuses such as using non conventional data from social networks and other sources.

COFACE-Families Europe raise an important concern when we consider the paragraph 110. Financial institutions should indeed provision for difficult to predict and sudden events such as the swiss frank loans, and to insure against it, in order to enable consumers to keep reimbursing under the same conditions, instead of transferring all the risk to consumers and expecting them to repay (which also introduces prudential risks in the case of mass defaults). The hedging, in this case, would be purchasing special insurance products at the financial institutions’ level, and not count on hedging at the level of the consumer (for instance, counting on the increase in value of property to hedge the risk in case of default and liquidation).

But given the unpredictability of products in foreign currency, even with the proper hedging, COFACE-Families Europe considers foreign currency loans to go against any possibility to do a proper creditworthiness assessment. Indeed, such product might lead to a change in the total cost of the product that might not allow anymore the borrower to face his liabilities, even if his incomes remain unchanged.

Because of these circumstances, because of the major issues encountered by a large range of EU borrowers, we recommend a stronger wording, in which:

• the risk related to change in exchange rate is not only covered by the consumer but also by the credit provider;

• to guarantee a possible meaningful creditworthiness assessment, provisions in the credit contract should at list: mention maximum increase / decrease in “interest”, in “duration”, in “monthly repayment” (so this predefined scenarios can be included in the creditworthiness exercise and it should be document at the time of the agreement how the product fit the situation of the borrowers);

• these predefined scenarios can also be used to defined what can be the “worst case scenario” and present to the consumer the maximum costs is is exposed to if every circumstances when in the “bad” direction.

(these type of credit have been proposed in Belgium, so called “accordeon”, which bring not only “flexibility” but also “security”.

For paragraph 118, it could be more relevant to assess the consumers' saving capacity since this reflects his left over income after all current expenditure, and thus, without assuming that the consumer can compress" one or more current expenditures to service a loan in case of problems.

With regards to missed payments, this data should be treated very delicately. Missed payments may reflect many different situations: an unfortunate circumstance (forgetting to repay, missed correspondence or mail...), or a conflictual situation with a provider (for instance, an error in the amount asked to pay for utility bills and a consumer withholding payment until the problem is resolved, which may appear as a missed payment in the data, but is actually a problem of the provider).

On the 5.2.3., COFACE-Families Europe wonders if any general remark on the fact that consumer credit origination should not be made backed on “guarantee” but should rely on “creditworthiness” evidence. In this respect, proportionality in the requirement of guarantee is an important dimension to be kept under scrutiny.

In paragraph 117., In a way or another, in the guidelines, an invitation for credit provider to design and adjust their credit design to new circumstances (type, of jobs, incomes, …) to bring more agile and user friendly products is key."

Taken from the creditworthiness perspective, it is important to define how much of the current borrowers' savings capacity can be taken up by the reimbursement of a credit without creating a substantial risk for the consumer, especially in the case of a financial shock (loss of employment, health problem, divorce etc).

Also on p. 182, it is important to factor in the constraints set out in macroprudential policy, where this is the case. Several EU MS have put forward macroprudential policy tools1, some more binding than others, which restrict loan granting by setting limits on ratios such as debt-to-service ratio, loan-to-value, and on maturity. These Guidelines should reflect that credit decision is also bound to macroprudential measures (in those jurisdictions where such measures are in place).

On p. 183, the information on the key features of a loan being offered to the borrower should include APR as this indicator is deemed to reflect the actual cost of a loan and is fundamental to compare different proposals (as referred to both in the CCD and the MCD).

P 187.b mentions that creditors should take into account behavioural assumptions in determining cost of funding. This needs more clarification.

Paragraph 187.d: again, this is related to the point above on the illusion to hedge credit risk by pricing it in. Unfortunately, this has rather a negative snowball effect. In the case of a vulnerable consumer, increasing the price of a credit to protect against a potential default will only increase the risk of the vulnerable consumer of defaulting since even more of his/her disposable income will have to be dedicated to servicing the loan (see above for a detailed explanation).

Furthermore, one has to question whether financial service providers should even seek to recover debt on which a consumer has defaulted if the risk of default is priced in the credit. This sounds counter intuitive. It is as if an insurance company would ask the consumer to nevertheless pay for the risk that the consumer was insured against!

The point is that the requirements for valuation of immovable and movable property collateral might very artificial and dependent on macro-economic factors which are beyond the control of any individual actor and which create a systemic risk which no requirement can hedge against. It is not to say that there should be no rules or requirements, only that regulators should not expect these requirements to be an effective hedge against bigger macro-economic developments, which need to be addressed properly in subsequent work of EBA, other regulatory bodies and policy makers in general.

On par. 204 the reference should be to par. 200 (not 2000).

In general, in this section, there was no mention of prevention measures such as identifying consumers in financial difficulty before they default on their existing financial commitments and a dedicated unit which deals with helping consumers in distress.

Paragraph 263: These early warnings seem to apply mostly to professionals and not individual consumers. It would be good to add indicators such as a drop in the consumers' ability to save, or a lack of financial buffer (living paycheck to paycheck).

Paragraph 266: The plan should also include the write off of part or all of the debt. That should also be a part of the solution.

The current ideologically fuelled belief that debts should be considered unbreakable contracts should be reconsidered. Debt is an essential instrument for keeping our current economies afloat. By taking out loans, consumers are actually contributing to maintain aggregate demand at a high enough level to maintain economic growth and stability. In other words, the most important factor which determines whether or not consumers are able to repay their credit is whether other people keep borrowing during the life of their credit (reimbursement). In short, if people stop borrowing, the money supply shrinks, which cascades throughout the economy and leads to lower salaries, higher unemployment, lower investment, etc, which, down the line, undermines the ability of a higher percentage of people to repay their existing credit. See the works of economist Steve Keen. The insight above is not meant to encourage borrowing but to recognize the role that borrowing plays in the economy, and therefore recognize the risk that borrowers take. This means that if we recognize that consumer borrowing is directly linked with the overall health of the economy, then much more generous policies in terms of personal insolvency should be put in place.

While a binary decision to lend based on disposable income could restrict the provision of credit and therefore negatively affect the economy, this could force policy makers to reconsider the overall monetary system which is overly reliant on credit as a major driver for aggregate demand and in general, affecting the global supply of money (monetary mass). Other solutions include Modern Monetary Theory (which considers injecting money directly to individuals – helicopter money) or a form of Universal Basic Income.

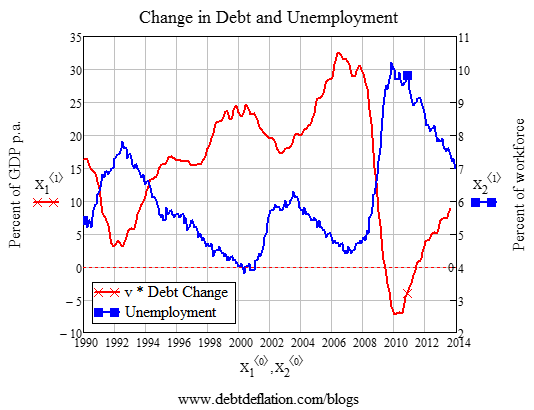

For more information: https://www.debtdeflation.com/blogs/2014/02/02/modeling-financial-instability/

Below, a graph showing the correlation (-0;92) between unemployment and change in how much credit is being lent out in the US.

Credit refinancing procedures (especially with mortgages) should be considered adequately. If the same strict standards are to be applied as they should with any entirely new credit or higher credit amount, too strict conditions could cause the borrower’s default instead of preventing it. Especially if consumers were able to repay their previous instalments before the refinancing, despite a lower assumed creditworthiness. This would as well be in line with the spirit of Article 28 of Directive 2014/17/ЕU (Mortgage Credit Directive).

In line with Article 28 of Directive 2014/17/EU, lenders should exercise reasonable forbearance and try to prevent credit contacts from becoming non-performing.

5. What are the respondents’ views on the requirements for governance for credit granting and monitoring (Section 4)?

In the paragraph 31. COFACE-Families Europe recommends to document as well in term on end-users situation (so to have an indicator of consumer at risk of over-indebtedness). EBA should in a second step elaborate a standardised set of common EU indicators (cf. paragraph 33. - “products and specific credit facilities” should benefit from an common EU typology).In the paragraph 35.b - and to be added in Annex 1: credit granting criteria should guarantee a sufficient remaining income to allow, beside credit and contract reimbursement, to allow a decent life standard for the household.

In this respect, a KEY information to become compulsory in data collection is the household composition.

COFACE-Families Europe is also in favor to propose to include a “suitability check” of the type of credit proposed. It should be used to document the information and advice consumers should have received in the pre-contractual phase.

In paragraph 41., we recommend to insist on the process to only use quality proof information and “non-falsifiable” ones (not using data such as non-structured ones available on internet and social media).

In section 4.3.3

Institutions should demonstrate the way they are using data is compliant with GDPR and non-discrimination regulation. Principles such as “necessity” and “proportionality” should be operationally presented.

Paragraph 59: what is the rationale behind using the borrowers’ geographic location in the credit-decision making framework? This could also lead to discriminations based on “poor” neighbourhoods.

Paragraph 63.b.ii Does the principle of independence and minimisation of conflict of interest, which references economic interest, cover sales incentives?

Paragraph 76.f again talks about credit risk and creditworthiness as if they were similar processes. (See above) To this point, it should be added:

Ensure that creditworthiness and credit risk assessments do not lead to contradictory lending decisions".

To put it in other words: while a client may not have sufficient funds to repay a loan (negative creditworthiness assessment), the credit risk associated with lending at a certain interest rate may still be viable for the financial institution and in line with prudential regulation (creating a risk pool with borrowers of a similar profile and ensuring that overall, the borrowers which manage to repay cover for the loss of those who default)

Paragraph 76.g What is the definition of "independent"? For instance, would credit rating agencies be considered "independent"? For instance, is the Schufa score considered independent? It is key to define what an “independent” or “second opinion” looks like. From our perspective, it should be defined by law and supervised by public authorities. For instance, using a methodology for creditworthiness assessment which has been validated by a public institution using data which is also validated and approved by a public institution. Although the necessity for this “second opinion” would only be necessary if creditworthiness checks were made in a poor and unregulated manner by financial institutions. We would be in favour of simply making sure that creditworthiness checks are of high quality and independent from the start rather than relying on them as a “fall back” plan.

At the end of paragraph 76, add:

“Put in place preventive mechanisms for early detection of financial problems and set up a specific unit to explore solutions with customers in difficulty such as putting a loan reimbursement on hold, helping the customer with legal and administrative proceedings (obtaining social benefits, any benefits they may be entitled to given there difficult financial situation such as unemployment benefits etc), liaising and cooperating with not for profit or independent, recognized, high quality debt counselling and debt advice services.”"

6. What are the respondent’s views on how the guidelines capture the role of the risk management function in credit granting process?

For paragraph 82.a, how would this work in practice? What do you consider as high quality"? This is too vague.First, given staff turn-over, it may not be possible to remunerate staff based on long-term criteria.

Second, does "quality" refer to complying with prudential requirements or does it refer to a specific number of non-performing contracts or defaults from borrowers? For instance, in pay day lending institutions, while their default rates are high, they still comply with prudential requirements.

The same question can be raised for point b, how is “credit quality” defined in that context?

In point c, what is the “best interest” of the consumer?

In order to make these recommendations or requirements operational, rigorous definitions need to be put in place to define when a credit is deemed of “high quality”. As was explained above, perhaps setting up a benchmark such as the level of NPL for certain products and how they compare to other products could be an objective way to measure credit quality. If the level of defaults for a specific product or in a specific institution is significantly higher than some defined benchmark, that would signal a “poor quality” product/credit.

Overall, the above requirements are very focused on credit risk and not so much on consumers and protecting their best interest (protecting them against loan sharks, payday lenders, debt collectors etc). More focus should be put on creditworthiness and what should be done to mitigate negative consequences of defaults and NPLs from the point of view of consumers."

7. What are the respondents’ views on the requirements for collection of information and documentation for the purposes of creditworthiness assessment (Section 5.1)?

The 5.1.1. section should include a more precise definition of the creditworthiness definition - it should refer more to household budget (incomes, contracts, liabilities, incompressible expenditures, remaining income for a decent level of life).It should also underline the necessary objective of creditworthiness assessment to guarantee a remaining income for a decent life considering the household composition (children or other members - parents...). Should this notion being the definition of “disposable income”, mentioned in the paragraph 98., we recommend to make this very clear in the guidelines. Actually, the 98. should not only refer to borrower’s income, but more appropriately, to borrower’s budget.

In this respect, paragraph 99. should also mention a ratio related to “remaining income for decent life” amount remaining per person in the borrower household. This is aligned with the content of paragraph 109. which mention “appropriate substantiation and consideration of the living expenses”, which does not mean anything if these expenditures are not connected with household composition (things might defer, if the amount of expenditures considered cover one adult or one adult and two children, for example). Using an automated analysis of inflow and outflow from the consumer's accounts via PSD2 may be relevant in this case, rather than trying to manually assess the expenditures of the borrower.

In this respect, 5.1.2. paragraph should include:

• employment should be understood more broadly as all type of professional activities. The current trend of moving away from traditional labour contracts (no end date) to temporary contracts should be taken into account as banks may consider that temporary contracts are more “risky” then other labour contracts, which would significantly impair many workers from accessing credit at decent conditions.

• household composition

• budget remaining amount (after incompressible expenditures such as contracts (rent - energy/water,...,+ financial commitments, liabilities) for decent life (food, health, education, mobility…)

• point f is too vague and should be removed as it is open ended, and could lead to abuses such as using non conventional data from social networks and other sources.

8. What are the respondents’ views on the requirements for assessment of borrower’s creditworthiness (Section 5.2)?

Some elements have already been mentioned in the response of question n°7.COFACE-Families Europe raise an important concern when we consider the paragraph 110. Financial institutions should indeed provision for difficult to predict and sudden events such as the swiss frank loans, and to insure against it, in order to enable consumers to keep reimbursing under the same conditions, instead of transferring all the risk to consumers and expecting them to repay (which also introduces prudential risks in the case of mass defaults). The hedging, in this case, would be purchasing special insurance products at the financial institutions’ level, and not count on hedging at the level of the consumer (for instance, counting on the increase in value of property to hedge the risk in case of default and liquidation).

But given the unpredictability of products in foreign currency, even with the proper hedging, COFACE-Families Europe considers foreign currency loans to go against any possibility to do a proper creditworthiness assessment. Indeed, such product might lead to a change in the total cost of the product that might not allow anymore the borrower to face his liabilities, even if his incomes remain unchanged.

Because of these circumstances, because of the major issues encountered by a large range of EU borrowers, we recommend a stronger wording, in which:

• the risk related to change in exchange rate is not only covered by the consumer but also by the credit provider;

• to guarantee a possible meaningful creditworthiness assessment, provisions in the credit contract should at list: mention maximum increase / decrease in “interest”, in “duration”, in “monthly repayment” (so this predefined scenarios can be included in the creditworthiness exercise and it should be document at the time of the agreement how the product fit the situation of the borrowers);

• these predefined scenarios can also be used to defined what can be the “worst case scenario” and present to the consumer the maximum costs is is exposed to if every circumstances when in the “bad” direction.

(these type of credit have been proposed in Belgium, so called “accordeon”, which bring not only “flexibility” but also “security”.

For paragraph 118, it could be more relevant to assess the consumers' saving capacity since this reflects his left over income after all current expenditure, and thus, without assuming that the consumer can compress" one or more current expenditures to service a loan in case of problems.

With regards to missed payments, this data should be treated very delicately. Missed payments may reflect many different situations: an unfortunate circumstance (forgetting to repay, missed correspondence or mail...), or a conflictual situation with a provider (for instance, an error in the amount asked to pay for utility bills and a consumer withholding payment until the problem is resolved, which may appear as a missed payment in the data, but is actually a problem of the provider).

On the 5.2.3., COFACE-Families Europe wonders if any general remark on the fact that consumer credit origination should not be made backed on “guarantee” but should rely on “creditworthiness” evidence. In this respect, proportionality in the requirement of guarantee is an important dimension to be kept under scrutiny.

In paragraph 117., In a way or another, in the guidelines, an invitation for credit provider to design and adjust their credit design to new circumstances (type, of jobs, incomes, …) to bring more agile and user friendly products is key."

9. What are the respondents’ views on the scope of the asset classes and products covered in loan origination procedures (Section 5)?

Paragraph 182: There needs to be a clarification in the credit decision making process between acceptance and refusal thresholds, linked to default rates. For instance, at which rate of default inside a specific risk pool does credit become predatory lending or irresponsible lending? For instance, if inside a risk pool over 20% of consumers are considered to likely default on their loan, is this considered predatory lending?Taken from the creditworthiness perspective, it is important to define how much of the current borrowers' savings capacity can be taken up by the reimbursement of a credit without creating a substantial risk for the consumer, especially in the case of a financial shock (loss of employment, health problem, divorce etc).

Also on p. 182, it is important to factor in the constraints set out in macroprudential policy, where this is the case. Several EU MS have put forward macroprudential policy tools1, some more binding than others, which restrict loan granting by setting limits on ratios such as debt-to-service ratio, loan-to-value, and on maturity. These Guidelines should reflect that credit decision is also bound to macroprudential measures (in those jurisdictions where such measures are in place).

On p. 183, the information on the key features of a loan being offered to the borrower should include APR as this indicator is deemed to reflect the actual cost of a loan and is fundamental to compare different proposals (as referred to both in the CCD and the MCD).

10. What are the respondents’ views on the requirements for loan pricing (Section 6)?

Pricing of consumer credit should forbid (by design) any risk of discrimination. Pricing policies should be documented in such a way it allows a compliance check by the relevant authority.P 187.b mentions that creditors should take into account behavioural assumptions in determining cost of funding. This needs more clarification.

Paragraph 187.d: again, this is related to the point above on the illusion to hedge credit risk by pricing it in. Unfortunately, this has rather a negative snowball effect. In the case of a vulnerable consumer, increasing the price of a credit to protect against a potential default will only increase the risk of the vulnerable consumer of defaulting since even more of his/her disposable income will have to be dedicated to servicing the loan (see above for a detailed explanation).

Furthermore, one has to question whether financial service providers should even seek to recover debt on which a consumer has defaulted if the risk of default is priced in the credit. This sounds counter intuitive. It is as if an insurance company would ask the consumer to nevertheless pay for the risk that the consumer was insured against!

11. What are the respondents’ views on the requirements for valuation of immovable and movable property collateral (Section 7)?

All of these provisions in this section have a limit: that of pricing in the effect of the current experimental monetary policy (QE) which artificially inflates the prices of real estate and the stock market, completely disconnected from fundamentals, and the impact it may have in case of a massive recession or collapse of the “everything bubble”, which refers to the inflation of several assets among which, mostly, the price of stocks (thanks to massive corporate buybacks facilitated by QE) and the inflation in the price of (existing) property and real estate. Both of these assets are completely disconnected from economic fundamentals (for instance, stock prices relative to company earnings), and any reversal in the policy of central banks would precipitate their depreciation, triggering a massive crisis (the alternative being a “Japanification” of Europe, aka, 30 years of economic stagnation with base central bank interest rates at negative or 0%)The point is that the requirements for valuation of immovable and movable property collateral might very artificial and dependent on macro-economic factors which are beyond the control of any individual actor and which create a systemic risk which no requirement can hedge against. It is not to say that there should be no rules or requirements, only that regulators should not expect these requirements to be an effective hedge against bigger macro-economic developments, which need to be addressed properly in subsequent work of EBA, other regulatory bodies and policy makers in general.

On par. 204 the reference should be to par. 200 (not 2000).

12. What are the respondents’ views on the proposed requirements on monitoring framework (Section 8)?

Paragraph 229.e The monitoring of credit risk and especially NPLs across comparable consumer segments could be a basis for defining predatory lending. If any financial service provider has a NPL ratio which negatively deviates significantly (from a statistical point of view) from its competitors (average), then their lending practices should be closely examined/investigated and considered inappropriate.In general, in this section, there was no mention of prevention measures such as identifying consumers in financial difficulty before they default on their existing financial commitments and a dedicated unit which deals with helping consumers in distress.

Paragraph 263: These early warnings seem to apply mostly to professionals and not individual consumers. It would be good to add indicators such as a drop in the consumers' ability to save, or a lack of financial buffer (living paycheck to paycheck).

Paragraph 266: The plan should also include the write off of part or all of the debt. That should also be a part of the solution.

The current ideologically fuelled belief that debts should be considered unbreakable contracts should be reconsidered. Debt is an essential instrument for keeping our current economies afloat. By taking out loans, consumers are actually contributing to maintain aggregate demand at a high enough level to maintain economic growth and stability. In other words, the most important factor which determines whether or not consumers are able to repay their credit is whether other people keep borrowing during the life of their credit (reimbursement). In short, if people stop borrowing, the money supply shrinks, which cascades throughout the economy and leads to lower salaries, higher unemployment, lower investment, etc, which, down the line, undermines the ability of a higher percentage of people to repay their existing credit. See the works of economist Steve Keen. The insight above is not meant to encourage borrowing but to recognize the role that borrowing plays in the economy, and therefore recognize the risk that borrowers take. This means that if we recognize that consumer borrowing is directly linked with the overall health of the economy, then much more generous policies in terms of personal insolvency should be put in place.

While a binary decision to lend based on disposable income could restrict the provision of credit and therefore negatively affect the economy, this could force policy makers to reconsider the overall monetary system which is overly reliant on credit as a major driver for aggregate demand and in general, affecting the global supply of money (monetary mass). Other solutions include Modern Monetary Theory (which considers injecting money directly to individuals – helicopter money) or a form of Universal Basic Income.

For more information: https://www.debtdeflation.com/blogs/2014/02/02/modeling-financial-instability/

Below, a graph showing the correlation (-0;92) between unemployment and change in how much credit is being lent out in the US.

Credit refinancing procedures (especially with mortgages) should be considered adequately. If the same strict standards are to be applied as they should with any entirely new credit or higher credit amount, too strict conditions could cause the borrower’s default instead of preventing it. Especially if consumers were able to repay their previous instalments before the refinancing, despite a lower assumed creditworthiness. This would as well be in line with the spirit of Article 28 of Directive 2014/17/ЕU (Mortgage Credit Directive).

In line with Article 28 of Directive 2014/17/EU, lenders should exercise reasonable forbearance and try to prevent credit contacts from becoming non-performing.

Upload files

graph.png

(9.3 KB)

{kind=link}