Part I – Achievements of the year

Achieving the 2024 core priorities

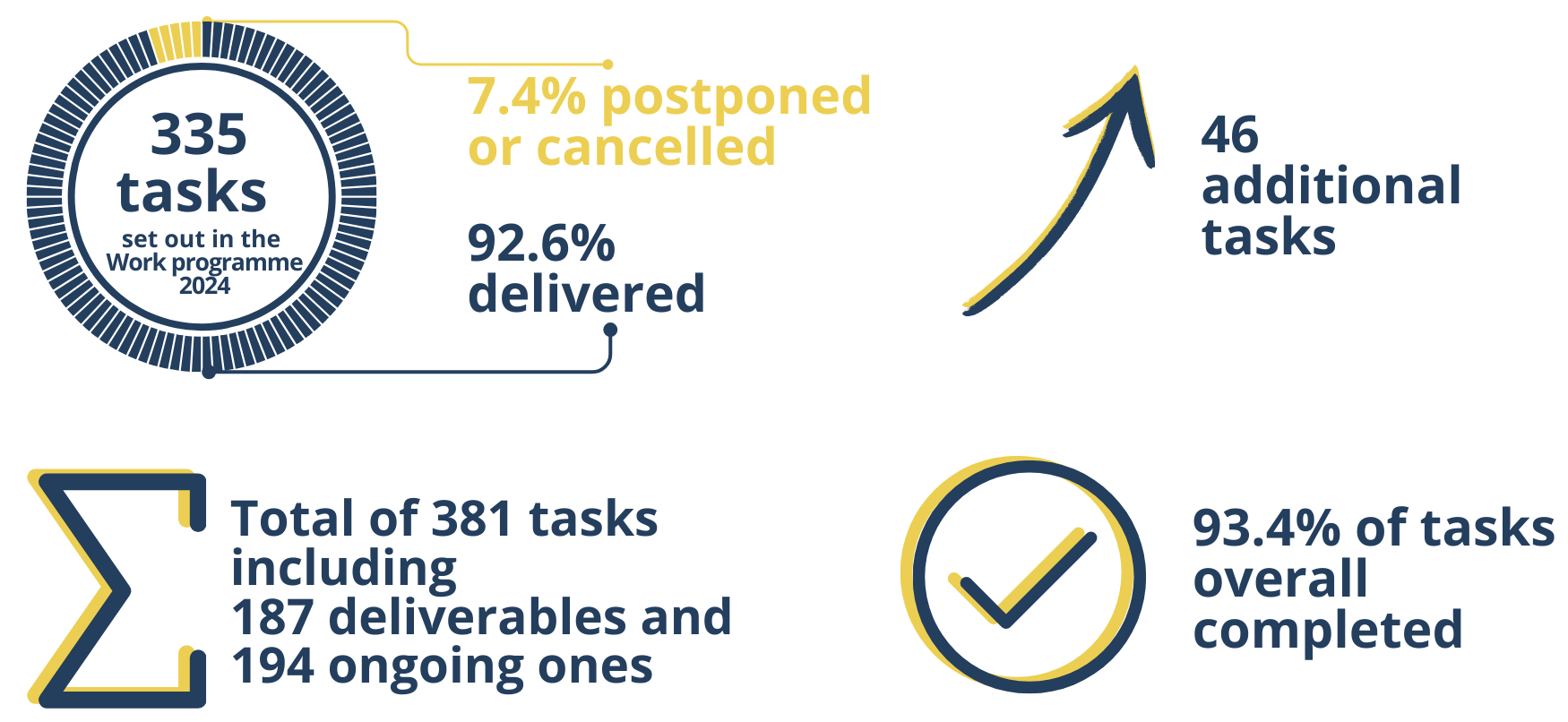

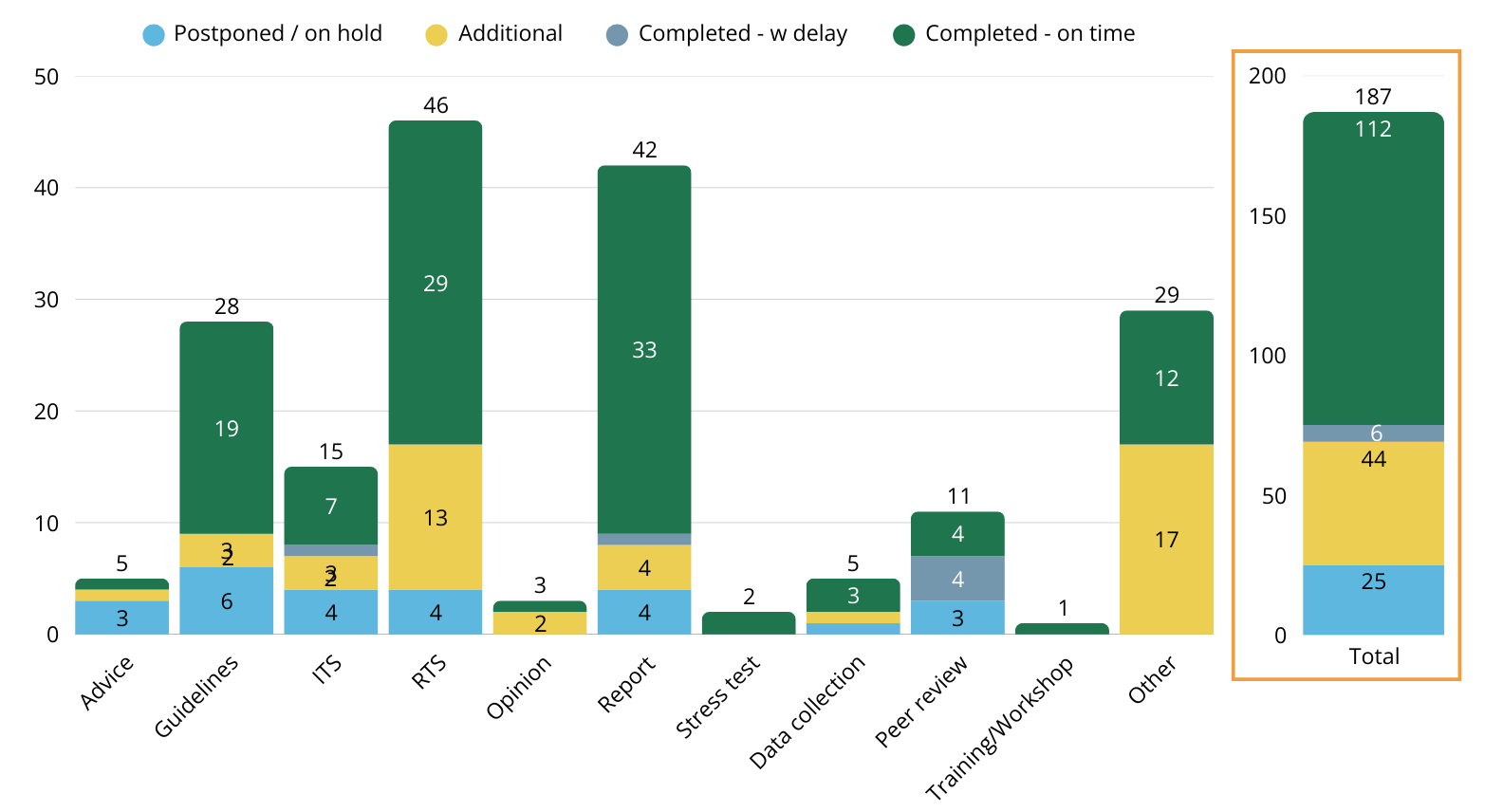

In 2024, the European Banking Authority (EBA) completed 93% of the tasks outlined in its 2024 Work Programme (WP). Similar to the previous year, a small number of tasks were delayed or postponed, primarily because additional tasks were required that were not initially anticipated.

The EBA’s deliverables included technical standards (regulatory technical standards (RTS) and implementing technical standards (ITS)), guidelines, responses to calls for advice, opinions, reports and peer reviews, reflecting the institution’s role within the European Union’s regulatory framework.

The sections below break down the EBA’s main tasks and deliverables over the past 12 months in further detail, adhering to the priorities and structure of the 2024 WP. They include tables and visuals illustrating or detailing how the EBA executed the WP.

Overall, the achievements section offers insights into the scope of the EBA’s activities, stressing an unwavering commitment to its regulatory responsibilities and its role in ensuring stability and integrity within the European banking sector.

NB: These deliverables do not include tasks that are ongoing in nature.

Implementing Basel framework in the EU and enhancing the Single Rulebook

The EBA focused on its contribution to the timely and faithful implementation of the Basel III reforms in the EU to ensure banks can withstand future crises and to preserve a proper functioning of the European and global financial systems. This will underpin a strong regulatory framework, relying on more risk-sensitive approaches for determining capital requirements and also addressing previous shortcomings. At the same time, this work contributes to enhancing the Single Rulebook in banking and financial regulation.

Whereas the banking package, i.e. the Capital Requirements Regulation (CRR) III and Capital Requirements Directive (CRD) VI, entered into force in July 2024, in December 2023 the EBA published a roadmap detailing its approach to, and sequencing of, its work on the some 140 mandates in the different areas, in line with the legal deadlines set out by the co-legislators.

Overall, the EBA has so far issued Consultation Papers (CPs) on 24 mandates of the banking package, delivered on 10 mandates and delivered 8% of the planning foreseen under the roadmap.

Facilitating Basel III implementation in Europe

In accordance with Phase 1 of the roadmap, work was carried out in the area of credit risk with the publication of five CPs on the mandates, aimed at implementing critical elements of the standardised approach (SA) and the review of targeted elements of the internal ratings based (IRB) framework (review of the RTS on the categorisation of model changes and of the ITS on joint decision processes). In addition, the EBA published a report on the treatment of credit insurance in the prudential framework.

In the area of operational risk, work focused on preparing the CP on mandates relating to the calculation of the business indicator (BI) and its sub-items, mapping the BI to FINREP, as well as the adjustments to the BI following mergers, acquisitions and disposals. Further work included developing a CP on the taxonomy for operational risk losses, together with two mandates related to the management of operational risk losses. In parallel, the reporting framework for the new requirements concerning operational risk in CRR III was developed.

Many of the mandates on market risk, covered in a batch of CPs issued in 2023 and in 2024, related to aspects of the FRTB that are essential for sound implementation, or that have a material impact on own funds requirements, were also completed. As a result of the Commission’s decision to postpone the application of the market risk framework in the EU in order to preserve an international level playing field, the EBA published a no-action letter on the boundary between the banking book and the trading book to help address technical questions and issues arising from the postponement.

Anna Gardella – Single market accessIn 2024, I led the team in charge of projects relating to market access from third countries and from within the EU. These projects focused, on the one hand, on the implementation of the regime applicable to third country groups operating in the EU and, on the other hand, on the execution of material transactions, such as mergers, acquisitions and divisions. I coordinated the development of the Level 2 and Level 3 mandates with a view to ensuring consistency of the policy approach of the various interconnected projects, as well as the coherent interpretation of the freshly adopted CRD6. This required a great deal of interaction with several stakeholders, including the European Commission, ESMA, EIOPA, financial stakeholders, as well as internally with EBA experts. The projects relating to market access from third countries posed several challenges in ensuring consistency of the policy stance, as well as a coherent approach vis-à-vis the operation of third country groups in the EU. The new regime on third country branches is the first EU-led exercise in an area so far left exclusively to national level. Hence the need for clarity on the identification of what pertains to the general EU approach and what is still left within the national sphere. As a team with a variety of expertise, we managed to address all these challenges and complexities and to promote a single policy view thanks to transparent dialogue with our stakeholders, effective planning and organisation of the work. I am proud of the pillars we have set in the development of this new area of regulation that will contribute to shaping a single approach at EU level for third country groups operating in the EU. |

The EBA continued its contribution to the Commission’s renewed Sustainable Finance Strategy, announced in July 2021 as part of the European Green Deal, and paid particular attention to aspects relating to environmental, social and governance (ESG) matters reflected in its work, in accordance with the roadmap on sustainable finance published in December 2022.

Contributions in this field include the following: the EBA’s final report on greenwashing, in response to a request from the Commission and produced in coordination with the other ESAs – the report also provides recommendations to institutions, supervisors and policymakers; a joint ESAs opinion on the review of the SDFR in which the ESAs call for a coherent, sustainable finance framework that caters for both the green transition and for enhanced consumer protection, taking into account the lessons learned from the functioning of the SFDR; as well as under the same regulation, the annual joint Article 18 report focusing on principal adverse impact (PAI) disclosures.

In addition, efforts were devoted to addressing ESG-related regulatory mandates conferred on EBA in the banking package. In this context, the authority issued guidelines on the management of ESG risks in early January 2025, which set out harmonised guidance to help EU banking institutions identify, measure, manage and monitor ESG risks, including for designing their transition plans to ensure their resilience in the short, medium and long term.

At the same time, the EBA published a CP on the draft guidelines on ESG scenario analysis in January 2025, which also aims to contribute to this field, albeit with a focus on institutions. The proposed guidelines set out expectations for institutions when adopting forward-looking approaches and incorporating the use of scenario analysis as part of their management framework to test financial and business model resilience to the negative impacts of ESG factors. These proposals complement the EBA guidelines on the management of ESG risks, published at the same time, and further deliver some of the elements set out in the EBA Roadmap on Sustainable Finance and as part of the EBA’s planned actions for the implementation of the EU banking package.

With regards to the work on the prudential treatment of exposures subject to ESG risks, the focus was on data availability and the feasibility of adopting a standard methodology for ESG exposures with a corresponding report (published with a short delay in Q1 2025). Work has also started on incorporating ESG aspects into the disclosure and supervisory reporting that is being prepared as part of step 2 of implementing CRR III/CRD VI changes.

Following a first batch of CPs issued in 2023, the mandates relating to step 1 of implementing CRR III/CRD VI changes in the supervisory reporting framework and in the disclosure requirements for banks were finalised towards the end of Q2 2024 – and for investment firms in Q4 – thereby allowing early implementation of these elements and ensuring that market participants and supervisors have access to the information they need to assess institutions for their respective purposes.

In the context of the banking package, the EBA has taken into consideration the recommendations of the Advisory Committee on Proportionality (ACP) to ensure that the regulatory products and guidance it delivers are drafted in a way that is consistent with and uphold the principle of proportionality, and reduce compliance costs without damaging the prudential objectives. The ACP viewed that the development of RTS, ITS, GL and Q&As could reflect proportionality by (i) setting different scopes, (ii) aiming for less complex regulation, (iii) using easy language and (iv) having the implementation impact on small and medium-sized banks in mind. In particular, the ACP recommended that the EBA further address proportionality in the credit risk framework, given its relevance for banks’ balance sheets regardless of size, range of activity and level of complexity.

The ACP also recommended that proportionality considerations remain at the core of the impact assessments that accompany the regulatory products and guidance. In the area of securitisation and covered bonds, the ESAs provided a report on the securitisation framework under Article 44 of the Securitisation Regulation (SECR). Prioritising this request led to the deprioritisation of three monitoring reports. The EBA has also started working on a call for advice from the Commission to support the revision on the performance of the EU covered bonds framework, mandated in Article 31 of the Covered Bonds Directive, and expects to deliver it in Q2 2025.

Roberta de Filippis – Securitisation and covered bondsIn 2024, I led a talented team in reviewing the EU securitisation and covered bond frameworks. Our work required extensive coordination with various stakeholders, including the European Supervisory Authorities and the European Commission. Building on the EBA’s previous efforts, we focused on harmonising and strengthening the securitisation market to advance the Saving and Investment Union. Regular meetings with ESMA and EIOPA colleagues were crucial for keeping everyone informed and engaged. In 2024, I also oversaw the comprehensive review of the EU covered bond framework in response to the Commission’s Call for Advice. This required effective communication and continuous cooperation with covered bond supervisors from all EU Member States and various industry stakeholders. Internal coordination with other EBA units was also key to ensuring a consistent approach on ESG-related topics. Reflecting on 2024, I am proud of our achievements. Leading the securitisation and covered bond team through several transitions and unexpected challenges was both demanding and rewarding. The cooperative environment and efficient coordination enabled us to adapt and thrive, preparing us for future challenges and successes. |

Work continued to respond to a call for advice for the purposes of a second benchmarking of national loan enforcement frameworks (insolvency benchmarking). The EBA launched an update of the first benchmarking exercise in 2020 to publish a report in 2025. This allowed for a considerable reduction in the burden for euro area banks, as the related ad hoc data collection was limited to data needs not covered by the AnaCredit dataset.

In the area of investment firms, the EBA focused on the remaining mandates stemming from the new regulatory regime set out in the IFR/IFD. This led to the publication of guidelines on the application of the group capital test, for investment firms setting harmonised criteria to address the observed diversity in the application of such tests across the EU. Progress was made on the response to the European Commission’s call for advice, with a discussion paper published in June 2024 to gather stakeholder feedback and ad hoc data collection. The feedback will inform the response that the EBA and ESMA intend to provide jointly, and which will include a broad assessment of the provisions of the IFR and IFD and their interaction with other regulations.

Reaping the benefits of the Single Rule Book

The EBA updated the list of Common Equity Tier 1 (CET 1) instruments in December 2024, addressing bank liabilities. It also monitored developments in capital and capital issuances (Additional Tier 1 (AT1), Tier 2 and total loss-absorbing capacity /minimum requirement for own funds and eligible liabilities (TLAC/MREL) instruments), and published its monitoring report in June 2024, with new guidance on the prudential valuation of non-CET1 instruments and other aspects related to the terms and conditions of issuances.

Furthermore, the EBA continued its work on implementing the EBA opinion on legacy instruments (including in the context of the CRR II grandfathering provisions) and, after providing guidance on one specific issuance of legacy Tier 2 instruments in January 2024, addressed a further case in December 2024.

As a result of reviewing the stacking orders of capital, leverage and MREL/TLAC requirements and related capital buffers, in July 2024 we published a report describing the role of regulatory stacks, summarising the differences between the EU, UK and US frameworks, and highlighting institutions’ practices on management buffers. The findings contributed to other EBA regulatory products, such as the mandate on the interplay between the output floor and Pillar 2 (Article 104a(7) CRD6), which was also the topic of an EBA opinion published in January 2025, as well as the updated supervisory review and evaluation process (SREP) guidelines planned for 2025.

A report on liquidity measures published in December 2024 set out the findings of the monitoring and evaluation of the liquidity coverage requirements currently in place in the EU. It highlighted that, between June 2023 and June 2024, EU banks’ liquidity coverage ratio (LCR) increased by three percentage points to reach 167%, and also reveals changes in the composition of banks’ funding deposits, while banks’ holdings of liquid assets steadily increased.

At the beginning of 2024, the EBA published a report about specific aspects of the net stable funding ratio (NSFR) framework. The report provides an evaluation of the materiality of the specific items analysed, as well as an assessment of the impact of possible changes to the current prudential treatment. All analysed items appear to have limited materiality in terms of contribution to the total required stable funding, and this situation is confirmed for major as well as smaller banks. A change in the regulatory treatment of such items is not expected to have material effects on institutions but would generate compliance costs. Moreover, the current treatment appears to be aligned with other jurisdictions, which means that any changes would jeopardise the level playing field. The EBA therefore concluded that no changes are needed to the current legislation.

As part of Pillar 2 work, the EBA monitored the impact of the interest rate environment on own funds and eligible liabilities aspects, as set out in its heatmap following scrutiny of how the interest rate risk in the banking book (IRRBB) standards are being implemented in the EU. The heatmap published in January 2024 set out policy areas that would be subject to further scrutiny, and corresponding actions in the short to medium and long term. An initial follow-up report reflecting on the short/medium term objectives of the heatmap was prepared during 2024 and published in early February 2025.

The EBA continued to monitor implementation of the GL for the SREP, with particular consideration of the recommendations made by the ACP. This work also relied on the EBA’s ongoing assessment of supervisory practices through the European Supervisory Examination Programme (ESEP) and the monitoring of its implementation, and through participation in supervisory colleges. The report on the convergence of supervisory practices, published in July, shows that there is still room for further consistency in the identification and treatment of risks covered by Pillar 2 requirements across the EU, while supervisory college monitoring confirmed that the annual college cycle is functioning well.

As in previous years, the authority continued its benchmarking activities in both credit and market risk models (inclusive of IFRS 9-related considerations) in order to support Competent Authorities (CAs) in assessing the internal approaches used for the calculation of own funds requirements and for remuneration practices.

In the area of governance, the ESAs (EBA, EIOPA, ESMA) published joint guidelines on the system for exchanging information relevant to fit and proper assessments, with a view to enhancing the information exchange between supervisory authorities in a dedicated system across different parts of the financial sector.

On the topic of remuneration, in July the authority published its report on the application of gender-neutral remuneration policies by institutions subject to the CRD and the IFD, based on information collected from institutions, investment firms and CAs. The report shows that the industry faces no major hurdles in adopting and implementing gender-neutral remuneration policies, but that some entities lag behind.

Separately, in July 2024, the EBA published a report on the application of derogations from the requirements on deferral and payout in instruments under the CRD. This work aimed to assess the implementation and application of derogations within the EU, their impact on costs, the risk alignment of variable remuneration vis-à-vis the risk profile of the institution, and their impact on the ability to recruit and retain staff.

The annual report on high earners, based on 2022 data (covering entities subject to both CRD and IFD), was published in April 2024 and the report based on 2023 data was published in December 2024. The reports show an increase in the number of individuals working for EU banks and investment firms who received remuneration of more than EUR 1 million between 2021 and 2022. This increase is linked to the overall good performance of institutions, with the expansion of business and salaries adjusted for inflation. Later on, in 2023, the number of high earners remained stable overall, with an increase in high earners in banking and a decrease in high earners in investment firms. These changes were mainly caused by the more volatile business model of investment firms and reduced profitability in 2023 compared to 2022, while banks, on average, continued to perform well.

In 2024, the EBA simplified its regular annual report on high earners’ remuneration into a dashboard to visualise data in a more appealing way for interested stakeholders.

Figure 4: Number of high earners (data for 2023) by Member State and payment bracket of one million euros for institutions and investment firms

In May 2024, the EBA received a mandate from the Commission to each year develop a set of indicators about the market share of non-EU entities operating in the EU banking sector and the concentration of their business models in specific countries or sectors of activity. The mandate also requires the EBA to analyse EU banks’ asset and liability exposures in foreign currencies. In response to the second part of the mandate, the EBA delivered a report in December 2024 analysing EU banks’ funding structure, their reliance on foreign (significant) currencies for funding, and the breakdown of EU banks’ exposures by domestic and foreign currency.

KPIs

| Indicator | Weight | Short description | Target | Achievement | |

|---|---|---|---|---|---|

| A | Number of technical standards, guidelines, reports delivered (Output) | 80% | Number of technical standards, guidelines and reports, most including analytical impact assessments, delivered on time and stemming from implementation of the CRD VI / CRR III / BRRD III | 80% | 81% |

| B | Number of technical standards, guidelines, reports delivered – ESG (Output) | 20% | Number of ESG-related technical standards, guidelines and responses to CfA, most including analytical impact assessments, stemming from the mandates in the EU regulations and directives and from the renewed Sustainable Finance Strategy of the Commission delivered on time. Source: Annual activity report | 80% | 100% |

Monitoring financial stability and sustainability in a context of increased interest rates and uncertainty

Within this priority, the EBA placed increased focus on the impact of slow growth and high interest rates on the real economy in general, and on the banking sector in particular, in a context of inflationary pressures and against the background of unstable geopolitical and economic circumstances (see Section Work on proportionality).

Findings from the EBA’s risk assessment work were reflected in deliverables such as the quarterly risk dashboard and the joint committee (JC) spring and autumn risk presentations, as well as the JC report on risks and vulnerabilities. Starting from 2024, the EBA evolved its annual Risk Assessment Report into a spring and an autumn edition, with the latter linked to the publication of the results of the 2024 EU-wide transparency exercise (discussed below).

The RAR is complemented by the regular MREL monitoring conducted by the EBA and publicised in the form of a dashboard summarising the state of play in resolution planning for all banks with a resolution strategy in the EU, stating the level of MREL requirement, the level of resources and resulting shortfalls and roll-over needs.

The introduction of top-down elements for NFCI in the previous exercise helped to shape the approach and methodology for the 2025 exercise. This gave rise, in July 2024, to an informal consultation on the draft methodology, templates and guidance for the 2025 EU-wide stress test, with important changes worthy of note, namely the integration of the Capital Requirements Regulation (CRR3), the Commission’s announcement to postpone the application date of the fundamental review of the trading book (FRTB), the centralisation of net interest income (NII) projections, but also advancements in the market risk methodology to increase risk sensitivity. Expanded geographical reach and the incorporation of proportionality features aim to boost efficiency while ensuring the relevance and transparency of the results, with the latter addressing the recommendations of the ACP.

Drawing on the feedback received, the EBA then proceeded to publish the final methodology, draft templates and template guidance for the 2025 EU-wide stress test, along with the milestone dates for the exercise in November 2024.

In addition to the work on the regular stress test exercise, the EBA undertook a one-off Fit-for-55 climate risk scenario analysis jointly with ESMA, EIOPA, the ECB and the ESRB, the results of which were published in November 2024. The exercise, which is part of mandates received under the European Commission’s Renewed Sustainable Finance Strategy, was aimed at assessing the resilience of the financial sector in line with the Fit-for-55 package, and to gain insights into the capacity of the financial system to support the transition to a lower carbon economy under stress conditions.

Scenarios of the Fit-for-55 climate stress testThe climate stress test was conducted against three scenarios developed by the European Systemic Risk Board (ESRB), with the support of the ECB. The scenarios incorporated transition risks as well as macroeconomic factors, based on the assumption that the Fit-for-55 package is implemented as planned.

The results of the exercise show that estimated losses stemming from a ‘Run-on-Brown’ scenario have limited impact on the EU financial system. Over the 8-year horizon, total first-round losses stand at between 5.2% and 6.7% of starting point exposures in each sector. The second-round losses are mostly relevant for investment funds, and amount to 11.2% of starting point exposures. Moreover, the interaction of adverse macro-financial developments with transition risk factors could disrupt the evolving transition and substantially increase financial institutions’ losses, thereby impairing their financing capacity. This was assessed in the second adverse scenario where the ‘Run-on-Brown’ shocks are coupled with adverse macroeconomic conditions. Under this scenario, the first-round losses registered by banks, insurers, occupational pension funds and investment funds stood at between 10.9% and 21.5%, depending on the sector. Although sizeable, the impact of these losses on financial institutions’ capital appeared to be mitigated by factors such as banks’ income, insurers’ and occupational pension funds’ liabilities, and cash holdings by investment funds that were not included in the assessment. |

In addition, the EBA has been working on incorporating climate-related risks into the EU-wide stress test in order to address the mandate in our founding regulation (Articles 23 and 32). A proposal was presented at the BoS meeting in December 2024, receiving support from the members.

The proposal outlines the EBA strategy, and distinguishes between a short-term module to assess capital adequacy and a long-term module to evaluate banks’ business model resilience, leveraging scenario analysis. According to this strategy, the incorporation of climate risks into the EU-wide stress-testing framework should be gradual, starting with a partial integration (‘combined approach’) in 2027, with more climate risk-related elements being added in subsequent stress tests. The combined approach will leverage the processes and infrastructure (e.g. timeline, FAQs, data collection and data quality checks) and some core methodological assumptions (e.g. static balance sheet, three-year time horizon) of EU-wide stress test, allowing for economies of scale and reducing the burden, both for banks and for supervisors. However, a clear separation between the results of the climate stress test and the results of the EU-wide stress test should be ensured, at least for the first application, for communication and supervisory action purposes.

Following the guidance provided by the BoS Members in December, work in the coming months will focus on developing concrete proposals for the implementation of the combined approach, while starting to discuss the possible high-level framework for the long-term module. Efforts will be made to ensure adequate coverage and assessment of physical risks (including their acute dimension), in addition to transition risks, for instance through the development of ad hoc scenarios. Efforts will also be made to ensure the principle of proportionality is included, as well as promoting alignment with the EU-wide stress test technical framework as far as possible.

KPIs

| Indicator | Weight | Short description | Target | Achievement | |

|---|---|---|---|---|---|

| A | Achievement of milestones ahead of the upgrade of ST methodology and development of a hybrid model (Output) | 50% | 1. Approval of the revised EU-wide stress test framework by Q1 2024 2. Design of the new ST methodology by end of 2024 3. Implementation of the revised EU-wide stress test framework for the 2025 exercise | 70% | 100% |

| B | Development and execution of a one-off and regular climate stress test (Output) | 50% | 1. Development of a one-off climate stress test and regular climate stress test 2. Implementation of one-off climate stress test 3. Implementation of regular climate stress test | 70% | 100% |

Source of information KPI A, KPI B: EBA WP monitoring tool and publications.

Providing a data infrastructure at the service of stakeholders

The EBA continued implementing its data strategy to improve the way regulatory data are acquired, compiled, used and disseminated to relevant stakeholders, thereby strengthening analytical capabilities. Its EUCLID platform enables data flows between diverse endpoints and provides access to high-quality, curated data and insights to internal and external stakeholders by employing advanced technical capabilities, with the objective of fostering the ingestion and dissemination of critical data assets, insights and analytics policies, as well as implementing the Pillar 3 data hub requested by the Level 1 legislation. In the last quarter of 2024, planning started for a 2025 review of the EBA’s data strategy, keeping in mind the 2026–2028 horizon and a close alignment with the EBA’s ICT Strategy for the same period.

Table 1: EUCLID in numbers

| How many | Data from | Reporting areas (up to EBA DPM v3.5) | |

| All EU/EEA credit institutions | ~4 400 | Q4 2020 | COREP (solvency, large exposures, liquidity, leverage ratio, fundamental review of the trading book, supervisory benchmarking of internal models, asset) |

| All EU/EEA banking groups | >500 | Q4 2020 | |

| Largest credit institutions or banking groups | >160 | Q1 2014* | Encumbrance, interest rate risk in the banking book, FINREP (IFRS9, national GAAP), Funding Plans, Environmental, Social and Governance, Resolution (Planning, MREL Decisions, MREL/TLAC), Global Systemically Important Institutions, Remunerations (High Earners, Benchmarking, Higher Ratio, Gender Pay Gap and Diversity Benchmarking) |

| All EU/EEA Investment firms | >2 300 | Q3 2021 | Investment Firms (CLASS2, CLASS3, GroupTest), COREP (solvency, large exposures, liquidity, leverage ratio, fundamental review of the trading book, supervisory benchmarking of internal models, asset encumbrance, interest rate risk in the banking book), FINREP (IFRS9, national GAAP), Remuneration (High Earners, Benchmarking, Higher Ratio, Gender Pay Gap and Diversity Benchmarking), Resolution** (Planning, MREL Decisions, MREL/TLAC) |

| All EU/EEA Investment firms’ groups | >200 | H2 2021 | |

| All EU/EEA payment institutions | >3 200 | H1 2019 | Payments, Resolution** (Planning, MREL Decisions, MREL/TLAC) |

| All EU/EEA e-money institutions | >300 | H1 2019 | Payments |

* Data for ~50 Key Risk Indicators from Q4 2008 onwards is available at the EBA for ~50 institutions from 20 EU countries, covering at least 50% of the total assets of each national banking sector. Numbers are based on non-harmonised prudential and financial reporting standards applicable in the EU before 2014. From Q1 2014 onwards, the data available at the EBA for the sample of largest credit institutions and banking groups accounted for more than 80% of EU banking sector total assets.

** Long-term expectations.

As it did in 2023, the EBA contributed to fostering transparency and market discipline in the EU banking sector. In December 2024, the authority published the annual transparency exercise, together with the autumn 2024 edition of the Risk Assessment Report (RAR). This provided transparency on around 9 500 data points per bank, in a comparable and accessible format, for 123 banks from 26 countries across the EU and EEA, complementing banks’ own Pillar 3 disclosures, as required by the EU’s CRR. The EBA provided users with a variety of interactive tools to visualise and compare data over time, both by country and by individual banks on capital positions, financial assets, risk exposure amounts, sovereign exposures and asset quality of the EU banking sector covering the latter half of 2023 and the first half of 2024. To reduce the reporting burden for the entities, the exercise was exclusively based on supervisory reporting data submitted to the EBA via EUCLID.

The EBA also carried out a number of data-driven analyses and it supported calls for advice, providing insights and comprehensive analyses that significantly enhanced decision-making processes and increased transparency. In 2024, the EBA provided a draft report in response to the CfA on EU banks’ funding and exposures in foreign currencies and a CfA on the market share of non-EU entities operating in the EU banking sector and the concentration of their activity in specific countries or sectors. The EBA leveraged existing FINREP data to create an EU-level set of indicators.

In the field of data collection, in 2024 the EBA began adapting EUCLID for receiving data from new types of reporting entities (MiCA/DORA) and new directly reported data flows (MiCA, Pillar 3). Regarding data dissemination, the EBA Risk Dashboards publication process was streamlined, resulting in more timely publication and increasing the value of the reported data. The EBA offered more visualisation tools and digitalised the RAR to provide better data insights and easier use of data. The EBA also expanded its offering to competent and resolution authorities of its EBA Data Access Portal (EDAP) with master data and report monitoring and data quality indicators.

The EBA continued to implement the Pillar 3 data hub envisaged by the Level 1 legislation. Building on the feedback received on the discussion paper launched in 2023, a pilot exercise with voluntary institutions to test the process for large and other institutions was completed in 2024. Conclusions from this pilot exercise, together with the feedback received during the consultation, were taken into account when finalising the draft ITS covering IT solutions, data exchange formats and technical validations. The final draft ITS were submitted to the Commission for adoption in February 2025.

The Pillar 3 hub will ultimately be connected to the European single access point (ESAP), on which the ESAs published the final draft ITS specifying certain tasks of the collection bodies and functionalities in October 2024. The published ITS represent the first milestone for the successful establishment of a fully operational ESAP.

In the area of integrated reporting, the governance structures were set up in 2024, following the finalisation and publication in March of the MoU signed with the ECB. The Joint Bank Reporting Committee (JBRC), which is the forum for collaboration between European and national authorities on reporting topics, had its first meeting in May. The JBRC will cooperate with the industry through the Reporting Contact Group, which was established with 22 members and had its first meeting in November. Furthermore, one of the main tasks of the JBRC – achieving semantic integration – was also launched, with the creation of an expert group on semantic integration that started its work based on the roadmap and methodology for semantic integration developed jointly by the ECB and the EBA during the first half of the year. This work will increase efficiency in reporting by streamlining and aligning definitions, as well as removing overlaps and redundant requirements.

Anca Dinita – Integrated reportingWhat is the project about and your role? As the EBA team lead for the Integrated Reporting project, I have the privilege of being at the forefront of transforming how we deal with data, a valuable yet scarce and costly resource. Moving away from siloed approaches, it is essential that we, as authorities, collaborate more closely in defining and collecting the data we need and share it responsibly, under the appropriate legal frameworks. In my role I collaborate and work alongside exceptional colleagues from the EBA and from national and European authorities, contributing to the development of a more efficient and effective approach to reporting data for all stakeholders involved, including industry. What are the challenges of the project? The challenges we face are complex, stemming from the diverse needs of numerous stakeholders and the necessity to maintain accurate and reliable reported data, even when regulations are being updated. Therefore, we have adopted a step-by-step approach to achieve greater integration. The year 2024 represents a significant milestone for the project. The EBA and ECB established the Joint Bank Reporting Committee to oversee the development and implementation of an integrated approach. Similarly, the DPM alliance between the EBA, EIOPA and the ECB was formed to create a common governance framework for the DPM2.0 meta model, marking the first step towards building a unified data dictionary. Preparatory technical work for integration started some years ago and is now being continued under the new governance frameworks, reflecting our ongoing close collaboration among the multitude of stakeholders involved. |

In 2024, the EBA announced the implementation of the enhanced Data Point Model and methodology, DPM 2.0, to ensure the EBA data dictionary is fit for future challenges of reporting and digital processing. DPM 2.0 was used for the reporting release 4.0 framework, published in December 2024. In parallel and in preparation for the migration to DPM 2.0 and for the work on integrated reporting, the EBA has conducted a quality review of its DPM data dictionary definitions to improve its semantic glossary, and the way the latter is used to define the reporting variables included in the EBA’s regulatory frameworks. Release 4.0 incorporates the revised glossary. Finally, the EBA started using the new Digital Regulatory Reporting tool, DPM studio, to produce the reporting frameworks, including the DPM releases, the complete validation rules lifecycle, and the creation of XBRL taxonomy packages. Both the DPM standard 2.0 and DPM studio were developed jointly with EIOPA.

Tomas Meri – Master data managementWhat are some of your main tasks as Team Leader? As Team Leader for Master Data Management (MDM), one of my responsibilities is to map business needs to system configurations and coordinate efforts across Competent Authorities (CAs) and Resolution authorities (RAs) and other EU institutions, such as the ECB and the SRB. The main goal of my team is to ensure that master data is of good quality and up to date. We also regularly configure the system for new mandates, such as the recent IRRBB, DORA Register of Information, diversity benchmarking, MiCA, resolution planning and CRR3/CRD6 changes. What is master data? Master data is information about the reporting entities. In the statistical domain, master data provides the most foundational information about entities and their attributes, unique identifiers, hierarchies and relationships within an organisation. This information is shared across business functions and systems to support business processes and decision making via a Master Data Management (MDM) function, which is a critical component of any organisation’s data strategy, particularly in complex organisations with multiple stakeholders, where data silos can lead to inefficiencies and errors. What does you team do? The role of MDM is to:

At the EBA, master data is also needed for publishing registers (for instance, the credit institution register) and for setting correct reporting obligations when collecting data. Master data is managed via the EBA’s EUCLID system, where the EBA is responsible for system configurations and CAs/RAs for ensuring master data is up to date. |

Furthermore, the publication of guidelines on the resubmission of historical data under the EBA reporting framework provided a common approach for financial institutions in case there are errors, inaccuracies or other changes in the data reported in accordance with the supervisory and resolution reporting framework developed by the EBA. This will enhance the quality, consistency and completeness of reported data. They deliver on one of the remaining open recommendations set out in the 2021 Cost of Compliance report and thus conclude the work on the related roadmap. Policy work on reporting and transparency is covered under Sections Implementing the Basel framework in the EU and enhancing the Single Rulebook, Developing an oversight and supervisory capacity for DORA and MiCA and Risk assessment and data.

As part of the EBA’s continued efforts in the field of supervisory disclosure, in November 2024 the EBA updated the centralised information disclosed by EU CAs, in accordance with their ITS on supervisory disclosure under CRD and IFR, which provide for the information being accessible in one single electronic location. This includes information regarding the laws, regulations, administrative rules and general guidance adopted by the Member States in the field of prudential regulation and supervision, aggregate statistical data on key aspects of the implementation of the prudential framework in each Member State, but also information on options and national discretions available in EU banking legislation and general criteria and methodologies used by national authorities in the SREP.

KPIs

| Indicator | Weight | Short description | Target | Achievement | |

|---|---|---|---|---|---|

| A | Timeliness of reporting (ratio %) (Results / Impact) | 25% | From EUCLID: Accepted modules / Expected modules by remittance date (T)+10 working days (wd) | >95% | 97.15% |

| B | Completeness of reporting (ratio %) (Results / Impact) | 25% | From EUCLID: Not reported / Expected templates by remittance date (T)+10 wd | <0.1% | 0.03% |

| C | Accuracy of reporting (ratio %) (Results / Impact) | 25% | From EUCLID: Failed error rules / Total of error rules executed against the received file by remittance date (T)+15 wd | < 0.1% | 0.02% |

| D | Time to publication of Quarterly Risk Dashboard (nbr days) (Results / Impact) | 25% | Working days from final remittance date of supervisory data (based on the EBA’s DC 404) to date of publication on the EBA’s RDB web page | < 15 | 19 |

* Target for KPIs have been adjusted from: KPI A > 85%, KPI B < 1%, KPI C < 0.25, KPI D <30.

Source of information KPI A to D: EUCLID.

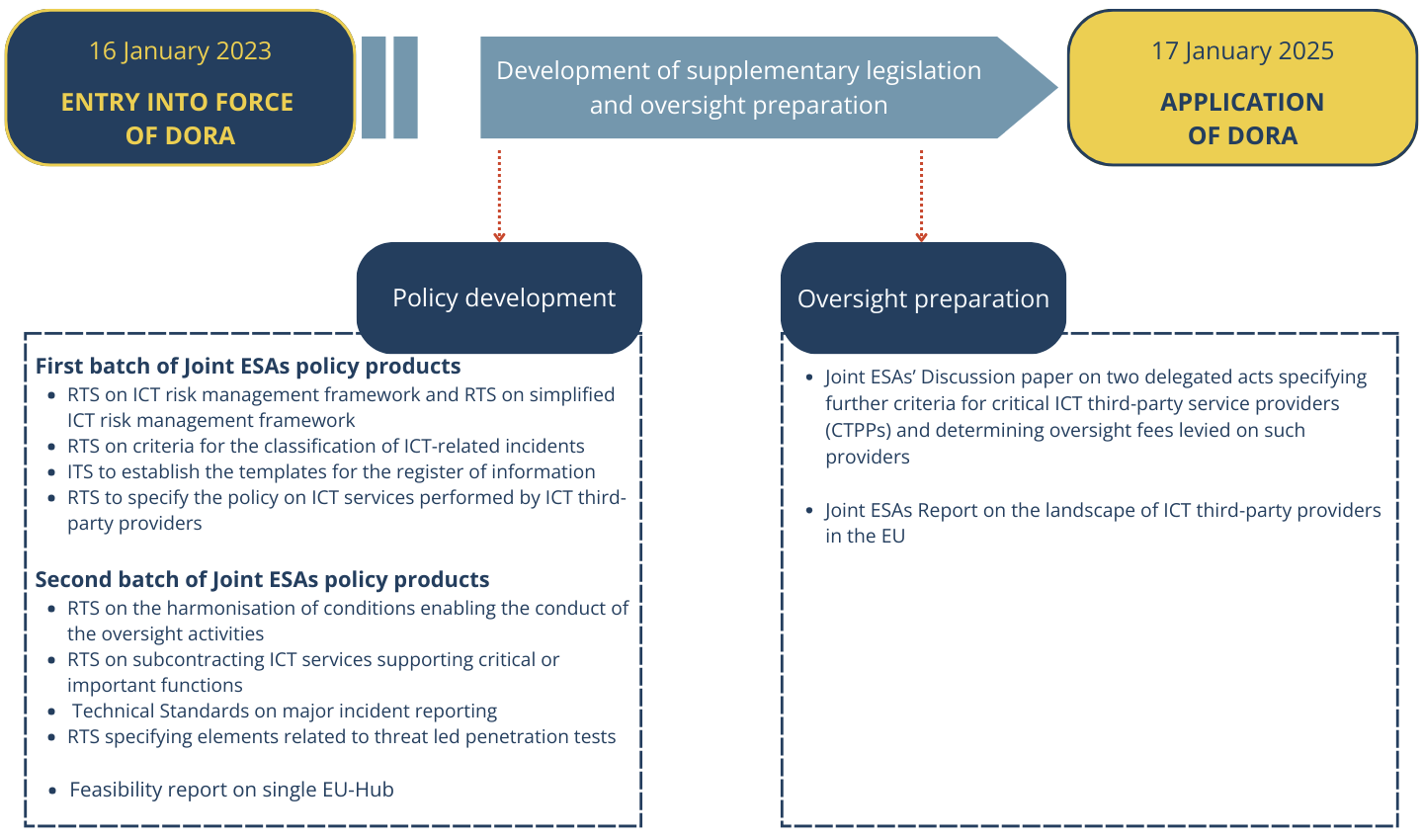

Developing an oversight and supervisory capacity for DORA and MiCAR

DORA and MiCA are part of the EU Digital Finance Strategy, which aims to ensure that the current legal framework does not pose inadvertent obstacles to the use of new technologies and the emergence of new products while ensuring effective risk mitigation.

In 2024, the EBA, together with other appropriate ESAs, finalised the MiCA and DORA policy mandates, thereby contributing to the ICT risk management dimension of the Single Rulebook and to a consistent framework for the regulation and supervision of crypto-asset activities.

DORA Policy

DORA, which entered into force on 16 January 2023, has applied from 17 January 2025, with the ESAs collectively delivering 13 legal instruments in January and July 2024 in relation to ICT risk management, incident reporting, third-party risk management, testing and oversight. In doing so, the ESAs took into consideration the feedback from the market and recommendations of the Joint ESA ACP. On 7 March, in response to the Commission’s rejection of the draft ITS on the registers of information, the ESAs published and submitted an opinion on these ITS to the Commission.

With the delivery of the regulatory mandates, there was additional focus on preparing for the taking up of the new roles and tasks assigned by DORA.

DORA oversight

The EBA, together with EIOPA and ESMA, advanced its preparations for oversight over CTPPs. This included the establishment of the new governance structures, namely the Oversight Forum (a new JC subcommittee) and the Joint Oversight Network (ESAs), as well as the arrangements to set up and operate the Joint Examination Teams. The ESAs have also been preparing the methodologies and processes to support the oversight activities. New IT systems are being developed to support the designation of CTPPs and future collaboration when performing oversight tasks.

To jointly tackle their new oversight responsibilities over CTPPs, the ESAs set up a joint directorate to pool the resources allocated by the legislation to carry out the oversight tasks with the support of NCAs in the Joint Examination Teams (JETs). This will ensure maximum consistency in the oversight approach towards CTPPs, optimise the use of resources (avoiding redundancies), including for their allocation over time, and facilitate the development of a common oversight culture in largely uncharted territory. The director leading the new joint directorate was recruited in October 2024 and is responsible for implementing and running the oversight framework for CTPP at European level, contributing to the smooth operation and stability of the EU financial sector.

To build operational and ICT risk capacities internally during the execution phase of the implementation plan, the EBA offered training in-house, via the EU Supervisory Digital Finance Academy, and other means with a view to building competencies at the ESAs and CAs for managing DORA-related activities. The EBA also offered training for staff on oversight techniques, policies and procedures.

One of the essential components of the DORA framework is the designation of CTPPs. To support this first step of the oversight activity, in November 2024 the ESAs published a decision providing a general framework for the annual reporting to the ESA of the information necessary for CTPP designation, including timelines, frequency and reference dates, general procedures for the submission of information, quality assurance and revisions of submitted data, as well as confidentiality and access to information. In particular, the decision requires CAs to report by 30 April 2025 the registers of information on financial entities’ contractual arrangements with ICT third-party service providers. While the ITS on the registers of information was adopted late by the Commission, the essential part of the requirements for registers of information has been available since April 2024.

To support industry preparations, the ESAs shared the draft templates, DPM and reporting technical package in May 2024 and carried out a voluntary dry run exercise on the reporting of registers of information, with the participation of around 1 000 financial entities across the financial sector in the EU. As part of the exercise, the ESAs have published numerous supporting documents, organised three industry workshop with a wide reach of participants, and provided data quality feedback to the participating financial entities. The support offered by the ESAs did not stop with the publication of the dry run summary report in December 2024, as the ESAs have continued updating supporting explanatory documents and the frequently asked questions on the dedicated web page throughout 2024 and 2025.

Antonio Barzachki – DORA oversight preparationsThe team that I lead is responsible for establishing the novel oversight function under DORA on critical providers of ICT services (e.g. cloud services, security management) to financial entities. This oversight function aims at providing assurance that the critical providers manage their risks effectively, thus ensuring continued and secure provision of financial services to consumers, and the stability of the financial system. We embarked on the journey of developing the oversight framework more than two years ago, jointly with colleagues from EIOPA and ESMA and closely cooperating with national authorities and other EU institutions. Throughout this journey, we have successfully progressed multiple parallel activities, met tight timelines, navigated through complex governance, managed many different stakeholders, mitigated various risks and resolved all issues faced. At the end of 2024, I am proud to say that thanks to the motivation, commitment and high-quality work of the team, we are almost ready. We have established a first of its kind cross-ESA joint team, for oversight made up of staff from the three authorities. We have set up the governance structures, the operating model, and are in the process of finalising the internal methodologies and IT tools to support the oversight activities. I am confident that we are well prepared to designate the critical providers of ICT services and to start engaging with them in 2025. |

Other DORA tasks

In line with the relevant ESRB recommendation, the ESAs announced in July 2024 the establishment of the EU Systemic Cyber Incident Coordination Framework (EU-SCICF) in the context of DORA, which was accompanied by the publication of a factsheet. This framework will facilitate an effective financial sector response to a cyber incident that poses a risk to financial stability, by strengthening coordination among financial authorities and other relevant bodies in the European Union, as well as with key actors at international level.

With the completion of the policy mandates and the approaching DORA application date, the ESAs also intensified their work to help converge supervisory practices in the implementation of the new framework. This led to the publication in December 2024 of a joint ESA statement, to ensure that financial entities are prepared for the new requirements, particularly on the register of ICT third-party providers and on the reporting of ICT incidents.

MiCA policy

For MiCA, which entered into force on 29 June 2023, and the provisions relating to asset-referenced tokens (ARTs) and electronic money tokens (EMTs) applying from the end of June 2024 (the remaining provisions applying from the end of December 2024), the EBA delivered 20 technical standards and guidelines in 2024 (two of which were joint with the ESMA, and one with the ESMA and EIOPA), and one set of own initiative guidelines to address reporting gaps under MiCA. The policy mandates under MiCA expanded the common Single Rulebook for crypto-asset issuance in the EU, with the aim of enhancing consumer protection (e.g. with clear rules on complaints handling), governance (e.g. measures to identify and address conflicts of interest), prudential resilience (e.g. regarding reserve, recovery and redemption arrangements), and reporting requirements.

MiCA supervision and other tasks

MiCA confers on the EBA supervision tasks with regard to ARTs and EMTs that are determined by the EBA to be ‘significant’. In 2024, the EBA took preparatory steps for these tasks and developed its framework for significance assessments and supervisory policies and procedures and forms, templates for the exchange of information between all relevant parties (including supervised issuers, national CAs, the ECB and other relevant central banks). In parallel, the EBA developed the IT capabilities needed to support the EBA’s supervision function. The EBA also established the CASC to support the authority in the performance of its supervision tasks[1], as a replacement of its temporary CSCG, which met throughout 2024 to facilitate knowledge-sharing between CAs and support supervisory convergence efforts in the initial phase following the application of MiCA. In 2024, the EBA also worked towards strengthening its supervisory capacity, in particular by further extending training for staff, and by organising workshops with NCAs on techniques for the supervision of issuers of ARTs and EMTs.

As part of its convergence efforts, in July 2024 the EBA published a statement addressed to issuers, consumers and other relevant stakeholders. In the statement, the EBA reminded (prospective) issuers of ARTs and EMTs of the new requirements under MiCA, and drew attention to the relevant technical standards and guidelines. The EBA also drew attention to factors that consumers can check before deciding whether to acquire an ART, EMT or other type of crypto-asset, and reminded consumers of the risks of acquiring crypto-assets that have not been issued in accordance with the applicable provisions of MiCA. Additionally, in July 2024, the EBA published the key topics for supervisory attention across the European Union for issuers of ARTs/EMTs in 2024/2025. Both documents were prepared with a view to promoting the timely and consistent application of MiCA.

Beyond supervisory preparedness, in 2024 the EBA completed preparedness actions for its other tasks under MiCA, specifically regarding its tasks of preparing non-binding opinions on the classification of crypto-assets under MiCA[2], and its task of exercising temporary intervention powers[3].

KPIs

| Indicator | Weight | Short description | Target | Achievement | |

|---|---|---|---|---|---|

| A | Delivery of policy mandates under DORA/MiCA (Output) | 30% | Delivery of policy mandates and CP within the legally required timeline | 95% | 100 % of DORA and MiCA mandates delivered on time. |

| B | Operational readiness to take up new tasks (Output / Result) | 70% | As part of the DORA and MiCA proposals, the EBA should be ready to take up tasks (supervision/oversight and others) | Completion of preparatory work | DORA oversight preparations progressed as planned. MiCA supervision preparations progressed as planned. |

Source of information KPI A: EBA WP monitoring tool and publications; KPI C: DORA /MiCA milestones tracker.

Increasing focus on innovation and consumers (including access to financial services) while preparing the transition to the new AML/CFT framework

In 2024, the EBA further enhanced the focus on innovation, on the conduct of financial institutions and on consumer protection mandates (including those given by MiCA and the Credit Servicers and Credit Purchasers Directive (CSD)) and also contributed to ensuring that citizens have access to financial and banking services. The authority also worked to strengthen CAs’ ability to tackle financial crime across its regulatory and supervisory remit.

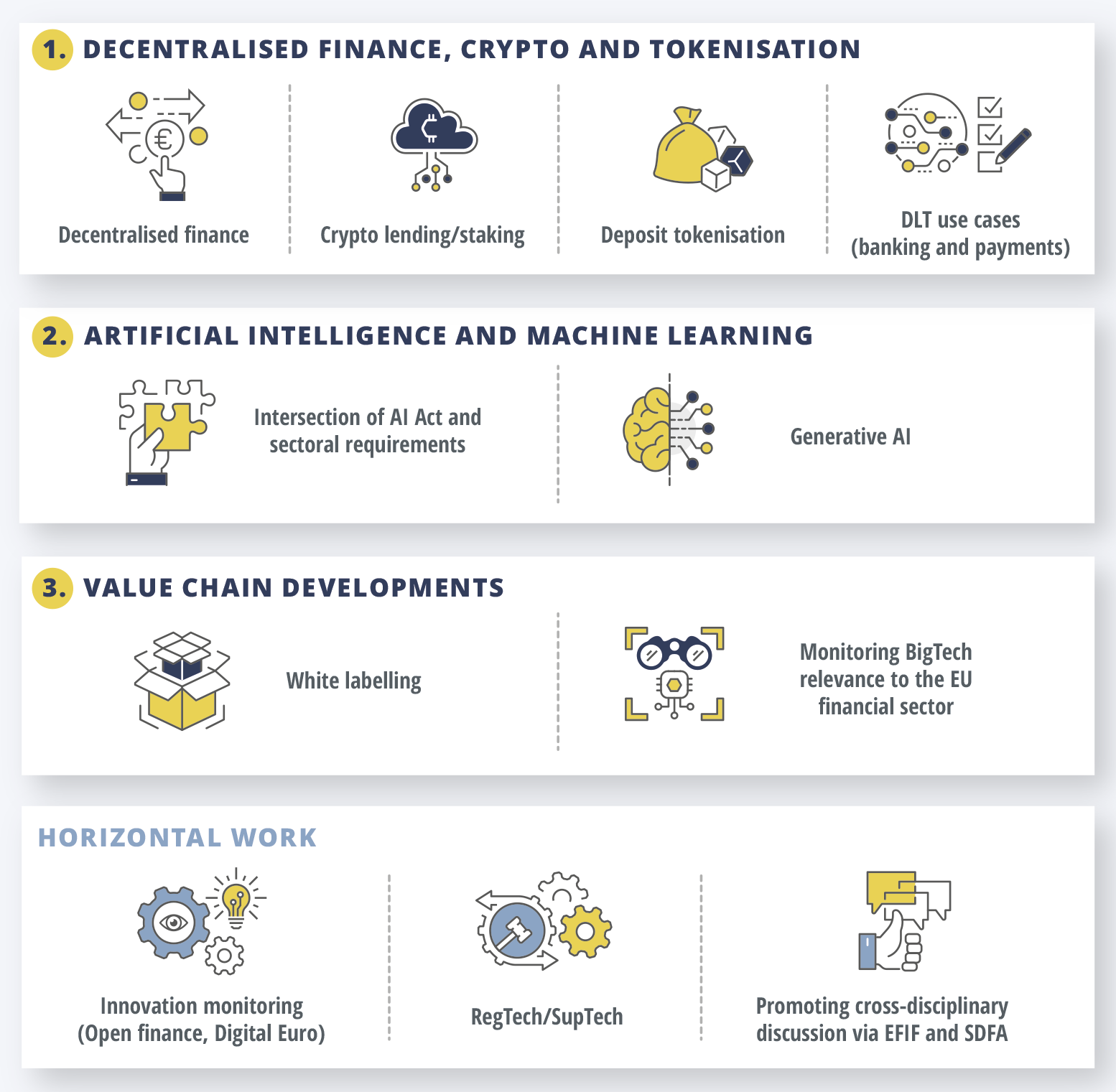

Innovation

The EBA continued to monitor financial innovation, to identify opportunities and risks, promote knowledge-sharing and capacity-building among supervisors, and identify any areas where specific regulatory or supervisory responses may be needed. Crypto-assets, tokenisation in relation to new financial products and services and decentralised finance and the application of AI/ML in financial sector, as well as digital identity management, digital platforms, supervisory and regulatory technologies (SupTech and RegTech), are examples of innovations that are currently on the EBA’s innovation monitoring radar. Keeping a close eye on developments via targeted surveys of industry and CAs, as well as information exchanges with industry, CAs and other EU and international organisations help to identify emerging risks and provide guidance on areas where further work by the EBA may be needed.

As part of its innovation monitoring work, the EBA published a factsheet on the uses of distributed ledger technology (DLT) in the EU banking and payments sector. The EBA also published, in December 2024, a report on tokenised deposits which assesses potential benefits and challenges of tokenised deposits, and aims to promote convergence in the classification of such deposits in contrast with EMTs issued by credit institutions under MiCA.

Main findings:

|

Regarding crypto-asset market developments, the EBA, jointly with the ESMA, prepared a thematic report on recent developments (published in January 2025) including decentralised finance (DeFi) and crypto-asset staking and lending. This report contributes to the Commission’s report to the European Parliament and Council under Article 142 MiCA (the Commission report on the latest developments in crypto-assets).

Main findings:

|

Importantly, in 2024 the EBA commenced work regarding the implementation of the EU’s AI Act. The EBA commenced an assessment of the interplay between the AI Act and sectoral legislation applicable to the EU banking and payments sector, with a view to informing further mapping, assessment and discussion in 2025, to identify any actions needed to secure regulatory consistency and supervisory convergence. Additionally, the EBA took actions to assess AI Act implications, providing inputs to the Commission to inform the Commission’s guidelines on the AI System definition[4] and to support knowledge-sharing among CAs regarding the designation in the Member States of ‘market surveillance authorities’ for the purposes of the AI Act.

More generally, the EBA continued to monitor adoption of AI applications in the EU banking and payments sector, and assess potential opportunities and risks (including via a workshop in April 2024 on General Purpose AI (GPAI)), publishing its findings in the Autumn Risk Assessment Report.

Earlier in 2024, the ESAs published a joint report with the findings of a stocktake of BigTech’s provision of direct financial services in the EU. The report identifies the types of financial services currently carried out by BigTechs in the EU pursuant to EU licences, and highlights inherent opportunities, risks, regulatory and supervisory challenges, and recommends steps to enhance the monitoring of these activities. Additionally, the EBA commenced work on a thematic report (to be published in 2025) on white labelling, as part of its wider efforts to monitor the implications of value chain evolution.

Finally, the EBA, together with the ESMA and EIOPA, further contributed to the European Forum for Innovation Facilitators (EFIF) and guided and steered development of the EU Supervisory Digital Finance Academy (SDFA) training curriculum to ensure it is tailored to the CAs’ needs and contributes to the SDFA’s aim to strengthen supervisory capacity in innovative digital finance.

Consumer protection

More specifically with regards to consumer protection, the EBA continued its efforts to enhance the monitoring of financial institutions’ conduct of retail activities across the authority’s regulatory and supervisory remit.

As a follow-up to the Consumer Trends Report published in April 2023, the EBA undertook a fact-finding exercise on the creditworthiness assessment (CWA) practices of non-bank lenders (NBLs). The exercise, the results of which were published in August, was aimed at gaining insight into the extent to which NBLs contribute to over-indebtedness and arrears. It revealed that, while some NBLs might service segments of the population that may have limited opportunities to access traditional banks for credit, a significant number of the surveyed NBLs appear to apply inadequate practices for information gathering and verification during their CWAs.

Main findings: The report also found that the lack of a harmonised definition of NBLs and of a harmonised authorisation framework in the EU contribute to different types of NBLs being supervised in different ways across EU Member States. Consequently, different rules apply to entities of a similar kind across the EU. The EBA will continue monitoring the activities of NBLs through its biennial Consumer Trends Report and, depending on the findings and need, may consider initiating further ad hoc action to foster further protection of EU consumers. |

The ESAs published a joint report in July 2024 following their workshop on the use of behavioural insights by supervisory authorities in their day-to-day oversight and policy work. The report provides a high-level overview of the main topics discussed during the workshop held on 14 and 15 February 2024 for national supervisors and other CAs, where participants explored the added value of behavioural insights in their work by exchanging experiences and discussing the challenges they face.

In addition, the authority, in coordination with the ESMA, developed technical standards (published in April 2024) setting out complaints handling procedures for complaints from holders of ARTs and other interested parties (including consumer associations that represent those holders) to issuers of such assets under MiCA – specifying the requirements, templates and procedures for handling complaints received.

In addition, in July, the EBA published final guidelines that extend the existing joint committee guidelines on complaints handling (JC Guidelines) to credit servicers under the new Credit Servicers Directive (CSD), ensuring that, when handling complaints from borrowers, credit servicers are required to apply the same effective and transparent procedures that have been applied for more than a decade to other firms in the banking, insurance and securities sectors. Further reflecting the authority’s concerns about simplification, the EBA introduced non-substantive changes in order to align the guidelines with the amendments made to the EBA Regulation in 2020, allowing the EBA to delete procedural requirements, directed towards national authorities, that are no longer required.

In June 2024, the EBA furthermore amended its guidelines on arrears and foreclosure to address the changes introduced in the Mortgage Credit Directive (MCD), following an assessment of the impact of revision of Article 28(1) of the Directive, and concluded that Guideline 4 on ‘resolution process’ needs to be removed, given that its content had been embedded in E U Law.

Again in the context of the CSD, the guidelines on national lists or registers of credit servicers, published in March 2024 and aimed at CAs managing such lists or registers, specify i) the content of the lists or registers; ii) how they should be made accessible; and iii) the deadlines for updating them. To further enhance transparency for credit purchasers and borrowers, and to establish a level playing field across the EU, the lists or registers should also make it easier for borrowers to access information on complaint-handling procedures offered by CAs.

In accordance with Articles 39(2) and 41(1) MiFIR, the EBA also monitors the market for structured deposits. This mandate, in combination with a Commission request for the EBA to issue recurrent reports on the cost and past performance of structured deposits, led to a report published in July 2024 on structured deposits in the EU. The report highlighted that, in more than half of the 27 national markets in the EU, structured deposits do not exist, and that the EU market remains very small at an aggregate level, with only EUR 16.7 billion of structured deposits sold during the reference period of the report of 1 January to 30 September 2023 – the report’s reference period. 95% of these were concentrated in just four EU Member States. These four countries reported increases in the number of products offered and volumes sold, albeit at a very low level. Across the EU, the total value of structured deposits sold in each Member State ranges from EUR 2 million to EUR 10 billion, showing a disparity in market penetration and investor interest.

As regards cost and past performance of structured deposits – covered as per the Commission request – the limited performance data that are available indicate that the annual net returns for structured deposits vary significantly, with some structured deposits offering no return, while others showing positive returns, in one case of up to 24%.

In 2024, the EBA acted as lead organiser of the Joint ESAs’ Consumer Protection Day, which took place on 3 October 2024 in Budapest. The event followed the theme of ‘Empowering EU consumers: fair access to the future of financial services’ and featured three panels covering the topics of AI in financial services, access to consumer-centric products and services, and sustainable finance. Speakers and panellists included leaders from consumer organisations, regulatory authorities, EU institutions, academia, and market participants from across the European Union, with 300 in-person participants and more than 600 viewers online. Highlights from the day were shared publicly later in October.

AML/CFT

Through 2024, the EBA continued to lead, coordinate and monitor the EU financial sector’s AML/CFT efforts. As part of this, it continued to set common standards in line with its legal mandate where warranted and necessary, highlighted and acted upon emerging ML/TF risks, and supported the effective implementation of robust approaches to tackling ML/TF, sanctions and other financial crime risk across the EU.

Work to deliver the EBA’s mandates in Regulation (EU) 2023/1113 on information accompanying transfers of funds and certain crypto-assets (the Funds Transfer Regulation – FTR) was a particular focus. In 2024, the EBA issued:

- Guidelines on the so-called ‘travel rule’, i.e. the information that should accompany transfers of funds and certain crypto-assets. These guidelines, which were issued in July 2024, serve to tackle the abuse of such transfers for ML/TF purposes. They updated and replaced guidelines on the travel rule that the EBA had issued in 2017.

- Two sets of guidelines on internal policies, procedures and controls to ensure the implementation of EU and national sanctions. These guidelines, which were issued in November 2024, set out, for the first time, common EU standards on governance arrangements, and on the policies, procedures and controls that financial institutions should have in place to be able to comply with EU and national restrictive measures.

- A public consultation launched in December 2024 on draft technical standards specifying the criteria according to which crypto-asset service providers (CASPs) should appoint a central contact point to ensure compliance with local AML/ CFT obligations of the host Member State. These RTS amend the RTS the EBA had issued previously, by extending their scope to CASPs.

In addition, the EBA worked to include specific provisions on identifying and tackling ML/TF risks in 10 MiCA instruments, and published an ‘explainer’ to provide a comprehensive overview of the holistic approach to tackling ML/TF risk in crypto to an emerging sector.

The EBA continued to monitor and disseminate information on emerging ML/TF risks and coordinated CAs’ actions where necessary to tackle those risks. This included:

- Using the EBA’s EuReCA database to inform CAs of risks that were relevant to them concerning individual institutions under their AML/CFT supervision, and concerning their overall approaches to tackling ML/TF risk. For example, submissions suggested that across the EU, ML/TF risks associated with the ineffective use of RegTech solutions were increasing. By the end of 2024, EuReCA contained information on 2 542 material weaknesses and corrective measures concerning 517 institutions submitted by 44 CAs from all Member States.

- Assessing the risks and impact of the use of virtual IBANs (vIBANs) and publishing the findings in a report in April 2024. The report highlighted the lack of a common definition at EU level and divergent approaches, both by CAs and by the industry, which raise challenges not only from an AML/CFT perspective, but also from consumer and depositor protection, authorisation and passporting, and regulatory arbitrage perspectives. The EBA provided recommendations in that respect.

- Hosting meetings of EU supervisors to coordinate actions and ensure a robust approach to tackling crystallised ML/TF risks in individual CASPs. Over the course of 2024, the EBA hosted three such meetings, in addition to advice it also provided on tackling ML/TF risk in specific situations. As a result of the EBA’s work, CAs reassessed the fitness and propriety of senior managers and beneficial owners in three cases, and triggered other supervisory actions in seven cases.

- Raising awareness of specific risks it had identified by publishing factsheets for financial institutions on terrorist financing and derisking.

As was the case in previous years, the EBA continued to support the effective implementation of its standards through targeted reviews and training. In 2024, the EBA:

- Completed its reviews of EU/EEA CAs’ approaches to tackling ML/TF risk in the banking sector. By December 2024, the EBA had assessed all 40 CAs in the EU and provided them with feedback and recommendations for change where necessary. For the final round of reviews, as set out in a report the EBA published in December 2024, the EBA found that AML/CFT supervisors had taken important steps to implement a risk-based approach to AML/CFT, but that challenges continued to exist in relation to prudential supervision and risk assessments in particular. The EBA will now conduct a final stocktake of all the actions taken by CAs in response to the EBA’s recommendations and publish a final report in 2025 as part of the EBA’s handover to AMLA.

- Continued to monitor the effective functioning of AML/CFT colleges. The fourth report on the functioning of AML/CFT colleges, which was published in December, highlights that AML/CFT colleges worked well in the period under review, but further progress was necessary in two areas: adjusting the functioning of AML/CFT colleges to specific ML/TF risks to which the underlying firm is exposed, and discussing the need for a common approach or joint action.

- Provided training to 350 staff from CAs on crypto, EuReCA, and on the effective assessment of ML/TF risk.

The EBA worked closely throughout 2024 with CAs and the Commission to prepare for the transition to the EU’s new legal and institutional AML/CFT framework. The publication of the new AML/CFT package in June 2024 started a transition period whereby the EBA continues to be responsible for AML/CFT until 31 December 2025 while the new AML/CFT Authority, AMLA, is being set up. As part of this, the EBA has started to prepare the transfer of data, knowledge and powers to AMLA, supported national CAs in their preparatory work to adjust to the new framework, and contributed to safeguarding effective cooperation between prudential and AML/CFT supervisors and regulators in future.

An important aspect of this work relates to the preparation of the EBA’s response to a Call for Advice the EBA received from the Commission on 12 March. In this Call for Advice, the Commission tasks the EBA with the preparation of several technical standards that will be key to the new AML/CFT regime. The EBA is due to respond to the European Commission by the end of October 2025. Specifically, the Commission asked the EBA to prepare a common ML/TF risk assessment methodology for AML/CFT supervisors in line with Article 40(2) of the Sixth Anti-Money Laundering Directive (AMLD6) and the methodology that the AMLA will use to select institutions that will be directly supervised by it pursuant to Article 12(7) of AMLA. The EBA’s input will also cover customer due diligence aspects under Article 28(1) of AMLR and the criteria that supervisors will use to determine pecuniary sanctions or administrative measures under Article 53(10) AMLD6 and to consider possible guidance on the base amounts for such sanctions under Article 53(11) AMLD6. The EBA organised an industry roundtable in October 2024 to obtain the views of the private sector on these mandates with a view to informing its approach. A consultation was launched in Q1 2025.

KPIs

| Indicator | Weight | Short description | Target | Achievement | |

|---|---|---|---|---|---|

| A | Delivery of mandates conferred in sectoral legislation (Output) | 40% | The EBA will deliver on an estimated 20+ mandates conferred under the Markets in Crypto-Assets (MiCA), and the Credit Servicers and Credit Purchasers Directive (CSD) | 75% | 100% |

| B | Effective retail conduct supervision to enhance protection of consumers (Result / Impact) | 10% | The EBA will take action in response to information provided through retail risk indicators and the EBA’s Consumer Trend Reports 2022/2023 | 1 initiative | 1 initiative |

| C | Policy response and supervisory convergence in financial innovation (Result / Impact) | 10% | The EBA will deploy its mandate in monitoring innovation, contributing to a common approach towards new or innovative financial activities, and in providing advice to the co-legislators, by: i) issuing a number of thematic publications, incl. opinions or reports issued to the Commission and NCAs; ii) fostering knowledge-sharing via various platforms (EBA structures, EFIF, SDFA); iii) reviewing and verifying the training curriculum of the SDFA | Up to three initiatives 100% reviewed materials for SDFA | i) and ii) four initiatives (including workshops) iii) Fully achieved |

| D | Supporting the effective implementation of the new legal and institutional AML/CFT framework (Output / Result) | 40% | The EBA will work closely with AMLA to ensure the smooth transition of powers and effective cooperation between prudential and AML/CFT regulators going forwards. | 2 reports | Fully achieved: 2 reports |

Source of information KPI A and KPI B: EBA WP monitoring tool and publications; KPI C: EBA WP monitoring tool and report to SDFA; KPI D: EBA WP monitoring tool and EBA transition workplan.

Additional achievements in 2024

Work on proportionality

Since its creation in 2020, the ACP has been providing recommendations to the EBA on how to foster proportionality in its activities and missions. Its core mandate is to assess the EBA draft WP for the upcoming year and make recommendations to enhance its proportionality. It is also tasked with reviewing how the EBA has addressed its advice.

In 2024, the ACP followed up on its previous recommendations in the areas of Recovery and Resolution, ESG in supervision and regulation, and reporting and transparency, and recommended that the EBA also pay particular attention to proportionality in its work related to payment services, consumer and depositor protection.

The EBA took the recommendations into account in the preparation of these activities, recognising the value of enhancing proportionality where possible.

In the area of Recovery and Resolution, the work on revision of the RTS on resolvability assessments has been ongoing and the EBA engaged extensively on the topic with an aim of reviewing existing EBA products to increase optionality and the development of alternative strategies in the resolvability assessment process, reflecting the ACP’s recommendations. Similarly, considering the ACP’s advice, EBA has been reviewing the RTS on the content of resolution plans to streamline these plans, simplify them, amend the update frequency and help authorities focus on testing. Furthermore, the EBA’s review aimed at standardising resolution planning and a streamlined MREL section of the plan.

Addressing the continuous focus on proportionality in the EBA’s work, the EBA has started preparatory work on the inputs for the upcoming review of the SREP Guidelines, in particular regarding the management of ESG risks and transition plans. The simplification of Pillar 3 reporting templates for SNCIs, including the alignment of Pillar 3 disclosures with supervisory reporting, has been progressing throughout 2024, with further work expected in 2025.

The EBA finished implementing the recommendations from the study on the cost of compliance with supervisory reporting (2021), which aimed to reduce compliance costs for institutions by 25%, particularly for small and non-complex institutions. Reducing the overall reporting burden for SNCIs has become an integral part of all the EBA’s reporting work and, in addition, the EBA has considered proportionality in all new and amended reporting requirements, not only for SNCIs but also for medium and large institutions. As part of changes resulting from CRR3 and related to liquidity and FINREP, the EBA is also reviewing, existing data points and their relevance. The new JBRC and its units have been working on integrating supervisory, resolution and statistical reporting.

Considering the ongoing legislative discussions on PSD3 and PSR, the EBA actioned the ACP’s recommendation on payment fraud prevention, by publishing an opinion with legislative proposals for how to enhance payment fraud rules in April, and an inaugural joint report with the ECB on payment fraud data for 2022 and 2023 in August (see the Section Engaging with stakeholders for details).

Recovery and resolution

The Commission’s proposals for a strengthened CMDI framework, issued in April 2023, are aimed at enabling authorities to organise an orderly resolution for failing banks of any size and business model, including smaller players, drawing from lessons learned during the initial years of application of the existing rules. The proposals, to which the EBA has contributed in previous years through responses to various calls for advice, anticipate amendments to the Bank Recovery and Resolution Directive (BRRD), the Deposit Guarantee Schemes Directive (DGSD), and the Single Resolution Mechanism Regulation (SRMR). Whereas the proposals contain requirements for the EBA to issue standards on provisions and to report to the Commission on the framework’s effective and harmonised implementation, the uncertainty around the package’s finalisation has impacted and delayed the start of work on these resolution and deposit insurance mandates.

Notwithstanding this delay, the EBA worked on a number of related mandates, including one on recovery stemming from MiCA. This work led to the guidelines on recovery plans under MiCA issued in June 2024, which set out the requirements with respect to the format of the recovery plans and the information to be included in those plans, as well as supervisory expectations for issuers to be able to identify and understand the risks they face and formulate possible actions for restoring compliance with regulatory requirements.

In addition, the EBA launched a public consultation on its draft ITS, overhauling the resolution planning reporting framework, with the aim of further harmonising reporting on these plans in the EU and avoiding duplication of data requests, thus reducing institutions’ cost of compliance. Proportionality was a key driver of this work and led to a streamlining of datapoints to avoid overlaps based on the size and complexity of institutions.

The objective of the European Resolution Examination Programme (EREP) is to drive convergence. In August 2024, the EBA published its findings on the progress achieved with respect to the priorities set for 2023. The report found that convergence had increased within the EU with regards to resolution planning practices and objectives.

More specifically: