Part I – Achievements of the year

Achieving the 2023 core priorities

The following headings and subheadings break down in further detail the EBA’s main tasks and deliverables over the past 12 months. Detailed tables also feature throughout, illustrating how the EBA executed the WP, broken down by product category.

The 2023 Annual Report offers insights into the breadth and depth of the EBA’s activities, highlighting the EBA’s unwavering commitment to its regulatory responsibilities and its vital role in ensuring stability and integrity within the European banking sector.

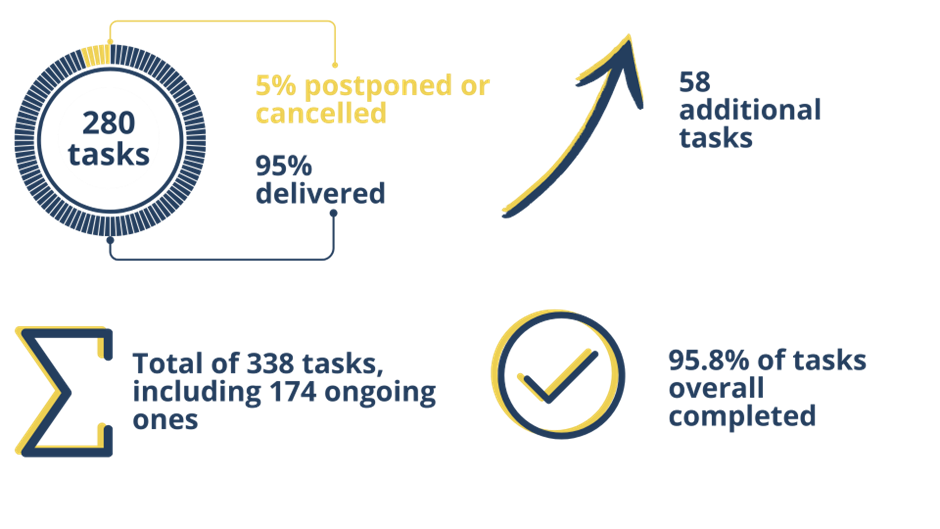

Figure 1: Achievements in 2023 in numbers

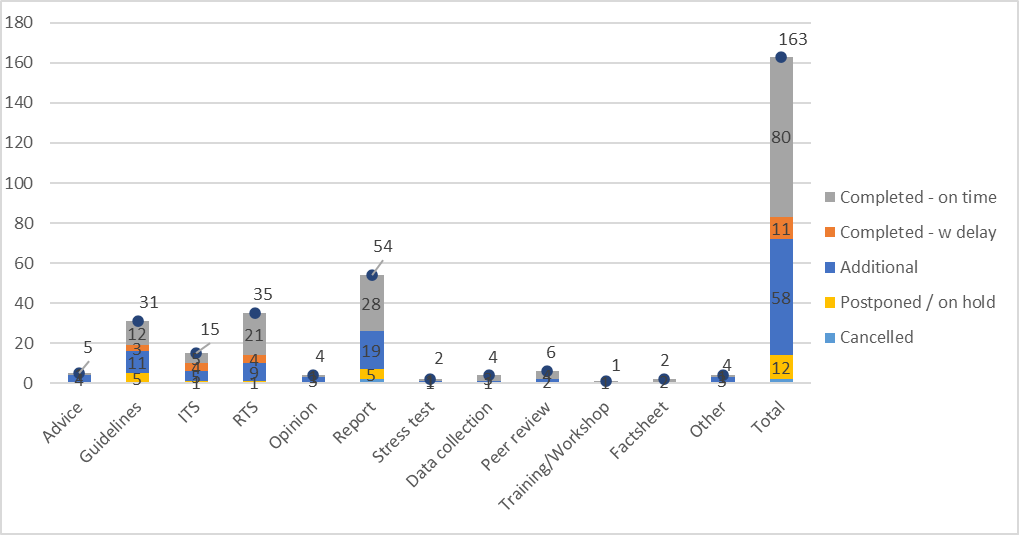

Figure 2: Breakdown of deliverables by category

NB: These deliverables do not include the c 175 tasks that are of an ongoing nature.

Finalising the implementation of Basel III in the EU

The banking package that was agreed on by co-legislators in 2023, i.e. Capital Requirements Regulation (CRR) III and Capital Requirements Directive (CRD) VI, will implement the Basel III framework in the EU.

To provide clarity to the industry on how the Authority will contribute to the implementation of the new legislation, in December 2023 the EBA published a roadmap detailing its approach to, and sequencing of, the work in the different areas in line with the legal deadlines set out by the co-legislators. Alongside the publication of the roadmap, a first batch of Consultation Papers (CPs) was published relating to the reporting/disclosure requirements and to market risk.

In the area of market risk, the EBA published draft RTS on the assessment methodology for the internal models approach to the fundamental review of the trading book (FRTB-IMA), which will provide clarification to supervisors and banks on the details relating to implementing internal models under the FRTB as well as to the report on the impact and relative calibration of the standardised approach for counterparty credit risk (SA-CCR).

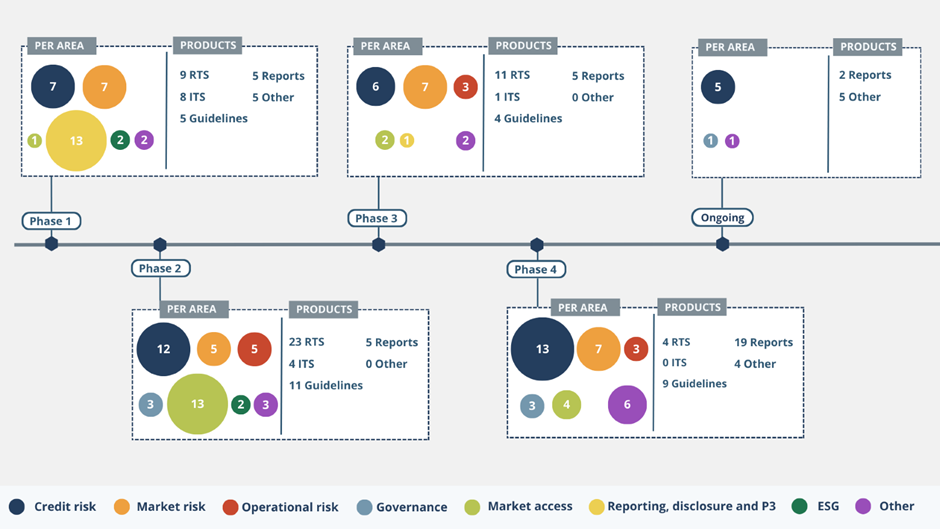

| The implementation of the banking package will be one of the main areas of work for the EBA in the coming years, with delivery of around 140 new mandates envisaged in 2024 and beyond. |

Figure 3: Overview of mandates by area

With respect to investment firms, the EBA’s work had two aims in 2023. Firstly, the EBA was focused on finalising the implementation of the technical details of the Investment Firms Regulation (IFR) and Investment Firms Directive (IFD) introduced in 2019. The delivery of the draft RTS on prudential consolidation for investment firm groups thus constituted the final EBA deliverable under the Investment Firms Roadmap. Secondly, on 1 February 2023 the EBA, along with the European Securities and Markets Authority (ESMA), received a Call for Advice (CfA) from the Commission on the implementation review for the IFR/IFD framework, and they then started on the work associated with this CfA. Additionally, on 25 July 2023 the EBA published the guidelines for consultation on the application of the group capital test for investment firms, which are due to be published before the end of Q2 2024.

In the fields of securitisation and covered bonds, the EBA finalised the RTS setting out homogeneity criteria for STS on-balance-sheet (or synthetic) securitisation transactions under the simple, transparent and standardised (STS) framework set out in the Securitisation Regulation, as well as the draft RTS on the exposure value of synthetic excess spread, set out in the CRR respectively.

The Authority continued to give significant attention to benchmarking activities in both credit and market risk models (inclusive of IFRS 9-related considerations) in order to support competent authorities (CAs) with the assessment of internal approaches used for the calculation of own funds requirements and for remuneration practices.

On the liabilities side, the EBA continued to monitor Common Equity Tier 1 (CET1) issuances and to follow developments relating to capital and capital issuances (Additional Tier 1 (AT1), Tier 2 and total loss-absorbing capacity / minimum requirement for own funds and eligible liabilities (TLAC/MREL) instruments in particular). This led to a combined update on TLAC/MREL and AT1 instruments published in July 2023, which evidenced further convergence and standardisation in terms of the drafting of the notes and programmes.

Furthermore, the EBA continued its follow-up work on the implementation of the EBA Opinion on legacy instruments (including in the context of the CRR II grandfathering provisions) and, after providing guidance on one specific issuance of legacy Tier 2 instruments in January 2023, addressed a second case in January 2024. The analysis of interactions among loss absorbency requirements (i.e. capital and TLAC-MREL stacking order, MDA and buffers, and output floors) will continue into 2024.

Given the economic circumstances, the EBA also embarked on work to monitor the impact of the interest rate environment on own funds and eligible liabilities aspects (e.g. on the valuation of non-equity instruments or on accounting-related aspects).

Furthermore, with respect to work regarding interest rate risk in the banking book (IRRBB), the EBA issued an opinion in Q2 2023 on changes that the Commission intended to apply to the draft RTS on supervisory outlier tests of net interest income (NII) as proposed by the Authority.

| Work was also carried forward on the scrutiny of IRRBB risks, as reflected in the publication in December 2023 of a heat map setting out aspects that will be subject to further monitoring and action, with corresponding timelines in the short-to-medium and long term (to continue in 2024 and beyond). |

In the area of liquidity, the EBA continued to review ways in which institutions and CAs have implemented the regulatory provisions, for example as regards notifications, use of national options and discretion, and monitoring of implementation in practice. This led the Authority to publish several (updated) monitoring reports, including the potential impact on liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) levels of the upcoming central bank funding repayment (mainly repayments under the targeted longer-term refinancing operations) as well as of a potential scenario of higher liquidity risks.

In terms of market access, the EBA continued to monitor the regulatory perimeter and authorisation practices as well as reports on the establishment of third-country branches and the intermediate parent undertaking framework, with a view among other things to facilitating cross-border cooperation between CAs supervising subsidiaries and branches of third-country groups. The EBA also started to examine the requirements imposed on various types of market players for access to the EU market, focusing in particular on access to the EU market under MiCAR by issuers of asset-referenced tokens (ARTs).

With regard to the authorisation of credit institutions and qualifying holdings, the EBA concluded the follow-up report on the related peer review, identifying solid improvements in particular with respect to assessment of the financial soundness of proposed acquirers and to suspicions of money laundering / terrorist financing issues.

As concerns supervisory convergence, the EBA performed the yearly European Supervisory Examination Programme and started its preparatory work for the future review of the guidelines on the Supervisory Review and Evaluation Process (SREP), looking at the supervisory measures, including capital add-on and liquidity measures, set by CAs throughout the European Union and launching a peer review devoted to proportionality in the SREP. The EBA also updated the regulatory products governing the functioning of Supervisory Colleges; this update was delivered in late Q4 and included an amendment to improve the sharing of information among authorities in the context of adverse economic events.

In matters of governance and remuneration, the EBA continued to monitor and benchmark diversity and remuneration practices at EU level, with findings published in Q1 in the latest editions of its recurring reports. At the same time it worked on the streamlining and effectiveness of related data collections.

An additional focus will be to assess whether specific parts of the rulebook should be updated, streamlined or simplified. Ease of access to the consolidated rulebook and its user-friendliness are also to be improved.

KPI

| Indicator | Weight | Short description | Target | Achievement | |

|---|---|---|---|---|---|

| A | Number of technical standards, guidelines, reports delivered | 100% | Number of technical standards, guidelines and reports delivered on time stemming from implementation of CRD VI / CRR III / BRRD III | 80% | 71% (or 82% with additional deliverables) |

See Annex I for details. Source of information: EBA WP monitoring tool and annual report.

Running an enhanced EU-wide stress test

Figure 4: 2023 stress test macro financial scenario

The results of the 2023 EU-wide stress test showed that European banks remain resilient under an adverse scenario, which combines a severe EU and global recession, high and persistent inflation, increasing interest rates and higher credit spreads.

Table 2: Summary of key results

| CET1 capital ratio | Leverage ratio | ||||||

|---|---|---|---|---|---|---|---|

| End 2022 | Baseline 2025 | Adverse 2025 | Delta baseline 2025-2022 | Delta adverse 2025-2022 | End 2022 | Adverse 2025 | |

| Fully loaded | 15.0% | 16.3% | 10.4% | +136 bps | -459 bps | 5.4% | 4.3% |

Ad hoc analysis on unrealised losses on EU banks’ bond holdingsIn parallel with the EU-wide stress test, the EBA also performed an ad hoc analysis of unrealised losses on debt securities at EU banks. The analysis focuses on unrealised losses on banks’ bond positions held at amortised cost. The sample considered is the same as that for the 2023 EU-wide stress test. ‘Held at amortised cost’ is an accounting classification, which allows banks to hold bonds without marking them to market. Banks are expected to hold these bonds until maturity, which has the important implication of allowing banks to reduce the sensitivity of their accounting profit and loss to interest rate changes. EU banks held debt securities (bonds) with a book value of EUR 2.24 trillion as of February 2023. Of these, 59% were held at amortised cost and 41% at fair value through other comprehensive income. Most were bonds issued by governments (66%) and credit institutions (18%). As of February 2023 total unrealised losses on bonds at amortised cost for the banks in the sample considered amounted to EUR 75 billion, compared to almost EUR 78 billion in December 2022. As of February 2023, losses were mitigated by hedges amounting to EUR 38 billion. Unrealised losses on bond holdings began increasing from the end of 2021 in line with increases in interest rates. However, according to these results, unrealised losses on bond holdings in the EU banking sector are currently limited in size compared to the overall solvency and liquidity profile of the banks. Finally, unrealised losses calculated for this ad hoc analysis under the 2023 adverse EU-wide stress test scenario appear manageable overall (net losses amounting to EUR 133 billion). The EBA also started developing a one-off Fit-for-55 climate risk scenario analysis, with the support of the ECB and CAs. This aims to assess the resilience of the financial sector in line with the Fit-for-55 package and to gain an insight into the capacity of the financial system to support the transition to a lower-carbon economy under conditions of stress. More detail on the activities carried out can be found in Section 1.1.6 Implementing the ESG roadmap. |

KPIs

| Indicator | Weight | Short description | Target | Achievements | |

|---|---|---|---|---|---|

| A | Validation of ECB NFCI and NII models | 25% | NFCI and NII to be validated by EBA and NCAs for possible use as top-down projections in 2023 stress test | 100% | 100%

|

| B | Publication of stress test results | 75% | Covers running the actual stress test, methodological updates and publication of results | 100% | 100%

|

See Annex I for details. Source of information: EBA WP monitoring tool and annual report.

Putting data at the service of stakeholders

The EBA further rolled out its Data Strategy, aiming to improve the way regulatory data is acquired, compiled, used and disseminated to relevant stakeholders. It strengthened its analytical capabilities, with a focus in 2023 on enabling the Authority to share data and insights with internal stakeholders and the whole data ecosystem. Leveraging its European Centralised Infrastructure for Supervisory Data (EUCLID) platform allowed for data flows between diverse endpoints and provided internal and external stakeholders with access to high-quality, curated data and insights. This further improved risk analysis and facilitated greater dissemination and disclosure of bank data, including those covered by Pillar 3. It enhanced the EBA’s assessment of the impact of regulatory reforms, improved proportionality and boosted the EBA’s ability to analyse the effects on specific business models, while significantly reducing the need for ad hoc data collection. It also facilitated evidence-based policy analysis in the context of EU-wide debates on regulatory and supervisory matters.

One key target was the collection and dissemination of critical data assets, insights and analytics policies, with priority given to the implementation of the Pillar 3 data hub envisaged by the Level 1 legislation which is currently under development. A discussion paper was published in December explaining the processes and the main challenges that might potentially arise and providing an opportunity for stakeholders to provide input and to take part in a pilot to test the system. The hub will ultimately be connected to the European single access point (ESAP).

EUCLID greatly facilitated preparations for the 2023 transparency exercise published in December 2023, together with the 2023 Risk Assessment Report (RAR). As an integral part of the EBA’s ongoing efforts to foster transparency and market discipline in the EU financial market, and complementing banks’ own Pillar 3 disclosures, as laid down in the CRR, the transparency exercise provided over 1.2 million data points, with on average more than 10,000 data points per bank, and was based on the supervisory data submitted to the EBA via EUCLID.

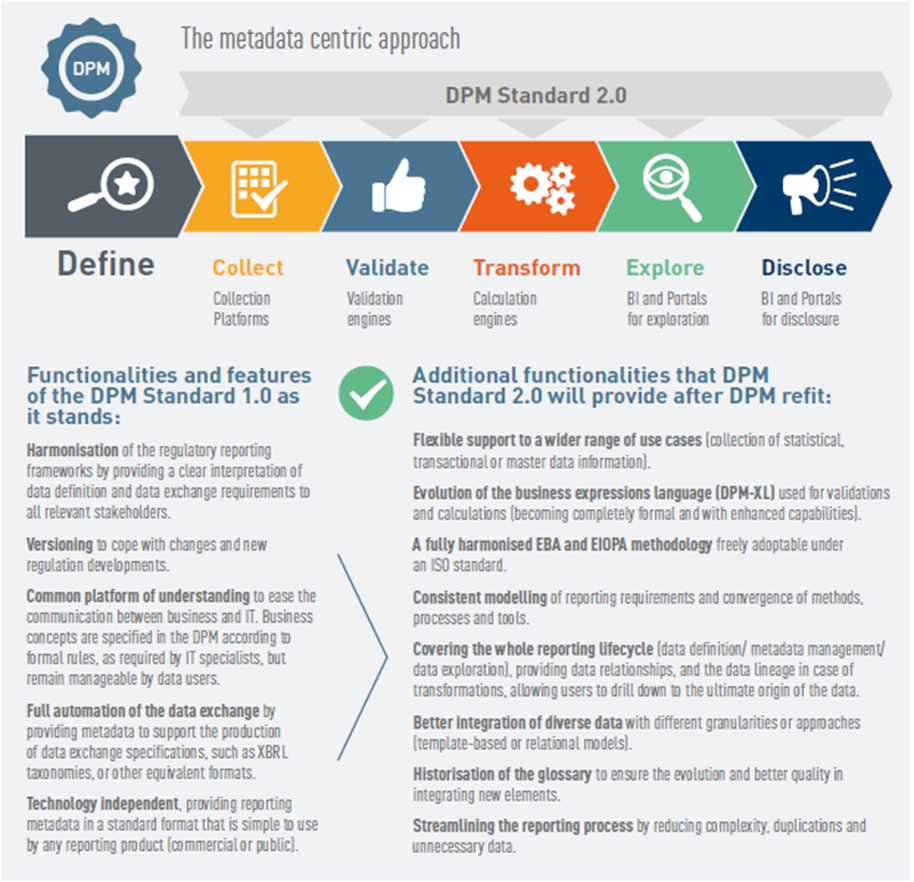

In 2023 the EBA finalised a Data Point Model (DPM) Refit to ensure that the EBA data dictionary is fit for future challenges of reporting and digital processing. A DPM 2.0 standard was published in 2023 and will be implemented during a transitional period of 2024-2025. As part of this effort, the EBA completed the first phase of the migration to the Digital Regulatory Reporting (DRR) tool, DPM Studio, which will support a continuous reporting framework development process, including DPM releases, a full validation rules lifecycle, support for data calculations and creation of eXtensible Business Reporting Language (XBRL) taxonomy packages. Both the DPM Refit and DPM Studio are EBA-EIOPA joint projects.

In the context of its work on reporting and transparency, the EBA continued to map disclosure and reporting frameworks and to consider further proportionality measures in reporting and disclosure in order to achieve a reduction in the reporting burden and in the cost of compliance. These considerations and the Advisory Committee on Proportionality (ACP) recommendations (e.g. introducing simplified reporting for small and non-complex institutions in the new IRRBB reporting and launching a signposting tool for reporting requirements) were also reflected in the different components that the EBA delivered in the course of 2023 in order to complete and update these frameworks, as well as in the work embarked on to address necessary revisions to reporting and disclosure requirements stemming from CRR III and CRD VI.

Work also continued on exploring an integrated reporting framework, thereby contributing to a more consistent and integrated system for collecting statistical, resolution and prudential data with a view to achieving efficiency gains and reducing reporting costs for institutions’ data. The EBA, together with the ECB and national authorities, prepared to establish a Joint Bank Reporting Committee to work together to integrate reporting frameworks and to build a common data dictionary.

The enhancement of the EBA data infrastructure and the improvement of the EU-wide reporting framework leverage input from various stakeholders, in particular from the CAs and the industry, with wide coverage in terms of size and business model. Moreover, the EBA benefits from the latest technological innovations, supporting its work in these areas and helping it to improve its regulatory landscape so as to develop innovative regulatory technology (RegTech) solutions.

DPM 2.0 and the path towards a common data dictionaryWhat is the DPM Standard? The DPM Standard is a key component of the data dictionary used by the EBA and EIOPA to define concepts for the harmonised regulatory data requirements (in the case of the EBA supervisory and resolution reporting) applicable to financial institutions in the EEA. In that sense, the DPM Standard supports experts preparing or using regulatory reporting data by providing a structured representation of the information, identifying all the business concepts and their relations, as well as validation and calculation rules. The EBA and EIOPA have developed the DPM Standard as a public good and as a means to promoting full digital processing of the reporting frameworks. DPM Standard 1.0 has underpinned the reporting frameworks under the remits of both authorities from the beginning and is scalable to further reporting frameworks. Moving from DPM Standard 1.0 to 2.0 In the last decade, the DPM methodology has successfully supported the EBA and EIOPA in integrating their respective regulatory frameworks. After all these years, DPM Standard 1.0 required enhancements in order to remain fit the purpose in terms of responding to changes and reducing costs. DPM Refit is the joint response to the challenge of the increased volume, granularity and complexity of the data, and aims to reap the benefits of closer collaboration and a higher degree of harmonisation. As such, experts from both European supervisory authorities (ESAs) have been working on the DPM Refit project to upgrade DPM Standard 1.0 to DPM Standard 2.0, which provides common data definition standards and tools. What is next? In the longer term, the DPM Standard will play a key role in enabling semantic integration of a single cross-sectoral dictionary for the whole financial sector. As far as the banking sector is concerned, DPM Standard 2.0 should become the single methodology for defining not only the supervisory and resolution reporting already supported by the standard, but also the statistical reporting under the European System of Central Banks statistical integrated reporting framework.  |

KPIs

| Indicator | Weight | Short description | Target | Achievements | |

|---|---|---|---|---|---|

| A | Launch of dissemination portal | 40% | Project to develop infrastructure for dissemination of data and analysis, including with a view to preparing for the Pillar 3 data hub | 100% | 100%

|

| B | DPM Refit | 30% | Implementation of new improved DPM | 100% | 100% Developed but implemented in 2024-2025 |

| C | DRR tools | 30% | Completion of first phase of new DRR tools to support efficient creation and maintenance of the data dictionary relating to reporting requirements (data modelling, validations and transformations, data exchange format generation) | 100% | 100% |

See Annex I for details. Source of information: KPI A: launch of the portal for use by EBA users and CAs; KPI B: publication of DPM Standard 2.0 in June and publication of implementation plan in October 2023; KPI C: launch of DPM Studio in late 2023.

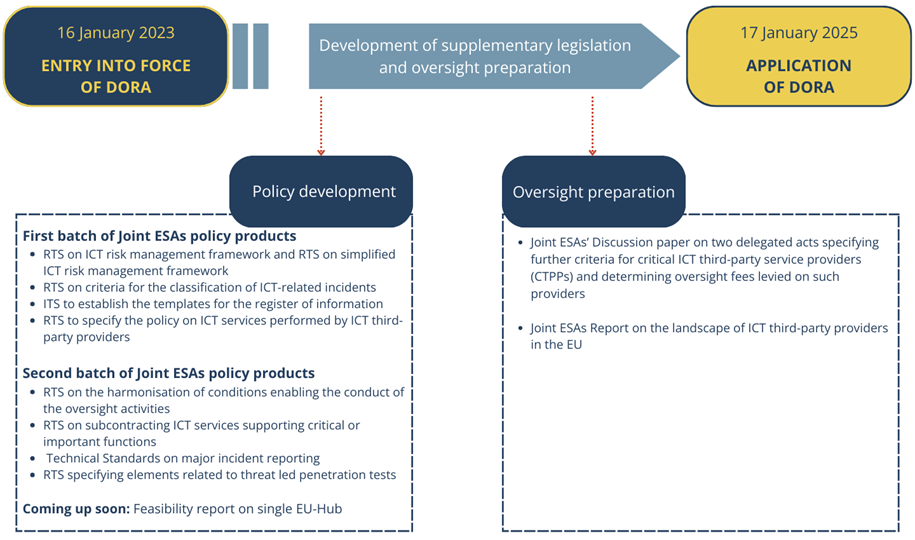

Delivering on digital finance and MiCAR/DORA mandates

The Digital Operational Resilience Act (DORA) entered into force on 16 January 2023 and it will apply from 17 January 2025. The Markets in Crypto-Assets Regulation (MiCAR) entered into force on 29 June 2023 with the date of application ranging from 12 months from entry into force (in the case of issuers of asset-referenced tokens (ARTs) and electronic money tokens (EMTs)) to 18 months following entry into force for other types of activity under MiCAR.

Both legal acts are part of an EU Digital Finance Strategy that aims to ensure that the current legal framework does not pose obstacles to the use of new technologies and products and, at the same time, ensures that such new technologies and products fall within the scope of EU financial regulation and operational risk management arrangements of financial entities. The key priority for the EBA in 2023 was the development of the related policy mandates to supplement the new legal acts.

In relation to DORA, the three ESAs are mandated to jointly deliver 13 legal products by January 2025. Following the groundwork and public consultations carried out in 2023, in January 2024 they published a first series of policies in the areas of information and communication technology (ICT) risk management, ICT third-party risk management and incident reporting. This took into account feedback received from a public consultation, the European supervisory authorities’ (ESAs’) stakeholder groups and the ESAs’ Advisory Proportionality Committee. The ESAs also delivered an interim report in relation to the upcoming implementation of a pan-European systemic cyber incident coordination framework (EU-SCICF).

Policy development for DORA continued with the launch of a second public consultation on policy products in December 2023 in the areas of incident reporting, digital operational resilience testing, ICT third-party risk management and oversight over critical ICT third-party providers (TPPs) (four sets of draft RTS, one set of draft ITS and two sets of guidelines). Publication of the final documents is scheduled for 17 July 2024.

In parallel with policy development, the ESAs also started preparing for the upcoming implementation of the pan-European oversight framework of ICT third-party service providers designated as critical (CTPPs). Among other things this includes:

- ongoing and enhanced engagement with relevant stakeholders carried on throughout the year, such as EU and third-country supervisory and oversight authorities as well as EU financial entities and ICT service providers;

- the establishment of a High-Level Group on DORA Oversight in December 2023 which involves CAs in the design of the oversight framework and the establishment of procedures, methodologies and governance documents;

- data collection on the ICT TPP landscape in the EU – the results of the exercise were published by the ESAs on 27 September 2023;

- the development of necessary IT tools to support the oversight activities as well as the ICT-related incident framework.

In September 2023, the ESAs published technical advice on the criticality criteria for the designation of CTPPs and on the oversight fees as a response to the Commission’s CfA.

Figure 5: Regulatory products and reports under the DORA mandate

For MiCAR, the EBA is responsible for delivering 20 technical standards and guidelines in all but one case within 12 months from entry into force (i.e. by the end of June 2024). Two of the mandates are joint with ESMA, and one is joint with ESMA and EIOPA. Again, substantial preparatory steps were taken to meet this challenge and the EBA launched Consultation Papers on the vast majority of its draft technical standards and guidelines in 2023:

- in July, the EBA issued its first consultation package on EU market access for issuers of ARTs and on complaints handling procedures;

- in October, the EBA issued its second consultation package on the procedure for the approval of white papers of ARTs issued by credit institutions, governance arrangements under the remuneration policy, internal governance arrangements, and on joint EBA-ESMA guidelines on suitability assessments of the management body and holders of qualifying holdings;

- in November and December, the EBA issued its third consultation package on supervisory colleges, reporting of transactions in ARTs and EMTs denominated in a non-EU currency, recovery plans for issuers of ARTs and EMTs, own funds requirements and stress testing of issuers under MiCAR, liquidity requirements and on stress testing of relevant issuers, on the requirements for policies and procedures on conflicts of interest for issuers of ARTs;

- in September 2023, the EBA also responded to the Commission’s CfA on significance criteria for ARTs and EMTs and supervisory fees to be charged to issuers.

As required in connection with the preparatory steps for the supervision tasks assigned to the EBA (with respect to significant ARTs and significant EMTs), the EBA started to develop supervisory models, policies and procedures, as well as templates for the exchange of information between all relevant parties (including issuers, national competent authorities (NCAs), the ECB and other relevant central banks). In addition, an EBA Crypto Supervision Coordination Group was established, which brings together high-level representatives from EEA NCAs, the ECB and ESMA to discuss practical issues regarding the supervision of issuers of ARTs/EMTs and to foster convergence of supervisory practices in view of MiCAR applying to ART/EMT issuers from June 2024.

Finally, in view of the fast-approaching application date, and the finalisation of the associated technical standards and guidelines, the EBA stepped up its actions to encourage the industry and supervisors to sharpen their focus on consistent and timely implementation. In particular, in July 2023 the EBA published a statement with ‘guiding principles’ to which issuers of ARTs and EMTs are encouraged to pay due regard by the application date. The principles are intended to facilitate early alignment with the rules established by MiCAR, for instance as regards the fair treatment of potential acquirers and holders of ARTs and EMTs, and sound governance and effective risk management.

The EBA also continued to monitor financial innovation and to identify areas where a further regulatory or supervisory response may be needed. Crypto-assets, tokenisation, decentralised finance, digital identity management and the application of artificial intelligence / machine learning, as well as digital platforms, supervisory and regulatory technologies (SupTech and RegTech) are examples of innovative applications on which the EBA focused during the year. As Chair of the European Forum for Innovation Facilitators (EFIF) in 2023, the EBA coordinated the delivery of the EFIF WP, including thematic publications on innovation facilitators and BigTechs which also contain related recommendations. In particular, the joint ESAs Report on innovation facilitators published in December 2023 recommends steps to improve the activities of innovation facilitators, such as innovation hubs and regulatory sandboxes, while the report on the 2023 stocktake on BigTech direct financial services provision in the EU, published in early February 2024, recommends steps to enhance the monitoring of these activities.

Finally, the EBA, together with ESMA and EIOPA, guided and steered development of the EU Supervisory Digital Finance Academy (SDFA) training curriculum to ensure it is tailored to the CAs’ needs and contributes to the SDFA’s aim to strengthen supervisory capacity in innovative digital finance.

KPIs

| Indicator | Weight | Short description | Target | Achievements | |

|---|---|---|---|---|---|

| A | Percentage of mandates under MiCA to be submitted to the Commission in 2024 and to be consulted on in 2023 | 35% | Under current assumptions, the EBA will be mandated to deliver to the Commission approx. 20 technical standards and guidelines in 2024 | 100% | 95% All but one CPs were delivered in 2023 |

| B | Percentage of mandates under DORA published and submitted to the Commission in 2023 | 35% | Under current assumptions, DORA will confer 13 joint mandates for technical standards and guidelines on the ESAs, of which 5 are to be delivered in 2023 | 100% | 100% All CPs / final products were delivered as planned |

| C | Operational readiness to take up new tasks in relation to DORA and MiCA | 10% | The EBA may be given new tasks as part of the DORA and MiCA proposals and should be ready to take up tasks (supervision/oversight etc.) effectively and efficiently | EBA is implementing its operational readiness plan | Implementation of operational readiness plan on track |

| D | Number of thematic publications, incl. opinions or reports, provided to the Commission and NCAs to build knowledge, promote convergence and identify regulatory gaps or obstacles relating to financial innovation | 10% | The EBA has a mandate to monitor innovations and regularly issues recommendations to NCAs and/or the Commission | Up to two thematic publications (opinions or reports) | Achieved two publications |

| E | Percentage of reviewed and quality-assured training curriculum of the Digital Finance Academy to ensure it is tailored to the CAs’ needs | 10% | The EBA, together with ESMA and EIOPA, will guide and steer development of the Academy’s training curriculum to ensure it is tailored to the CAs’ needs | 100% | 100% |

See Annex I for further details. Source of information: KPI A, B: and D: EBA WP monitoring tool and publications, KPI C: DORA /MiCAR milestones tracker, KPI E: internal ESA report to DG Reform.

Enhancing capacity to fight money laundering and terrorist financing in the EU

In 2023, the EBA continued to lead, coordinate and monitor the EU financial sector’s fight against money laundering/terrorist financing (ML/TF) in line with its legal mandate, by setting common standards, fostering cooperation and supporting the implementation of robust approaches to tackling financial crime risks across the EU.

The EBA built on its comprehensive regulatory framework to address emerging risks by issuing new guidelines, updating existing guidelines and contributing to a holistic approach to anti-money laundering and countering the financing of terrorism (AML/CFT) to ensure that ML/TF risks are considered across all areas of supervision. In 2023, tackling unwarranted de-risking, ensuring compliance with restrictive measures and building robust approaches to AML/CFT for crypto-asset service providers (CASPs) and their CAs were particular areas of focus.

Tackling ML/TF risk can have unintended consequences. For example, it can make access to financial services difficult for vulnerable customers who are unable to provide standard forms of identification. This is why, in March 2023, the EBA published two guidelines on how institutions can manage ML/TF risk effectively, rather than de-risk, in situations where access by customers to financial products and services should be safeguarded. These guidelines build on the EBA’s 2022 Opinion on de-risking, the EBA’s 2016 Opinion on the application of customer due diligence measures to customers who are asylum seekers from higher-risk third countries or territories and on the statement the EBA issued in April 2022 in the context of the war in Ukraine. The EBA also published a factsheet, together with the Commission, to help not-for-profit organisations understand what information they might have to provide to open an account or to carry out a specific transaction.

The war in Ukraine highlighted the challenges associated with divergent approaches to complying with EU restrictive measures. The EBA found that significant differences exist in relation to the quality of institutions’ systems and controls to comply with restrictive measures and supervisors’ expectations of those systems and controls. Together, these differences undermine the effectiveness of the EU’s restrictive measures or regimes and affect the stability and integrity of the EU’s financial system. To address this, the EBA used provisions in Regulation (EU) 2023/1113, the CRD and the PSD to propose two new guidelines. One set of draft guidelines sets common, regulatory expectations regarding the role of senior management, internal governance arrangements and risk management systems in the restrictive measures context. A second set of draft guidelines sets out what payment service providers (PSPs) and CASPs should do to be able to comply with restrictive measures when performing transfers of funds and crypto-assets and focus on know-your-customer, screening and due diligence measures.

Throughout 2023, the EBA supported the development of common approaches to tackling ML/TF risks associated with CASPs and other entities under the MiCAR framework. This included guidance on the AML/CFT supervision of CASPs; guidance to CASPs and financial institutions that service CASP customers on assessing ML/TF risks and putting in place commensurate and risk-sensitive measures to manage those risks; and setting common expectations on managing ML/TF risks at market entry and throughout a MiCAR institution’s life cycle. The EBA also consulted on revisions to its Transfer of Funds (‘Travel Rule’) Guidelines, which it amended and extended to apply to transfers of crypto-assets going forward. The public consultation on these guidelines closed in February 2024.

The EBA continued to foster supervisory cooperation by supporting information exchange and by continuing to develop the AML/CFT colleges framework.

By December 2023, more than 260 AML/CFT colleges had been set up. The EBA staff actively monitored 18 of these colleges and supported their effective functioning through contributions, feedback and the negotiation of draft terms of participation with key third-country observers. A report summarising the EBA’s observations was published in August 2023 and found that CAs had taken important steps to improve the functioning of AML/CFT colleges, although many colleges had not reached full maturity. The report further identified good practices that will be useful for CAs to improve the effectiveness of AML/CFT colleges and consequently, of supervisory outcomes. In December 2023, the EBA staff launched the latest round of thematic college monitoring, focusing on neobanks and payment or electronic money institutions with a similar business model.

In addition to its college work, the EBA brought together CAs to share information and establish cooperation gateways in situations where cross-border ML/TF risks had crystallised but no AML/CFT college existed. This was the case, for example, in relation to a number of CASPs.

Throughout 2023, the EBA continued to support the implementation of robust approaches to tackling financial crime risks across the EU by identifying and disseminating information on ML/TF risks, by monitoring the implementation of its standards by CAs and issuing recommendations for improvements as necessary, and by contributing to the effective design of the EU’s new legal and institutional AML/CFT framework.

In July 2023, the EBA published the fourth Opinion on the risks of money laundering and terrorist financing affecting the European Union’s financial sector. The EBA issued this opinion against the background of a changed risk landscape, which had impacted institutions’ AML/CFT compliance efforts and CAs’ approaches to AML/CFT supervision. The war in Ukraine and the growth in CASP activity stood out in particular. For the first time, the EBA used data from its new central database on anti-money laundering and countering the financing of terrorism (EuReCA) to inform its analysis.

Data from EuReCA also informed the EBA’s analysis of ML/TF risks associated with payment institutions. The EBA found that these risks were not assessed or managed effectively in all cases and that AML/CFT internal controls in payment institutions were often insufficient to mitigate inherent ML/TF risks, which were often high. The EBA’s findings also suggest that not all CAs were doing enough to supervise the sector effectively. To address this, the EBA hosted discussions and roundtables with industry representatives and supervisors to identify a way forward, and provided technical advice to the Commission and co-legislators to inform the nascent payment services framework.

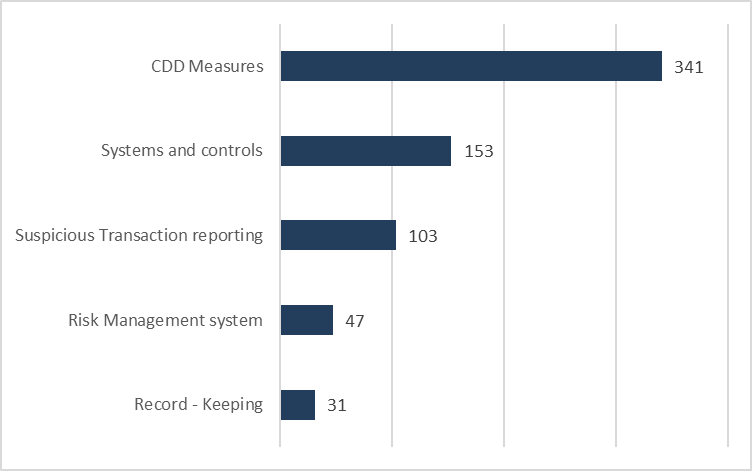

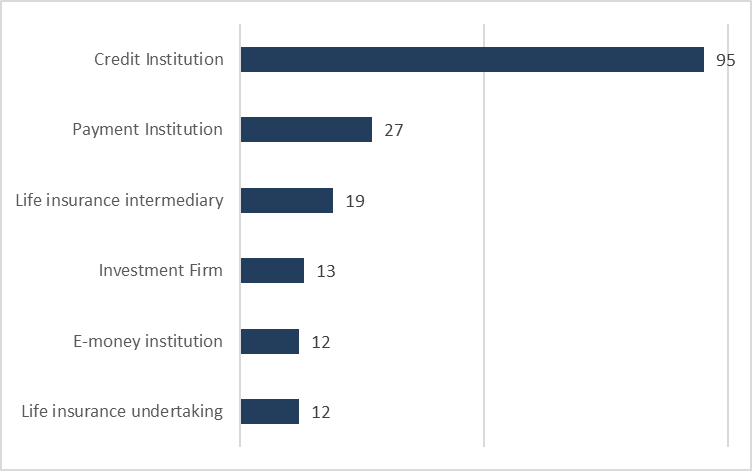

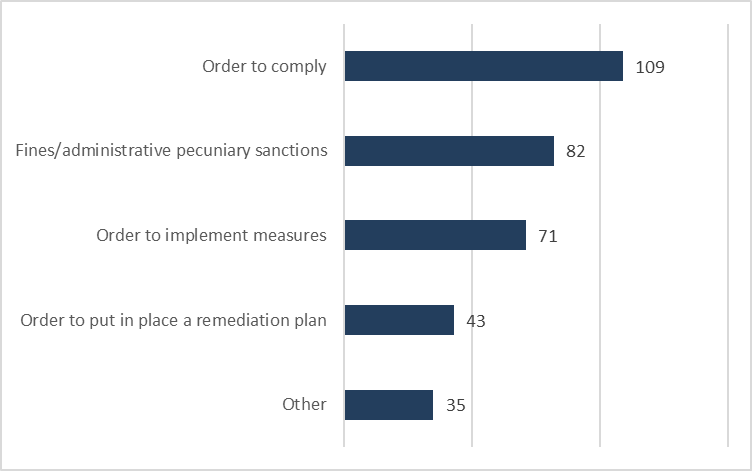

EuReCAEuReCA is the EBA’s AML/CFT database on serious AML/CFT deficiencies in individual financial institutions in the EU, which was launched in 2022. Between January and December 2023, the majority of reports related to credit institutions, followed by payment institutions. CAs found the largest number of deficiencies in respect of institutions’ Customer Due Diligence measures. Figure 6: areas where material weaknesses occur  Figure 7: Key EuReCA numbers  The EBA has used EuReCA data to support different AML/CFT work streams, namely the AML/CFT implementation reviews and the monitoring of AML/CFT colleges, to inform different AML/CFT deliverables, including the Opinion on ML/TF risks affecting the EU financial sector and the EBA Report on ML/TF risks associated with payment institutions, and to feed into the EBA's periodical Risk Dashboard and the EBA's Risk Assessment Report. The EBA staff have also shared information from EuReCA with other CAs, either at their request or at the EBA’s initiative; with ESMA and EIOPA, on a monthly basis, where information concerns entities under their scope; and with the lead supervisor of an AML/CFT college, where information concerns entities within the group. Figure 8: top 5 sectors where material weaknesses are identified  Figure 9: top 5 types of measures  |

The EBA continued its staff-led, in-depth assessments of CAs’ approaches to AML/CFT supervision. It published a report on aggregate findings and a summary of recommendations issued during its third round of reviews in July 2023, and concluded that supervisors were making progress in the fight against money laundering and terrorist financing, but most needed to do more to ensure that their approach was effective and enabled them to tackle ML/TF risks in their sector. The EBA launched its fourth, and final, round of reviews in 2023. Over the course of that year, staff assessed and provided comprehensive feedback to 11 CAs from 5 Member States. By the end of 2024, all CAs that are responsible for tackling ML/TF risk in the EU’s banking sector will have been assessed.

Finally, throughout 2023, the EBA contributed to shaping the new AML/CFT framework. As part of this, the EBA provided technical advice to the Commission and the co-legislators as necessary. It also worked to prepare a smooth hand-over of those aspects of its work that relate exclusively to AML/CFT compliance and supervision to the Anti-Money Laundering Authority (AMLA) that has been set up.

The Forum of EU AML/CFT supervisors on the transition to AMLASince the establishment of AMLA will bring significant changes to the way CAs approach AML/CFT supervision, the EBA has set up a Forum of EU AML/CFT supervisors to support them in the transition to AMLA and to the new EU AML/CFT framework. The Forum provides a space for discussion and information exchange, focusing on the practical aspects of the transition. Its objective is to contribute to the smooth transition to the new institutional framework, in particular by:

The first Forum took place in October and has met every six weeks since. In addition to the Forum, and throughout 2024 and 2025, the EBA will work with CAs to advise the Commission on key aspects of the new regime, including in relation to the methodology supervisors will use to assess ML/TF risks. |

KPIs

| Indicator | Weight | Short description | Target | Achievements | |

|---|---|---|---|---|---|

| C | Capacity to identify, analyse and disseminate information on ML/TF risks | 25% | The EBA will identify, assess and disseminate information about ML/TF risks based on, inter alia, information from EuReCA. The EBA will also publish the fourth Opinion on ML/TF risk under Art 6(5) of the AMLD. | Analysis and dissemination of information in EuReCA, ad hoc and upon reasoned request One opinion | Achieved Two opinions

|

| D | Contributing to the implementation of a holistic approach to tackling financial crime | 25% | The EBA will deliver mandates under the 2022 Fund Transfers Regulation. It will also continue its work on de-risking and access to the financial system. | Up to four guidelines or amendments to existing guidelines | Achieved

|

| E | Effective AML/CFT supervision – number of implementation and thematic reviews | 30% | The EBA will assess CAs’ approaches to AML/CFT supervision, with bilateral feedback and action points. It will also monitor AML/CFT colleges. | One thematic review; up to four implementation reviews | Achieved

|

| F | Preparing for the smooth transfer of powers to AMLA | 20% | The EBA will prepare to hand over those aspects of its work that relate exclusively to AML/CFT that will fall within AMLA’s remit. | Transition plan | Execution of plan on track |

See Annex I for further details. Source of information: KPI C, D and E: EBA WP monitoring tool and publications, KPI F: internal project plan.

Implementing the ESG roadmap

As a horizontal priority, the EBA paid particular attention to aspects relating to environmental, social and governance (ESG) matters being reflected in its work in accordance with the roadmap on sustainable finance published in December 2022.

Figure 10: The roadmap explains the EBA’s sequenced and comprehensive approach over the next three years to integrating ESG risk considerations into the banking framework and supporting the EU’s efforts to achieve the transition to a more sustainable economy.

In 2023, the Authority continued to deliver on mandates included in the CRD, CRR, IFD, IFR, EBA Founding Regulation and those stemming from the Commission’s action plan and Communication Strategy for Financing the Transition to a Sustainable Economy, and pursued its contributions to European and international work (particularly via the Platform on Sustainable Finance, Basel Committee, Network for Greening the Financial System, European Systemic Risk Board (ESRB)).

In line with the EBA’s ESG roadmap, the Authority continued the investigation and potential review of the current framework for the prudential treatment of exposures to capture environmental and social risks. The EBA follows a sequenced approach, in accordance with its legal mandates. To mark the completion of the first phase of this work the EBA published a report in October 2023 on the role of environmental and social risks in the prudential framework for credit institutions and investment firms. Taking a risk-based approach, the report assesses how the current prudential framework captures environmental and social risks and puts forward targeted enhancements to accelerate the integration of environmental and social risks across Pillar 1. The proposed enhancements aim to support the transition towards a more sustainable economy, while contributing to the stability, resilience and orderly functioning of the financial system.

In the report the EBA also puts forward recommendations for short-term actions to be taken over a three-year horizon as part of the implementation of the revised Capital Requirements Regulation and Capital Requirements Directive (CRR III / CRD VI). Taking a medium-to-long-term perspective, the report also presents possible revisions to the Pillar 1 framework – subject to monitoring and further assessment – reflecting the growing importance of environmental and social risks. Alongside other policy initiatives outside the prudential framework, the EBA continues to consolidate the integration of environmental and social risks across all pillars of the regulatory framework.

With regard to Pillar 2 requirements, the EBA continued its efforts to incorporate ESG considerations into risk management and supervisory guidance in a proportionate and gradual manner.

In January 2024 the EBA published a Consultation Paper on draft guidelines on the management of ESG risks with due consideration of the ACP recommendations. The draft guidelines, which are expected to be finalised in the course of 2024, set out requirements for institutions for the identification, measurement, management and monitoring of ESG risks, including through plans aimed at addressing the risks arising from the transition towards a climate-neutral EU economy.

In terms of disclosures and transparency, the ESAs also embarked on work to review principal adverse impact (PAI) indicators and financial disclosures in the Sustainable Finance Disclosure Regulation (SFDR), in response to a request from the Commission. Overall, the draft RTS proposes the extension of the list of social indicators for principal adverse impacts, refinement of the content of several of the other indicators for adverse impacts and their respective definitions, applicable methodologies, metrics and presentation, and amendments regarding decarbonisation targets. Further proposed changes, based on stakeholder Q&As and observations, cover the Do No Significant Harm disclosure design options and the simplification of the templates, among other technical changes.

Further assistance to the Commission in its next comprehensive assessment of the SFDR was provided in the ESAs’ second annual report, published in September 2023, on the extent of voluntary disclosure of principal adverse impacts under the Article 18 of the SFDR. In a similar way to the previous publication in 2022, the report presented the findings from a survey of NCAs in order to assess the state of entity-level and product-level voluntary PAI disclosures under the SFDR. The report also includes a preliminary, indicative and non-exhaustive overview of good practice and of areas offering room for improvement.

Also in the context of disclosures, the set of draft RTS were published by the ESAs in May 2023 on the ESG impact disclosure for simple, transparent and standardised (STS) securitisations under the Securitisation Regulation, which aims to help market participants make informed decisions about the sustainability impact of their investments on sustainability disclosures on STS securitisation.

As a further contribution to the EU’s wider objectives in sustainable finance, the EBA, ESMA and EIOPA published separate progress reports in June 2023 on greenwashing in their respective remits in the financial sector. In these reports, the ESAs put forward a common high-level understanding of the greenwashing applicable to market participants across their respective remits – financial markets, banking, and insurance and pensions.

The EBA progress report, more specifically, provides an overview of the greenwashing phenomenon in the banking sector and its impact on credit institutions, investment firms and payment service providers. The outcome of the quantitative analysis of the greenwashing phenomenon shows a clear increase in the total number of potential cases of greenwashing across all sectors, including for EU banks. It also indicates rising climate accountability: increased public attention directed towards climate change has led companies to be held more accountable for their environmental policies, climate impact and disclosures.

These progress reports came as an initial response to the Commission’s request for input on the topic.

The final reports are expected to be delivered in May 2024 and will put forward recommendations, possibly along with suggestions for changes to the EU regulatory framework.

As another piece contributing to the ESG roadmap, the EBA responded to the Commission’s CfA on green loans and mortgages. The report (and opinion) published in December 2023 advises the Commission to consider introducing a voluntary EU label for green loans based on a common EU definition, as well as the integration of the concept of green mortgages and their key sustainability features into the Mortgage Credit Directive (MCD). The EBA’s response includes an overview of green lending and associated practices in the EU banking sector, and outlines issues identified in the green loans market.

Furthermore, the EBA devoted substantial resources in 2023 to preparing for the one-off Fit-for-55 climate risk scenario analysis, to be conducted jointly by the ESAs, the ECB and the ESRB in accordance with the Commission request of 8 March 2023 and in line with the Commission Communication Strategy for Financing the Transition to a Sustainable Economy. The scenario analysis aims to assess the resilience of the financial sector in line with the Fit-for-55 package, and to gain insights into the capacity of the financial system to support the transition to a lower-carbon economy under conditions of stress.

One milestone to note here, after a public consultation in July 2023 on draft templates, is the launch of a data collection exercise (at the beginning of December) for gathering climate-related data from EU banks for the Fit-for-55 exercise. The data collection exercise seeks to gather climate-related and financial information on credit risk, market risk and real estate risks, at aggregated and counterparty level, as of December 2022. While aggregated data will provide information on the climate-related risks of the banking sector more broadly, counterparty-level data will enable the assessment of concentration risk for large climate exposures, capturing amplification mechanisms and assessing second-round effects.

The EBA is also considering developing a regular climate stress testing framework, with a focus at first on the development of methodologies, data and scenarios. A dedicated subgroup will work on this task.

Similarly, work on a framework to allow for effective monitoring of ESG risks in the banking sector and the green financial market is envisaged, but this had to be deprioritised owing to resource constraints. Ideally, such a framework could benefit from a gradual increase in external ESG risk-relevant data, with a focus on climate change-related risks.

KPIs

| Indicator | Weight | Short description | Target | Achievement | |

| A | Contribution to the renewed Sustainable Finance Strategy | 60% | Number of ESG related technical standards, guidelines, reports and responses to CfA stemming from the mandates in the CRD, CRR, IFD, IFR and from the Commission’s renewed Sustainable Finance Strategy delivered on time | 80% | 86% Seven mandates delivered in 2023, one of which was delayed |

| B | Implementation of one-off Fit-for-55 climate risk scenario analysis | 40% | Preliminary work on the one-off Fit-for-55 climate risk scenario analysis in accordance with the Commission’s renewed Sustainable Finance Strategy | Development of one-off Fit-for-55 climate risk scenario analysis | Data collection launched in December 2023

|

See Annex I for further details. Source of information: KPI A and KPI B: EBA WP monitoring tool and publications.

NB: KPI B was adopted after the finalisation of the 2023 Work programme.

Additional achievements in 2023

Risk assessment

Along with the stress tests, the EBA has a responsibility to identify and analyse trends, potential risks and vulnerabilities in the banking sector. This not only helps ensure the orderly functioning and integrity of financial markets, but also contributes to the stability of the financial system in the EU.

Following on from 2022, the EBA continued to pay particular attention to risks stemming from the Russian invasion of Ukraine and the crisis in the Middle East, the jitters in the financial markets in early 2023, mainly in the US banking sector and in Switzerland, high inflation, lacklustre economic growth and increasing interest rates, all of which posed challenges not only for the banking sector, but also for households and corporates. The deterioration in the macroeconomic outlook gave rise to uncertainty, requiring the EBA, in conjunction with CAs and other EU institutions, to adjust its focus for 2023. The Authority addressed topics such as unrealised losses on EU/EEA banks’ bond portfolios held at amortised cost, the impact of rising rates on EU/EEA banks and leveraging banks’ IRRBB data.

Findings from the above and many other findings were reflected accordingly in various deliverables such as the quarterly risk dashboard and the Joint Committee (JC) spring and autumn risk reports. In December 2023, the EBA published the results of the 2023 EU-wide transparency exercise and its annual RAR.

The RAR highlighted the following:The EU banking sector proved to be resilient in the aftermath of the US banking turmoil in March. Capitalisation remained high with an average CET1 ratio at its highest reported point (16%). Underlying profitability supported banks’ payouts. Figure 11: Key findings of the 2023 Risk Assessment Report

Elevated interest rate levels have so far supported widening interest margins, but this might have reached its turning point. Asset quality remained robust, yet subdued economic growth and elevated interest rate levels create pockets of risk going forward. Liquidity remained high but it started normalising from its highest levels connected with the pandemic. Market funding costs have increased in line with interest rates, yet deposit rates have remained comparatively low, though they might rise going forward. Operational risk – including cyber risk – has continued its rise, not least driven by geopolitical tensions. Climate-related and broader ESG risks are increasingly in banks’ focus. |

In June 2023 the EBA published a report assessing the potential impact on LCR and NSFR levels of the upcoming central bank funding repayment, as well as a potential scenario of higher liquidity risk, particularly affecting government bonds, derivatives and repo markets in the context of a higher interest rate environment, inflation and recession risks. The EBA also continued monitoring banks’ asset encumbrance and funding plans situation and published two thematic reports in July. The Asset Encumbrance Report highlighted further limited use of central bank funding in 2022 and an overall lower encumbrance ratio (decreased by 3.3 percentage points to 25.8% in December 2022). The Funding Plans Report showed that banks plan to issue more debt instruments to counterbalance an expected further decline in central bank funding.

In January 2024 the EBA published its heat map following scrutiny of the IRRBB. It contains specific short, medium and long-term targets for the EBA in terms of monitoring the impact on institutions from increases in interest rates and developments regarding institutions’ ability to manage the risks.

Recovery and resolution

In early July 2023 the EBA also published the final guidelines on overall recovery capacity (ORC), aimed at establishing a consistent framework for the determination of the ORC by institutions in their recovery plans and the respective assessment by CAs. The main objective here was to harmonise, with appropriate consideration of proportionality aspects, the observed practices for ORC determination and assessment, to improve the usability of recovery plans and to make crisis preparedness more effective.

In the context of crisis preparedness, the EBA monitored evolving practices in relation to recovery planning, focusing in particular on improving the usability and the operationalisation of plans, which was included as a key priority in the European Supervisory Programme for the year 2024 with an enhanced focus on liquidity recovery options in order to cater for the macroeconomic trends that materialised in 2023.

On the topic of resolution, the EBA continued to monitor convergence in the implementation of identified issues within the resolution framework through the European Resolution Examination Programme (EREP) exercise. Monitoring the build-up of MREL resources in the European banking sector continued following the latest report published in early 2023, and it covered with increased frequency the relevant trends in the context of the quarterly MREL dashboard.

Payment services

In the course of 2023, the EBA continued to help make retail payments across the EU efficient, secure and easy to use, by contributing to the common interpretation, application and supervision of relevant EU directives and EBA technical standards and guidelines.

The peer review published in early 2023 of the authorisation of payment institutions and e-money institutions under the revised Payment Services Directive (PSD2) was a key deliverable in that respect. Following 10 months of analysis, the review concluded that there is increased transparency and consistency of the information required in the authorisation process as a result of the directive and the guidelines that the EBA issued in support. However, the review also identified significant divergences in CAs’ assessment and the degree of scrutiny applied to the applications received. The review report therefore set out a series of measures addressed to CAs, to address such divergences, to level out the supervisory playing field, and to mitigate against ‘forum shopping’.

Following the delivery of the EBA’s response in June 2022 to the Commission’s CfA regarding the review of PSD2, the EBA did not publish any additional legal instruments under PSD2, but instead continued to support the Commission in the run-up to the publication in June 2023 of its proposals for a revised Payment Services Directive (PSD3), a new Payment Services Regulation, and a new Regulation on Open Finance (Financial Data Access (FIDA)). The proposals envisage around 35 mandates to be conferred on the EBA for estimated delivery between 2025 and 2027.

As a follow-up to a discussion paper that the EBA published in February 2022, the EBA also continued to assess payment fraud data that more than 6,000 payment service providers initially submitted to their NCAs in compliance with Article 96(6) of PSD2 and the supporting EBA guidelines (EBA/GL/2018/05), which then submitted aggregations of the data to the EBA. Analysis of such data is key to understanding the extent to which the security requirements the EBA developed in previous years, in particular strong customer authentication (SCA), have achieved the envisaged aim of reducing payment fraud. However, the EBA is of the view that the quality of the data remains insufficient for publication and instead established measures to enhance the quality so as to publish an improved set of data in mid-2024.

Consumer and depositor protection

During 2023, the EBA continued its efforts to enhance the supervision of financial institutions’ retail conduct across its regulatory and supervisory remit and to apply its depositor protection expertise to topical questions raised by the Commission and legislators.

With regard to the former, the Authority fulfilled for the first time the new ESA mandate to coordinate mystery shopping activities of NCAs; the findings were published in August 2023. The exercise, which focused on personal loans and payment accounts, confirmed that mystery shopping is a tool that adds value to the supervision of financial institutions by NCAs. It is complementary to other more conventional tools or approaches, and delivers first-hand information about, and insights into, the conduct of financial institutions towards consumers.

To allow for a robust identification of causes of potential harm to consumers, the EBA also developed for the first time a set of ‘retail risk indicators’, which were published in March 2023. The indicators cover a wide variety of different types of products within the EBA’s remit (e.g. mortgage credit, consumer credit, deposits, payment accounts and payment services). They aim to show possible risks to consumers arising from the misconduct of financial institutions offering retail banking products in the EU, and from wider economic conditions, and will complement other sources of information that the EBA already uses to decide on its consumer protection priorities.

As part of the Authority’s role in promoting transparency, simplicity and fairness in the market for consumer financial products or services across the internal market, the EBA also coordinates financial literacy and education initiatives undertaken by national authorities. To that end, the EBA, in conjunction with the other ESAs, published factsheets on inflation and the rise in interest rates (published in May 2023) and on financial education and sustainable finance (published in November 2023). The factsheets were developed in easy-to-understand language, translated into all official EU languages, and reproduced by national authorities on their respective websites.

In April 2023, the Authority also published the eighth edition of its biennial Consumer Trends Report (CTR), in which it summarised trends observed for the products and services under the EBA’s consumer protection mandate and identified two issues that consumers are currently facing and that will shape the EBA’s consumer protection priorities over the subsequent two years: fraud in retail payments, and over-indebtedness and arrears.

As regards the development of regulatory mandates and products, two public consultations in the context of the Credit Servicers Directive (CSD) are noteworthy.

- In July 2023, draft guidelines on the establishment and maintenance of national lists or registers of credit servicers, specifying the types of information that the national lists or registers have to include, in order to enhance transparency for credit purchasers and borrowers and to bring about a level playing field across the Union.

- Also in July 2023, draft RTS on complaints handling procedures for issuers of ARTs under the MiCAR, which the EBA developed in close cooperation with ESMA.

- In November 2023, draft guidelines on complaints handling by credit servicers, which extend to credit servicers the same requirements under the existing Joint Committee guidelines on complaints handling that applied for nearly a decade to tens of thousands of financial institutions in the banking, investment and insurance sectors. The requirements pertain to firms’ complaints management policy, their complaints management function, registration, reporting, internal follow-up and the provision of information, and procedures for responding to complaints.

- Finally, in response to the European Commission’s proposed amendments to the draft Technical Standards on crowdfunding service providers, the EBA issued an Opinion noting the importance of ensuring that crowdfunding service providers can access historical data to improve the assessment of creditworthiness and the performance of their scoring models.

Within the remit of ensuring the consistency and effectiveness of supervisory actions and outcomes, in 2023 the EBA undertook its first peer review on conduct and consumer protection issues, and more specifically on the supervision of creditors’ treatment of mortgage borrowers in arrears under the MCD. The peer review report was developed against the economic conditions and high interest rate environment at the time, published in December 2023, and found that CAs’ supervision is effective overall and has been adapted to reflect said interest rate environment.

However, the review also found differences in the level of scrutiny that CAs apply to mortgage creditors, including the identification of risks that borrowers are facing. The report sets out some follow-up measures, both for individual and named CAs and for CAs more generally, to ensure that supervisory measures to mitigate consumer detriment are taken before the detriment materialises. The report also sets out some examples of best practice in this area that will be of benefit for other CAs to adopt.

As part of its responsibilities in the field of depositor protection, the EBA continued to contribute to the enhancement of the rulebook, among other things, by way of the February 2023 revision of its guidelines on methods for calculating contributions to deposit guarantee schemes (DGSs). The revised guidelines further strengthen the link between the riskiness of a credit institution and how much it needs to contribute to the DGS funds that will be used to reimburse depositors in the event that their bank fails.

Furthermore, in order to contribute to the review of the existing DGSD in response to a CfA from the Commission, in December 2023 the EBA published a report on the deposit coverage level and coverage of public authorities’ deposits. Based on a quantitative analysis and simulation, the report concludes that a potential change to the current coverage level of EUR 100,000 would have a positive but limited impact on financial stability and depositor protection, while being costly and having a somewhat negative impact on moral hazard. The analysis also revealed that the extension of coverage to public authorities’ deposits would have a limited impact on the industry, mainly because there are relatively few public authorities in comparison to the overall number of depositors across the EU.

Acting as a hub for DGS data collection and analysis, the EBA regularly publishes data on DGS across the EEA, and in April 2023 it provided its most recent update. The data covered two key concepts and indicators, namely available financial means and covered deposits, and indicated that, in the period from 2021 to 2022:

- the number of deposits protected by EU DGS increased by 2.5%, while the amount of funds available to protect those deposits in the event of bank failures increased by 7.4%;

- DGS are gradually increasing their available funds raised from the industry with the aim of reaching the harmonised minimum target level of 0.8% of deposits covered by the DGS by July 2024;

- half of the 36 DGS in the EEA have already reached the minimum target level ahead of the deadline.

Equivalence

In the context of its work on third-country equivalence, the EBA is assessing the regulatory and supervisory frameworks of third countries and their equivalence with the EU framework by providing opinions to the Commission.

In line with a roadmap on equivalence work developed in 2022, the EBA established a Network on Equivalence that supports the assessments of individual third countries and furthermore assists in the overhaul of the EBA’s monitoring methodology.

At the same time, the Authority, in conjunction with the Commission, monitored the ongoing equivalence of countries covered by the Commission’s decisions and reported back to the EU institutions.

Supervisory convergence and independence

Mediation between the Spanish and the Belgian deposit guarantee schemes

The EBA was requested to settle a disagreement between two DGS about the contributions to be transferred between the DGS following the cross-border merger of a credit institution. Following a conciliation process which did not lead to the parties agreeing on a solution, the EBA adopted a decision specifying the contributions to be transferred between the DGS and requiring them to review their internal systems in order to explore potential enhancements to their risk management and communication processes in order to reduce the scope for similar future disagreements.

Joint ESAs criteria on the independence of CAs

Since 2020, the EBA has had the task of fostering and monitoring supervisory independence and has reported on the independence of prudential, conduct and AML/CFT supervisors, resolution authorities and deposit guarantee scheme designated authorities.

On 25 October 2023, the joint ESAs criteria on the independence of CAs (the Joint Criteria) were published on the three ESAs’ websites.

As different criteria have been adopted at the international level for each sector while the substance of the underlying principles is largely consistent, the aim of the Joint Criteria is to establish a single set of independence criteria for all CAs under the ESAs’ remit.

The Joint Criteria will be used by the ESAs for future common assessment work, as well as providing a useful European reference point that can be used as a tool by CAs, including in their interactions with legislators, to support and enhance their independence.

The Joint Criteria are non-binding, principle-based and outcome based, and organised around four areas of CAs’ governance: operational independence, financial independence, personal independence, and accountability and transparency.

Peer reviews

The EBA has made some changes to how it carries out peer reviews, undertaking more peer reviews – three peer reviews were launched in 2023 plus our first follow-up peer review following the 2020 ESAs review. In addition, the EBA peer review work plan for 2023 to 2024 was designed to support the EBA’s priorities and address current risks (e.g. a 2023 peer review looking at the treatment of mortgage borrowers in arrears, reflecting potential consumer detriment arising from the changing interest risk environment). In 2023, the following peer review reports were published:

- peer review report on authorisation under PSD2;

- peer review report on excluding transactions with non-financial counterparties established in a third country from credit valuation adjustment (CVA) risk;

- peer review report on supervision of creditors’ treatment of mortgage borrowers in arrears under the MCD.

The first follow-up peer review, on the joint ESAs guidelines on the prudential assessment of qualifying holdings, was started in spring 2023 and was published in early 2024. Work began in 2023 on the peer reviews on the definition of default and the application of proportionality under the SREP. Both are targeted peer reviews, and it is anticipated that the self-assessment questionnaires will be published in the summer of 2024. In addition, work is commencing on the tax integrity and dividend arbitrage trading schemes (Cum-Ex) peer review.

Engaging with stakeholders

The EBA continued to liaise closely with all relevant EU institutions and bodies, such as the Council of the EU, the European Parliament, the other ESAs and other EU institutions. In its mission, the EBA is accountable to the European Parliament, the Council and the Commission. In addition, we maintain an open institutional and proactive dialogue with our European partners. This dialogue remains a key pillar in the development of our products and in fostering awareness on current and future regulatory and supervisory challenges. In addition, the EBA maintains strong links with the supervisory community internationally. Through its active role at the Basel Committee on Banking Supervision (BCBS), the EBA contributes to discussions on global financial stability and international financial regulatory reforms, if and as appropriate.

The EBA’s participation in European and international forums ensures close and continuous collaboration with its counterparts around the world. It benefits from expertise and input from these stakeholders, while also sharing its knowledge with them.

To ensure proactive and effective engagement with all its stakeholders, the EBA made use of all its channels and tools, including seminars, workshops, public hearings, bilateral meetings and similar methods (most of them in hybrid format). In addition, the EBA engaged with industry, consumer associations, academics and students through speaking engagements and visits.

In addition, the EBA also continued answering stakeholders’ questions about the single rulebook submitted via the Q&A tool. In 2023, 287 were submitted and 190 were answered.

Figure 12: Stakeholder engagement in figures

Mapping deliverables by activity against the WP

This mapping of deliverables is based on the tables (Section 2) on the EBA 2023 WP with the main outputs for each activity, and compares planned against actual outcomes.

Policy and convergence

Activity 1: Capital, loss absorbency and accounting Contributing to VP 1 – directorate PRSP, unit LILLAC | Target | Actual | |

| Ongoing activities | Capital and loss absorbency

• Finalise and conclude the review on pre-CRR CET1 instruments • Monitor – and report – on CET 1 issuances • Monitor – and report – on AT1 issuances and calls • Maintain AT1 instrument templates

• Support Q&As on capital and eligible liabilities instruments • Monitor capital and TLAC/MREL eligible liabilities issuances, including for ESG purposes • Monitor and report on TLAC/MREL eligible liabilities issuances + Accounting and audit

| - | - |

| Output as per 2023 WP | Capital and loss absorbency

| TBC |

Q3 |

| Postponed / on hold | Accounting and audit

| TBC |

On hold

TBC

TBC |

| Additional output |

| - | Q4

Q4 |

* When updating the AT1 report, the EBA incorporated the TLAC-MREL monitoring report for simplicity in one publication. For CET1 issues no update was deemed necessary in 2023.

** Guidelines and report were postponed given the impact of the revised CRR (CRR III) and the aim now is to cover them as part of phase 2 of the EBA roadmap.

*** Update of the RTS was not deemed necessary at this stage.

Activity 2: Liquidity, leverage, and interest rate risk Contributing to VP 1 – directorate PRSP, unit LILLAC | Target | Actual | |

|---|---|---|---|

| Ongoing activities | Liquidity risk

Leverage ratio

Interest rate risk in the banking book

| - | - |

| Output as per 2023 WP | Liquidity risk

| Q1/Q2 | Q3 |

Liquidity risk

|

Q2/Q3 |

Q3 | |

| Cancelled | Liquidity risk

| Q2 | - |

| Additional output | Interest rate risk in the banking book

| - |

Q2

Q4 |

+ Tasks marked with a + were possible candidates to be postponed, cancelled or undertaken with less intensive resource input.

* It was not deemed necessary to proceed with a report on the cases of interdependent inflows and outflows in the LCR.

Activity 3: Credit risk (incl. large exposures, loan origination, NPLs, securitisation) Contributing to VP 1 – directorate PRSP, unit RBM | Target | Actual | |

|---|---|---|---|

| Ongoing activities |

Credit risk

Loan origination

Non-performing loans (NPLs)

Securitisation

| - | - |

| Output as per 2023 WP | Credit risk

|

Q1 |

Q1 |

| Delayed delivery | Credit risk

Securitisation

|

Q4 2022

Q3 2023

Q1

Q2 |

Q2

Q1 2023

Q1

Q1 2024 |

| Postponed/on hold | Securitisation

|

Q2 Q4 |

On hold On hold |

| Additional output | Credit risk

|

- |

Q4

Q4

Q3 Q3

Q4 |

+ Tasks marked with a + were possible candidates to be postponed, cancelled or undertaken with less intensive resource input.

* The ITS update was delivered in Q2 2023 (and in the WP should have referred to 2024 portfolios).

** Later delivery due to challenging legal deadline and resource constraints. The EBA requested delay to March 2023 (by letter to Commission of 2 February 2022) but then was able to close this in Q1.

*** Work not subject to legal deadline. Original planned delivery target had to be updated from Q2 to Q4.

**** Work not subject to legal deadline and had to be deprioritised.

*****There are limited market issuances, which does not allow for a sufficient sample of transactions to have a meaningful report.

Activity 4: Market, investment firms and services, and operational risk Contributing to VP 1 – directorate PRSP, unit RBM | Target | Actual | |

|---|---|---|---|

| Ongoing activities | • Regular updates to the list of diversified stock indices, including any additional relevant indices, and applying the ITS quantitative methodology • Monitor and promote consistent application of market risk requirements, including the finalisation of phase IV in the EBA roadmap on the implementation of the FRTB in the EU • Support the implementation of the Basel III market risk, CVA and counterparty credit risk (CCR) framework in the EU • Delivery of Basel III-related and CRR/CRD mandates as regards the FRTB, CVAs, CCR and securities financing transactions • Monitor and promote the consistent application of operational risk and investment firms’ requirements • Support Q&As on operational risk, investment firms, market risk, market infrastructure and CCR | - | - |

| Output as per 2023 WP | Market risk

| Q1 | Q1 |

Market risk

| Q2 |

Q2 | |

Market risk

| Q4 |

Q4 Q3

Q3

Q4 | |

| Delayed delivery | Market risk

|

Q4 2022 - |

Q2 Q3 |

| Postponed/on hold | Market risk

| Q4 | TBC |

| Additional output | Market risk

Investment firms

|

- |

Q4 Q4

Q4 Q4

Q2 Q3 |

* The ITS update was delivered in Q2 2023 (and in the WP should have referred to 2024 portfolios).

** Work not subject to legal deadline. Original planned delivery target had to be updated from Q2 to Q4.

*** Product was postponed due to no-action letter published by EBA on the FRTB boundary framework. The mandate has consequently been postponed as past of the CRR 3 legislative process.

Activity 5: Market, governance, supervisory review and convergence Contributing to VP 1 – directorate PRSP, unit Supervisory Review, Recovery and Resolution | Target | Actual | |

|---|---|---|---|

| Ongoing activities | Market access

Internal governance and remuneration

| - | - |

| Output as per 2023 WP | SREP and supervisory convergence • Report on convergence of supervisory practice in 2022 + | Q2 |

Q2 |

SREP and supervisory convergence

| Q4 | Q4 | |

| Delayed delivery | SREP and supervisory convergence

Internal governance and remuneration

|

Q2

Q2 |

Q4

Q4 |

| Postponed / on hold | Internal governance and remuneration

| Q2

Q3 Q4 | Q2 2024

Q1 2024 Q2 2024 |

| Additional output | Internal governance and remuneration

| - |

Q1

Q3

Q4

Q4 |

+ Tasks marked with a + were possible candidates to be postponed, cancelled or undertaken with less intensive resource input.

* Work not subject to legal deadline. Original planned delivery target had to be updated from Q2 to Q4.