Stress tests 2021

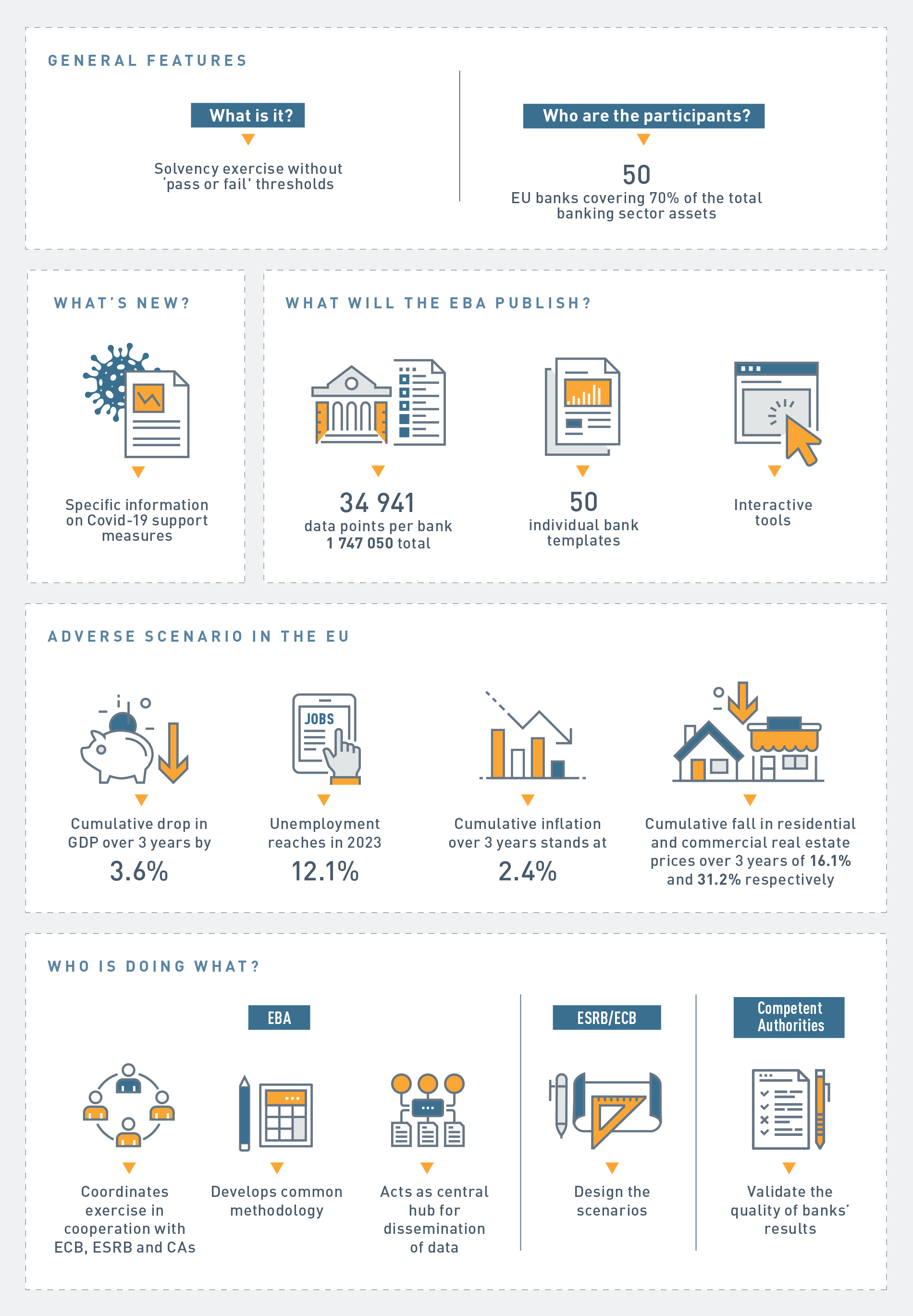

The European Banking Authority (EBA) published today the results of its 2021 EU-wide stress test, which involved 50 banks from 15 EU and EEA countries, covering 70% of the EU banking sector assets. This exercise allows to assess, in a consistent way, the resilience of EU banks over a three-year horizon under both a baseline and an adverse scenario, which is characterised by severe shocks taking into account the impact of the pandemic. The individual bank results promote market discipline and are an input into the supervisory decision-making process. The adverse scenario has an impact of 485 bps on banks’ CET1 fully loaded capital ratio (497 bps on a transitional basis), leading to a 10.2% CET1 capital ratio at the end of 2023 (10.3% on a transitional basis).

30/07/2021

The European Banking Authority (EBA) launched today the 2021 EU-wide stress test and released the macroeconomic scenarios. Following the postponement of the 2020 exercise, due to the COVID-19 pandemic, this year’s EU-wide stress test will provide valuable input for assessing the resilience of the European banking sector. Accordingly, the adverse scenario is based on a narrative of a prolonged COVID-19 scenario in a ‘lower for longer’ interest rate environment, in which negative confidence shocks would prolong the economic contraction. The EBA expects to publish the results of the exercise by 31 July 2021.

29/01/2021

The European Banking Authority (EBA) will launch its 2021 EU-wide stress test exercise with the publication of the macroeconomic scenarios on 29 January at 18:00 CET. The EBA expects to publish the results of the exercise by 31 July 2021.

25/01/2021

The European Banking Authority (EBA) published today the final methodology, draft templates and template guidance for the 2021 EU-wide stress test along with the key milestones of the exercise. The methodology and templates include some targeted changes compared to the postponed 2020 exercise, such as the recognition of FX effects for certain P&L items, and the treatment of moratoria and public guarantees in relation to the current Covid-19 crisis. The stress test exercise will be launched in January 2021 with the publication of the macroeconomic scenarios and the results published by 31 July 2021.

13/11/2020

The Board of Supervisors (BoS) of the European Banking Authority (EBA) agreed on the tentative timeline and sample of the 2021 EU-wide stress test. The exercise is expected to be launched at the end of January 2021 and its results to be published at the end of July 2021.

30/07/2020

In this section you can find the main documents of the 2021 EU-wide stress test. On 13 November 2020 the European Banking Authority published the final methodology, draft templates and template guidance for the 2021 EU-wide stress test. An updated version of the templates and template guidance, after the feedback provided by banks during the testing phase, is also available (18 December 2020 version). Please bear in mind that the current version of the templates and template guidance can still be subject to minor technical adjustments before its final publication in January 2021.

29/01/2021

29/01/2021

29/01/2021

The Macro-economic scenario has been amended on 12 February 2021. In particular, a correction of HICP and other consumption price indices on page 15 has been applied only for the United Kingdom

29/01/2021 (updated on 12/02/2021)

The Macro-economic scenario has been amended on 12 February 2021. In particular, a correction of HICP and other consumption price indices on page 15 has been applied only for the United Kingdom

29/01/2021 (updated on 12/02/2021)

29/01/2021

The excel version of the market risk shocks has been updated on 1 March 2020 to amend an inconsistency in the tab called “All_shocks_column”

29/01/2021 (updated on 01/03/2021)

29/01/2021

Templates (.xls)| Templates guidance (.pdf)

18/12/2020

Templates (.xls) | Templates guidance (.pdf)

13/11/2020

13/11/2020

2021 EU-wide stress test results

The European Banking Authority (EBA) published the results of the 2021 EU-wide stress test of 50 banks.

The aim of the EU-wide stress test is to assess the resilience of EU banks to a common set of adverse economic developments in order to identify potential risks, inform supervisory decisions and increase market discipline.

The EU-wide stress test is coordinated by the EBA and carried out in cooperation with the European Central Bank (ECB), the European Systemic Risk Board (ESRB), the European Commission (EC) and the Competent Authorities (CAs) from all relevant national jurisdictions.

Summary results

| Description | What you can get |

|---|---|

Data aggregated by countries of banks and Individual banks' data | Dashboard with main indicators and Stress test results by country and by bank. The Dashboard provides summary figures showing the impact of the stress test on capital ratios, as well as the main drivers of the impact. You can use it to compare, for example, the impact of the adverse scenario on Common Equity Tier 1 (CET1) ratio for different countries and banks by year. Also it allows to visualise the contribution of main drivers to the change in CET1 capital ratio from 2020 to 2023. |

P&L, Capital and Risk Exposure Amount

| Description | What you can get |

|---|---|

P&L, Capital and Risk Exposure Amount Data aggregated by countries of banks and Individual banks' data | This tool shows countries' data, reported in the following templates: Risk Exposure Amount, Capital, P&L and Major capital measures and realized losses. Figures are aggregated by country of the bank. The tools allows also to visualise individual banks' data reported under the same templates. |

Credit risk and securities

| Description | What you can get |

|---|---|

Data aggregated by countries of banks and Individual banks' data | This tool provides credit risk exposures for a specific country of counterparty (US, DE, ...) broken down by the country of the banks exposed to it (AT, DE,..) for all regulatory portfolios (IRB/SA) and exposure classes (corporates, retail, ...). |

COVID-19

| Description | What you can get |

|---|---|

Data aggregated by countries of banks and Individual banks' data | This tool shows exposures subject to legislative and non-legislative moratoria and public guarantees for a specific country of counterparty (US, DE, ...) broken down by the country of the banks exposed to it (AT, DE,..) for all regulatory portfolios (IRB/SA) and exposure classes (corporates, retail, ...). |

Banks individual results

All you need to know about the 2021 EU-wide stress test

In this section you will find an infographic that will help you understand the 2021 EU-wide stress test

(1) Some banks have filled row 74 in template “TRA_CAP” (Total Additional Tier 1 and Tier 2 instruments eligible as regulatory capital under the CRR provisions that convert into Common Equity Tier 1 or are written down upon a trigger event) with zeros although they had issued such type of investments. This information represents a memo item and it has no impact on the computation of capital ratios or the expected capital depletion at the end of the Stress Test horizon.