Executive Summary of the 2021 Annual Report

Introduction by EBA Chairperson and Executive Director

2021 marked our 10-year anniversary and we celebrated this special and momentous milestone by reflecting on all the key achievements of the past decade, the progress made so far as well as by setting the tone for the challenges that lie in front of us.

Since 2011, we have developed a harmonised and consistent set of rules on prudential and resolution aspects with more than 230 technical standards, which have helped establish a level playing field for financial institutions across the European Union (EU). We have also provided additional guidance with more than 120 Guidelines and answers to over 2000 Q&As on its supervisory implementation.

José Manuel Campa, Chairperson of the EBA

Figure 1: Overview of main outputs delivered against the EBA work programme for 2021

The evolving multi-annual priorities and mandates called for a reorganisation of the EBA working model aimed at increasing focus in key areas, fostering internal synergies and creating new opportunities for staff. We strengthened the Economic and Risk Analysis Department with a new Unit dedicated to Environmental, Social and Governance (ESG) risks and set up a new Department focusing on the entire data value chain, from their definition to their acquisition, management and dissemination. Finally, we created fully-fledged units focusing on Digital Finance and on anti-money laundering and countering the financing of terrorism (AML-CFT).

François-Louis Michaud, Executive Director of the EBA

Achievements in 2021

Sed ultrices sed elit in feugiat. Aliquam eget felis quis risus mattis tristique. Vestibulum blandit, eros ac pulvinar tincidunt, mauris quam ultricies nunc, faucibus maximus tortor odio at erat. Nam dapibus nisi lacus, a tristique nisl porttitor sed. Aliquam erat volutpat. Nullam dapibus justo et tellus luctus tincidunt tristique at turpis. Donec placerat malesuada faucibus. Praesent lorem tortor, scelerisque molestie mauris at, malesuada rhoncus mi. Integer fringilla aliquam dignissim. Nam malesuada, ex ut iaculis porttitor, erat lacus congue est, nec fringilla urna lacus ac augue.

Continuing the regulatory developments

Making progress in the development of the new prudential framework for investment firms

Under the new prudential regime, investment firms will be subject to risk-sensitive and proportionate prudential requirements based on their size and range of performed activities or financial services provided. In order to facilitate the preparation of market participants and the transition to the new prudential framework, the EBA provided an overview of the expected timeline, process and deliverables related to the Investment Firms Directive (IFD) and Investment Firms Regulation (IFR) in the EBA investment firms roadmap. The roadmap envisages four phases, with 21 technical standards and six Guidelines to be finalised by the end of 2022.

Supplementing the regulatory framework in the area of market risk and markets infrastructure

In 2021, the EBA continued to deliver technical standards in the area of market risk in accordance with its roadmap for the new market and counterparty credit risk approaches. The EBA also published its final Guidelines clarifying the requirements for the data inputs used to compute the expected shortfall risk measure under the alternative Internal Model Approach (IMA). In particular, these requirements aim to ensure that data inputs are calibrated to historical data reflective of prices observed or quoted in the market. Those regulatory deliverables contribute to ensuring the smooth introduction in the EU of the revised framework to calculate capital requirements for market risk.

Continuing the development of an all-inclusive large exposures regime in the European Union

In line with its new mandates in the risk reduction measures package adopted by European legislators in 2019, the EBA developed Guidelines to harmonise the way in which competent authorities assess and manage breaches of the large exposures limits by institutions.

Monitoring the implementation of Basel III global standards

The EBA conducts a regular Basel III monitoring exercise analysing (i) the impact of the final Basel III rules on European credit institutions’ capital and leverage ratios and (ii) the associated shortfalls that would result from a lack of convergence with the fully implemented Basel III framework.

In September 2021, the EBA published a Report on monitoring the impact of implementing the final Basel III regulatory framework in the EU using data as of December 2020. The Report contains a breakdown of the impact on the total minimum required capital arising from credit risk, operational risk, leverage ratio reforms and the output floor. The main factors driving the impact of Basel III framework are the implementation of the output floor and the credit risk reform, with 7.1% and 5.1% respectively. The new leverage ratio is partially counterbalancing the impact of the Basel III risk-based reforms by 4.3%.

The EBA has also been active in providing the Basel Committee on Banking Supervision (BCBS) with input before the development of supervisory standards by conducting new data collection activities that allow the proposed policies to be better assessed. In addition, the EBA collaborates closely with the BCBS to develop methodologies that more accurately evaluate the impact of the proposed BCBS supervisory standards.

Figure 2: Basel III monitoring exercise – total minimum capital requirement impact by risk category (December 2020 reference date)

New as of December 2021: the EBA decided to make the Basel III exercise mandatory. This will help the EBA to represent effectively the interests of EU institutions in the BCBS and to provide informed opinions and technical advice to the European Commission.

Implementing effective resolution tools

In 2021, the EBA finalised its resolvability Guidelines, which represent a significant step in complementing the EU legal framework in the field of resolution based on international standards and leveraging on EU best practices. Taking stock of the best practices developed so far by EU resolution authorities on resolvability topics, the Guidelines set out requirements to improve resolvability in the areas of operational continuity in resolution, access to financial market infrastructure, funding and liquidity in resolution, bail-in execution, business reorganisation and communication.

Identifying, assessing and monitoring risks in the EU banking sector

The 2021 Risk Assessment Report found that banks had strengthened their capitalisation and liquidity positions. They were helped by the robust economic recovery and the progress achieved in tackling the COVID-19 pandemic.

The 2021 Risk Assessment Report found that banks had strengthened their capitalisation and liquidity positions. They were helped by the robust economic recovery and the progress achieved in tackling the COVID-19 pandemic.

The assessment also acknowledges that banks have made some progress on ESG risk considerations. The share of ESG bonds of total bank issuances has increased in recent years, reaching around 20% of banks’ total placements this year.

In 2021, the quarterly EBA risk dashboard remained a leading element contributing to the regular risk assessment and in parallel fulfilling the EBA’s role of disseminating data to stakeholders. The EBA risk dashboard has become a reference point for granular EU aggregate and country-by-country supervisory data. It provides comprehensive, easy-to-use fundamental risk indicators for assessing the well-being of the EU banking sector, as well as comprehensive statistical tables for analysing trends and running peer analyses.

Figure 3: Looking at the EU banking sector, which other sources of risks or vulnerabilities are likely to increase further in the next 6 to 12 months?

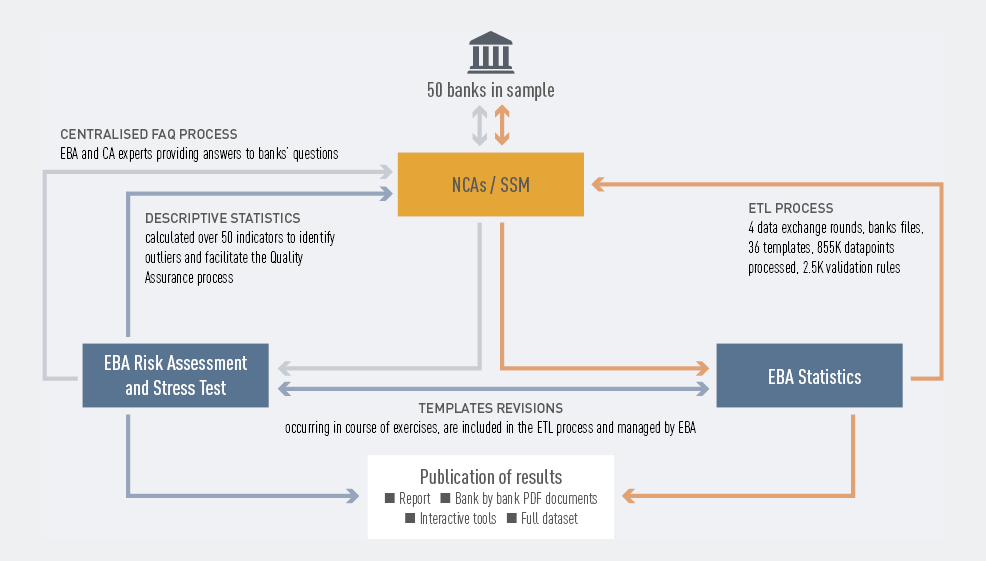

The 2021 EU-wide stress test

In July 2021, the EBA published the results of the 2021 EU-wide stress test, which involved 50 banks covering broadly 70% of total EU banking sector assets. Given the unprecedented macroeconomic shock due to the pandemic in 2020, the baseline scenario provided a useful yardstick for assessing and comparing the situation of EU banks. The stress test also helped provide a perspective on how the banking system could develop after the pandemic.

Overall, the results showed that banks continued to build up their capital base, with a Common Equity Tier 1 (CET1) ratio at the beginning of the exercise of 15%, the highest since the EBA has been performing stress tests, despite the unprecedented decline in gross domestic product (GDP) and the initial effects of the COVID-19 pandemic in that year.

Figure 4: The process behind the EU-wide stress test

Increasing transparency in the EU banking sector

The transparency exercise is a well-established and consolidated data dissemination, which provides the public with an invaluable source of individual banks’ data.

The EBA conducted its annual EU-wide transparency exercise in December 2021, disclosing detailed bank-by-bank data for 120 banks across 25 countries of the EU and the European Economic Area (EEA).

The results showed that fiscal and regulatory support measures put in place during the pandemic have prevented asset quality deterioration but have also made it more difficult for banks to assess borrower creditworthiness. The uncertainty on the economic outlook could trigger repricing of risks.

Figure 5: The EU-wide transparency exercise over the years: the evolution of a well established data collection

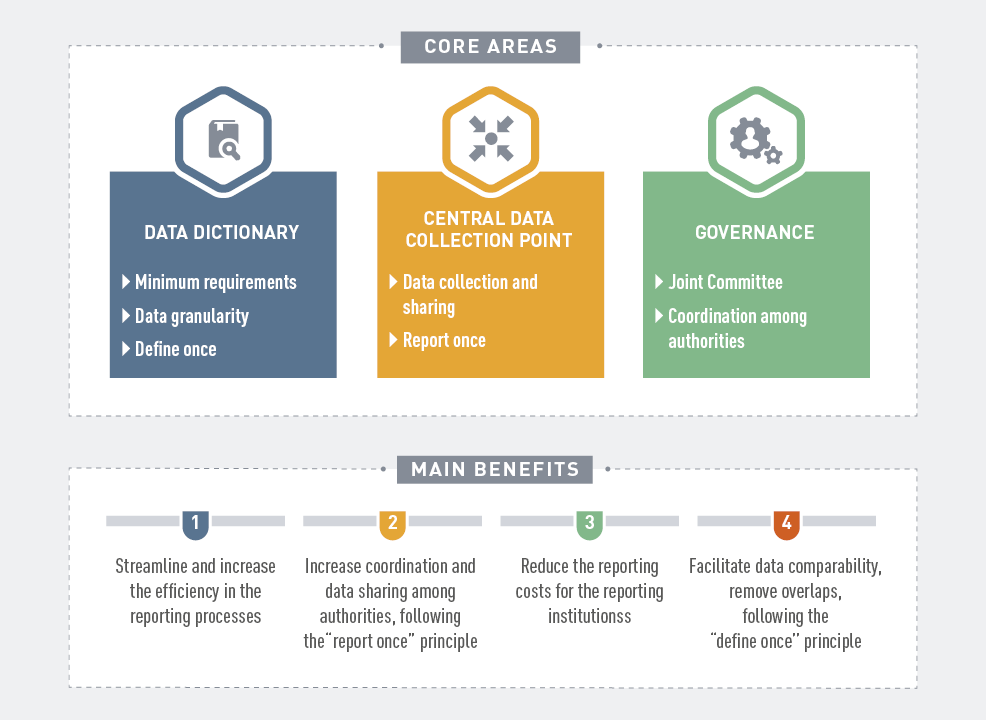

Becoming an integrated EU data hub

In 2021, the EBA completed its work on the feasibility study on a consistent and integrated system for collecting statistical, resolution and prudential data. The resulting Report puts forward a long-term vision for what an integrated reporting system could look like. It also highlights how reporting processes could be streamlined and improved for both institutions and competent authorities, and how cooperation among authorities could be enhanced in the areas of prudential, resolution and statistical reporting.

Figure 6: Integrated reporting system overivew

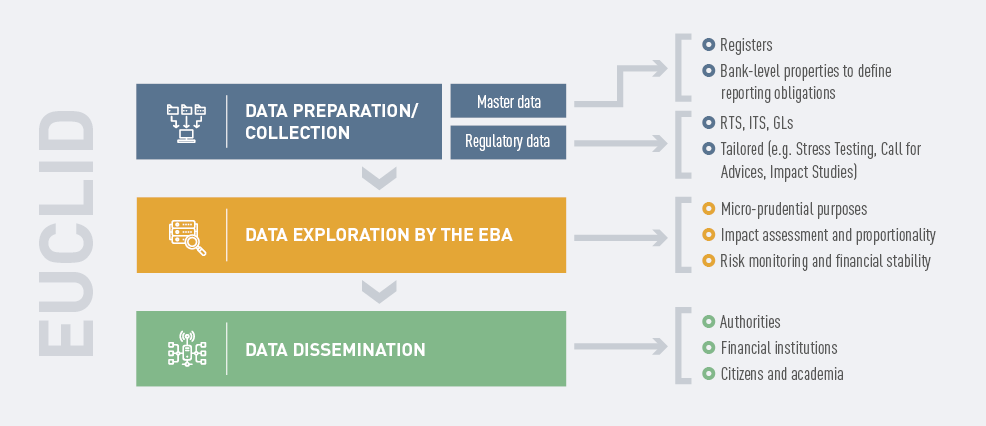

Finalising the EUCLID project

Figure 7: EUCLID process explained

With the implementation of the European Centralised Infrastructure of Data (EUCLID) the EBA was able to integrate most of its historical data and to start collecting information on the entire EU banking sector. Thanks to EUCLID, the various authorities liaising with the EBA have gained additional freedom and flexibility to manage data transmissions to the EBA. Master data flows steadily to the EBA, resulting in seamlessly refreshed reporting obligations being prepared overnight. The EBA can thus address reporting issues more quickly via EUCLID’s automatic feedback on data transmissions.

Figure 8: Number of reporting modules collected via EUCLID (reference date September 2021)

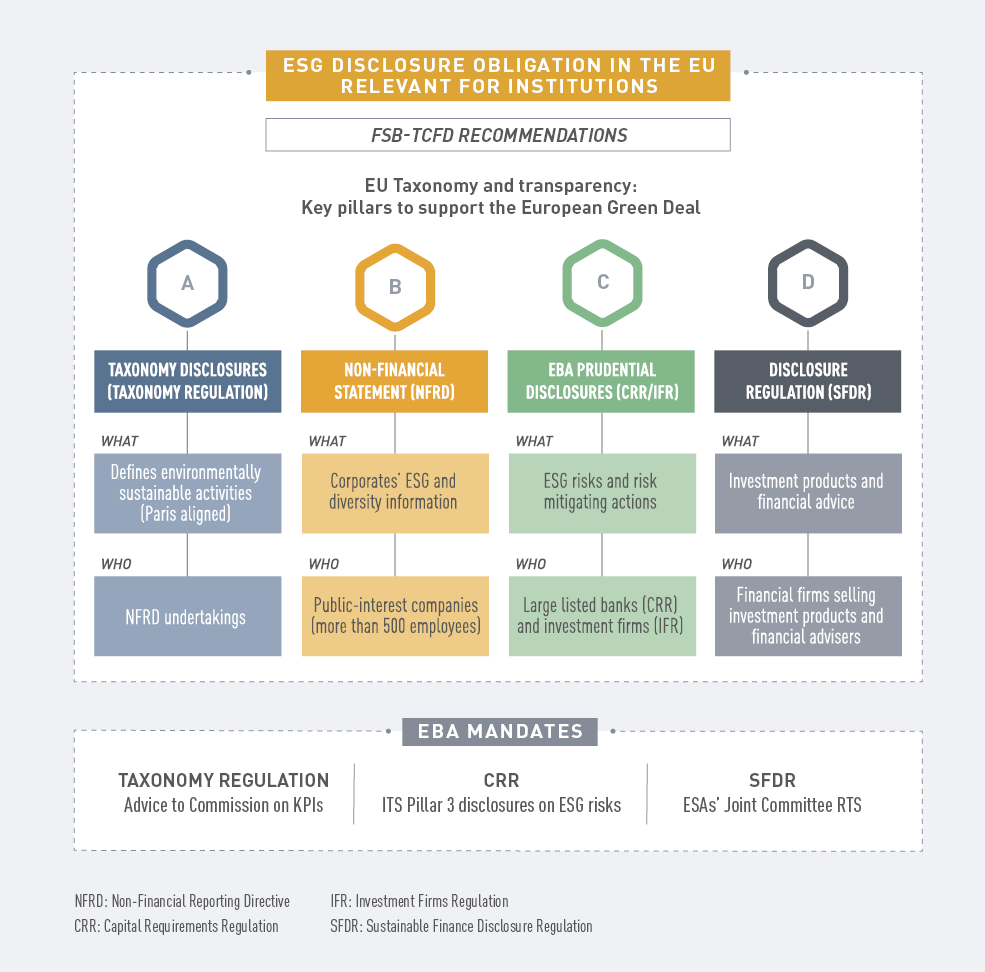

Continuing the development of a comprehensive and enhanced disclosure framework

In 2021, the EBA continued to make progress in implementing its roadmap and strategy on Pillar 3 disclosures focusing on:

- disclosing indicators of global systemic importance by global systemically important institutions (G-SIIs);

- disclosing exposure to interest rate risk on positions not held in the trading book (IRRBB);

- disclosing ESG risks;

- disclosing investment funds by investment firms.

Figure 9: ESG disclosure in the EU

Assessing fraud levels in retail payments

The EBA carried out an analysis of the payment fraud data reported by the industry to assess how effective are the payment security requirements developed by the EBA in the past years. One of the key observations is that fraud is substantially higher in cross-border transactions with counterparts located outside the (EEA), where no strong customer authentication (SCA) requirements apply, than in those conducted inside the EEA (where SCA does apply).

Figure 10: Share of fraudulent transactions (in terms of the volume of total transactions) when payments are executed domestically, inside and outside the EEA

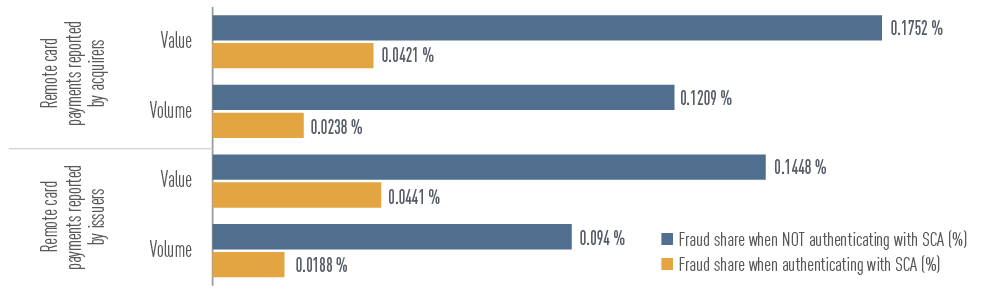

Other observations suggested that overall the regulatory requirements developed in relation to payment security are having the desired effect. For example, the share of fraudulent payments in the total payment volume and value is significantly lower for transactions that are authenticated with SCA than those that are not.

Figure 11: Share of fraudulent transactions (in terms of the volume and value of total transactions) for remote card payments reported by issuers and acquirers, with and without SCA

Contributing to the sound development of financial innovation in the financial sector

In 2021, the EBA continued to monitor how financial innovations emerge and evolve in the financial market. Crypto-assets, decentralised finance and the application of artificial intelligence (AI), as well as digital platforms and solutions to facilitate AML/CFT compliance, are just a few examples of innovations that are currently on the EBA’s innovation monitoring radar.

The EBA contributed to a wide range of topics under the European Commission’s digital finance strategy and beyond, including:

- legislative proposals for the Regulation on Markets in Crypto-assets (MiCA);

- legislative proposals for the Digital Operational Resilience Act (DORA);

- use of digital platforms in the EU’s banking and payments sector;

- requirements for crowdfunding service providers;

- proposals for non-bank lending.

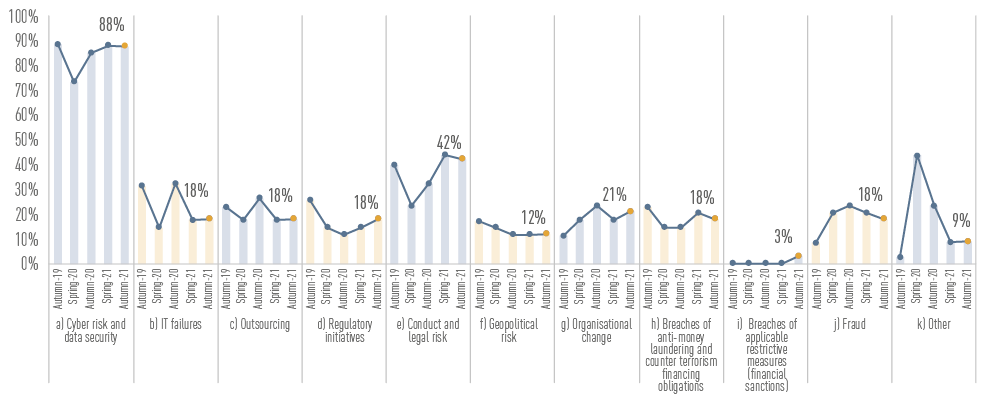

Figure 12: Main drivers of operational risk as seen by banks

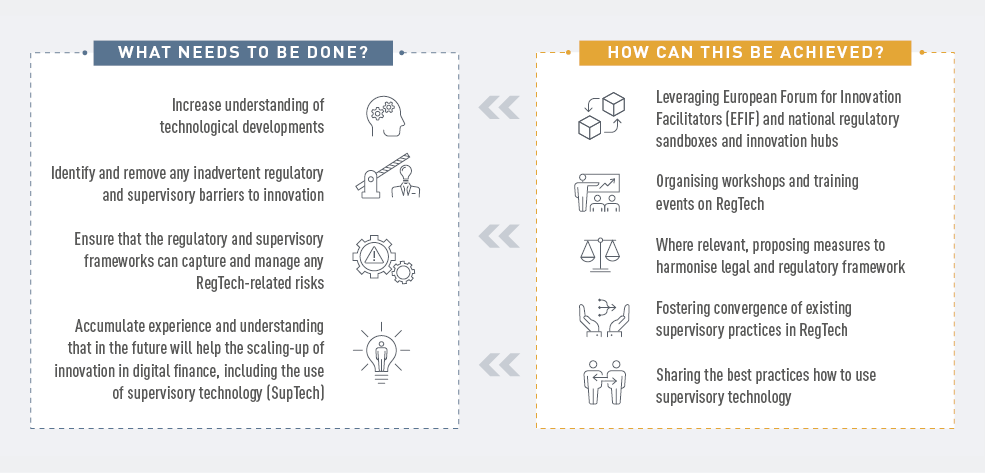

Analysing the RegTech market in the EU

In 2021, the EBA assessed the benefits, challenges and risks of Regulatory technology (RegTech) use in the EU and analysed the application of technology to facilitate compliance with regulatory requirements and make certain financial institutions’ processes more effective and efficient.

The top five segments identified in which RegTech is used most widely are AML/CFT, fraud prevention, prudential reporting, ICT security and creditworthiness assessments.

Figure 13: Benefits, challanges and risks of RegTech

Figure 14: Continued monitoring of RegTech development

Identifying the benefits and challenges of machine learning models used in the context of IRB models for credit risk

In 2021 the EBA consulted with the industry on how new, sophisticated machine learning models can coexist with and adhere to the regulatory requirements when used in the context of internal ratings-based (IRB) models. The discussion paper investigated a set of principles-based recommendations that would ensure the prudent use of machine learning models in the context of the IRB framework.

Strengthening depositor protection

In the context of depositor protection, the EBA has carried out work in three areas:

Enhancing the resilience of the national deposit guarantee schemes: the revised Guidelines on the stress tests conducted by the national Deposit Guarantee Scheme (DGS) extend the scope of the DGS stress tests by requiring more tests compared to the original guidelines. Deposit insurers now have to test their ability to perform all the interventions included in their legal mandate.

Figure 15: Steps of the stress testing cycles conducted by the DGS

Strengthening the protection of client funds by deposit insurers: the Opinion on the treatment of client funds under the Deposit Guarantee Schemes Directive (DGSD) assessed the current approaches to the protection of funds deposited with credit institutions on behalf of clients by entities that are themselves excluded from DGS protection

Contributing to the harmonised and transparent funding of deposit insurers: the Guidelines on the delineation and reporting of available financial means (AFMs) of deposit guarantee schemes that aim to improve confidence in financial stability across the EU by establishing a more harmonised application of the DGSD with regard to reaching the target level in the and by enhancing transparency and the comparability of DGS’ financial positions.

Building the infrastructure in the EU to lead, coordinate and monitor AML/CFT supervision

The main areas of focus remained AML/CFT-related policy development, fostering cooperation across Member States’ competent authorities in the fight against money laundering and terrorist financing and supporting the effective implementation of the overall EU AML/CFT framework through training and capacity-building.

Putting in place a data-driven approach to monitoring ML/TF risks

The EBA carried out preparatory work that led to the launch in January 2022 of EuReCA, the European reporting system for material CFT/AML weaknesses. The EBA aims to use EuReCA to gather, structure and share information on financial institutions’ AML/CFT material weaknesses, as identified by competent authorities, and the measures that such authorities have taken to rectify these material weaknesses.

In addition, the EBA continued monitoring new money laundering (ML) and terrorist financing (TF) risks and alerted competent authorities and the public at large where necessary. The EBA issued an Opinion on the risks of ML and TF affecting the EU’s financial sector. It identified risks related to virtual currencies and innovative financial services, de-risking, tax-related risks and risks associated with the COVID-19 pandemic. The Opinion included targeted recommendations to competent authorities to close the gaps identified.

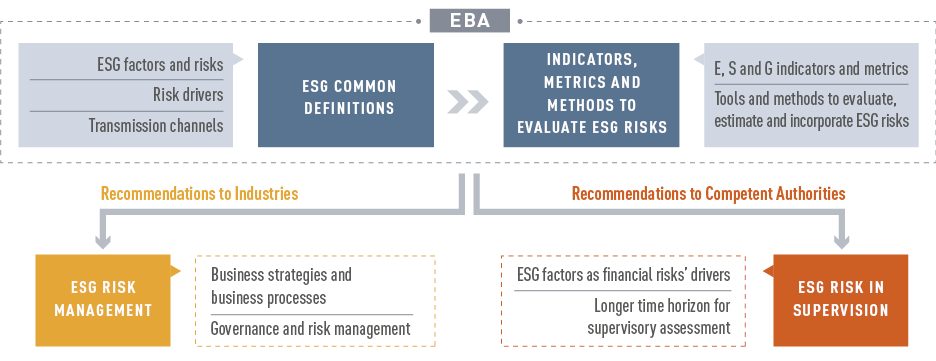

Integrating and managing ESG risks

There is a broad acknowledgement that ESG factors may translate into financial risks and that the financial sector should play a key role both in terms of managing risks and facilitating the transition towards a more sustainable economy. Clear definitions and effective risk assessment methodologies are necessary to achieve progress in this regard.

There is a broad acknowledgement that ESG factors may translate into financial risks and that the financial sector should play a key role both in terms of managing risks and facilitating the transition towards a more sustainable economy. Clear definitions and effective risk assessment methodologies are necessary to achieve progress in this regard.

In 2021, the EBA published a Report on the management and supervision of ESG risks for credit institutions and investment firms which harmonises definitions and describes available methodologies, as well as sets out the EBA’s proposals and recommendations on how institutions should address ESG risks and how supervisors should assess institutions’ ESG risk management practices.

Figure 16: Main content of EBA report on ESG risk management and supervision

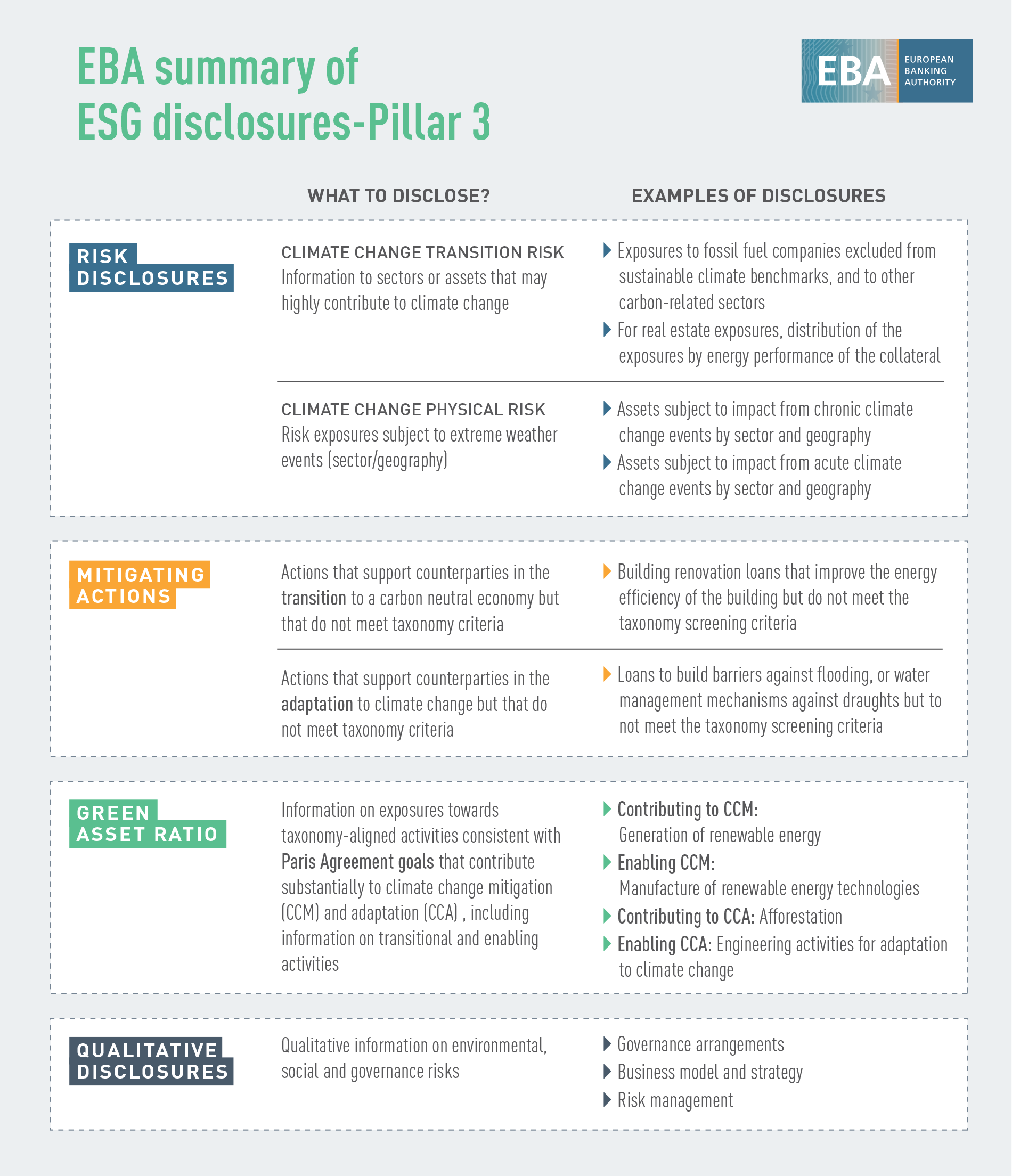

Defining disclosure standards on sustainability

The EBA aims to support institutions in their disclosure obligations, facilitating stakeholders’ access to comparable information on lending and investment activities that are subject to ESG-related risks, while enabling them to compare institutions’ sustainability performance. To this end, the EBA contributed towards defining sustainability disclosure standards with its technical standards for Pillar 3 disclosures of ESG risks.

Figure 17: Summary of ESG disclosures Pillar 3

Laying the foundations for embedding climate risk into the stress testing framework

The EBA addressed the climate-related risks in its climate stress test and scenario analysis. The EBA pilot exercise conducted in May 2021, was the first EU-wide initiative on climate risk and was run with 29 volunteer banks from 10 EU countries representing around 50% of the banking sector assets in the EU (47% of its risk-weighted assets). It focused on transition risk, and its main objective was to explore data and methodological challenges to categorise exposures that could potentially be vulnerable to climate risks and to assess banks’ readiness to apply the EU green taxonomy. The experience gained by both the EBA and participating banks was positive. It helped give an understanding of where banks stand in terms of data capabilities to assess climate risk. Banks are making significant efforts to expand their data and modelling infrastructures, but a substantial amount of work still remains to be done, especially concerning client-specific information at the activity level and incorporating forward-looking components (such as transition strategies) into climate risk assessment tools.

Providing guidance on own funds and eligible liabilities that include ESG features

In light of the recent market trend of issuing own funds or eligible liabilities instruments with ESG features linked to ESG labels, the EBA included a dedicated guidance in the Additional Tier 1 (AT1) Report published in June 2021. The purpose of this guidance was to (i) provide an overview of the risks identified, (ii) comment on the differences identified in clauses and (iii) provide policy observations and guidance on how the clauses used for ESG issuance and the eligibility criteria for own funds and eligible liabilities instruments interact. The ultimate aim was to indicate best practices or practices/clauses that should be avoided from an own funds and eligible liabilities perspective.

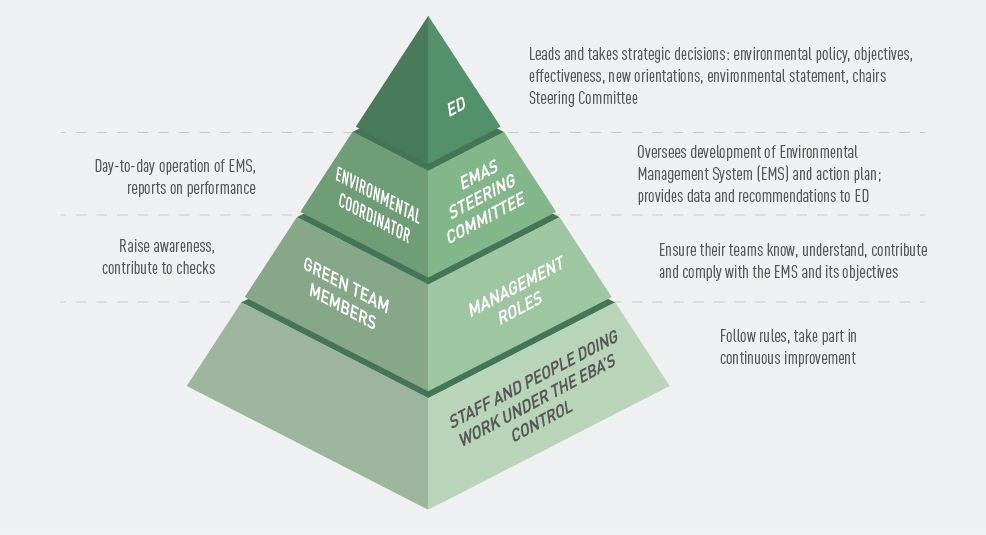

Making progress towards obtaining Eco-Management and Audit Scheme (EMAS) registration

In 2021, the EBA successfully completed all the preparatory phases to be registered with the EU Eco-Management and Audit Scheme (EMAS) and obtained the registration in August 2022. In its environmental policy, the EBA set out its intentions and direction in relation to its environmental perforce and committed to its continuous improvement.

Figure 18: EMAS team pyramid

Addressing the aftermath of COVID-19

In 2021 the EBA continued to mitigate the short-term effects of the pandemic, in order to maintain banks’ ability to provide lending and address short-term liquidity shortages faced by many businesses, through the reactivation of the Guidelines on legislative and non-legislative moratoria. However, after more than a year of crisis conditions, the focus was shifted to managing the transition to its full extent in order to ensure a smooth return to normality.

In April 2021, the EBA also followed up on a survey it had conducted in April 2020 on the potential impact of the pandemic on depositor protection provided by national DGSs. The updated survey confirmed that the pandemic itself did not have any adverse effects on depositor protection and confirmed the continued resilience of DGSs.

The EBA also monitored the evolution and assessed the asset quality of moratoria on loan repayments and public guaranteed schemes which authorities put in place to support businesses and households during the pandemic. The volume of loans with active EBA-eligible moratoria was residual at the end of 2021, (around EUR 10 bn), while banks still report around EUR 700 bn of loans with expired EBA-eligible moratoria.

Celebrating 10 years of EBA achievements

The year 2021 marked an important milestone for the EBA, which celebrated its 10 years of activity. For this special anniversary, the EBA organised several internal and external initiatives.

Image 1: 15 interviews in 13 EU countries: Belgium, Cyprus, the Czech Republic, Denmark, France, Finland, Germany, Greece, Italy, the Netherlands, Portugal, Slovenia, Spain. Reaching out locally helped to build synergies with domestic media, which in turn lead to increased visibility of the EBA and its work.

The EBA also organised its high-level conference EBA@10, which took place in a hybrid format on 26 October. The event brought together stakeholders from all over the European Union and beyond to reflect together on the progress made over the last 10 years on EU banking and financial integration, as well as to look at the EBA challenges and opportunities that lie ahead. Recordings of the conference are available on the EBA YouTube channel.

Five strategic areas for 2022:

Monitor and update the prudential framework for supervision and resolution

Revisit and strengthen the EU-wide stress-testing framework

Banking and financial data: leverage the EUCLID

Digital Resilience, Fintech and Innovation: deepen analysis and information-sharing

Fight AML/CFT and contribute to a new EU infrastructure

Two horizontal priorities for policy work:

ESG: provide tools to measure and manage risks

COVID-19: monitor and mitigate the impact