-

Article 243 (2)(b) sets the maximum risk weight that the underlying exposures of an STS securitisation should have to qualify for the treatment set out in Articles 260, 262 and 264.

These maximum risk weights are set according to the exposure class. Article 243(2)(b)(i) refers to exposures in the form of loans secured by residential mortgages or fully guaranteed residential loans, as referred to in point (e) of Article 129(1), for which the basis of the calculation of the maximum risk weight is the exposure value-weighted average risk weight.

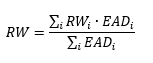

Consistently also with Article 267(1), which defines the calculation for the maximum risk weight for senior securitisation positions, the exposure value-weighted average basis referred to in Article 243(2)(b)(i) is to be intended as the exposure-weighted-average risk weight, and shall therefore be calculated with the following formula:

Where

is the risk weight of the individual exposure

is the risk weight of the individual exposure  , and

, and  is the value associated with the individual exposure

is the value associated with the individual exposure  .

.

Disclaimer

The Q&A refers to the provisions in force on the day of their publication. The EBA does not systematically review published Q&As following the amendment of legislative acts. Users of the Q&A tool should therefore check the date of publication of the Q&A and whether the provisions referred to in the answer remain the same.