Disclaimer

This report is provided for transparency purposes only. The official results are those which have been submitted and confirmed by competent authorities and published as PDF files by the European Banking Authority (EBA). The cut-off date for the data in this report is 17 July 2025 – 16:00 CET.

Executive summary

The results of the 2025 EU-wide stress test indicate that the largest EU banks would be resilient to a severe hypothetical stress scenario. The adverse scenario assumes a sharp deterioration in the global macro-financial environment, driven by heightened geopolitical tensions, entrenched trade fragmentation, higher inflation and persistent supply shocks causing simultaneous and prolonged recessions in the EU and global economies with high unemployment, and sharp falls in asset prices.

The results indicate that the EU banking system would have the capacity to continue to support the EU economy in stressed times. Despite bearing combined losses in the adverse scenario of EUR 547 bn during the 3-year horizon[1], higher than in previous stress tests, the results indicate that the EU banking system could withstand a severe but plausible macroeconomic scenario, reflecting the resilience built up by banks in recent years.

For the EU, the adverse scenario is more severe than the global financial crisis (GFC) and also substantially more severe than the recent macroeconomic developments. It combines a sharp loss of real GDP for the EU, reaching -6.3% from the starting point in 2024 to the end of the stress horizon in 2027, while the EU unemployment rate increases by 5.8 percentage points in the same period.

The stress test scenario is not a forecast of economic or financial conditions in the EU or elsewhere. Instead, it represents a severe but plausible adverse scenario designed to test the resilience of EU banks to a wide range of adverse shocks. It outlines hypothetical paths for key economic and financial variables following the materialisation of risks to which the EU banking system is exposed. While not a prediction of the most likely outcome, it provides a consistent and extreme downside case. Given the current uncertainty in the macroeconomic outlook, the scenario remains both relevant and sufficiently severe for assessing the robustness of EU banks.

EU banks show strong income generation during the exercise which helps to partly absorb the losses from the portfolio deterioration and results in an aggregate capital depletion of 370 bps[2]. The capital depletion is lower than in the 2023 EU-wide stress test, despite the overall severity of the scenario being broadly similar.

EU banks finish the exercise with an aggregate Common Equity Tier 1 (CET1) ratio above 12%. This outcome shows the capacity to continue to provide lending to households and businesses through a period of crisis caused by geopolitical tensions, even if economic and financial conditions were to be worse than expected. All participating banks remain above their CET1 total SREP capital requirement under the adverse scenario, while there is a breach of Tier 1 total SREP leverage ratio requirement for one bank.

Banks start the exercise with higher profitability and capital than in recent years, while showing favourable and stable asset quality. High net interest income (NII) provides a significant cushion for absorbing losses in the adverse scenario. This is further supported by the moderate interest rates rise in response to higher inflation. Also, other income sources like net fees and commission income remain elevated in the adverse scenario, also reflecting higher starting points.

Credit risk is the main contributor to the stress test losses, followed by market risk losses. While banks show higher nominal losses, they have better absorption capacity through income generation. The absolute credit risk losses at EUR 394 bn over the three-year scenario horizon are driven by the severe impact on the real economy of the scenario, and they are higher compared to the previous exercise as a result of the increase of stage 2 loans and the reduction of the coverage ratio for stage 3 exposures since then. Initial total market risk losses of EUR 187 bn that are caused by the assumed market downturn in the first year of the adverse scenario were largely offset by banks’ income generated through clients that engage in market activity. As a result, total market risk losses over the three-year scenario horizon were nearly halved to EUR 98 bn.

The adverse scenario affects economic sectors differently through rising energy and commodity prices and heightened trade tensions. Energy-intensive sectors and those dependent on international trade, like manufacturing and agriculture, are more impacted compared to other sectors. As in previous stress tests, the real estate and construction sectors are affected by the general economic downturn.

Compared to the last EU-wide stress test, banks differentiate better the impact of adverse scenarios across sectors but still need to further improve their modelling efforts. As the use of models improves risk sensitivity, banks should further develop their statistical capabilities to project sectoral losses. These capabilities would enhance their risk management of vulnerabilities that may hide in parts of their corporate portfolios. Regarding conduct risk, banks face difficulties projecting losses beyond one year, where after – based on a comparison between their baseline projections in the 2023 exercise and realised losses in the 2023-24 period – they tend to underestimate losses in the second year.

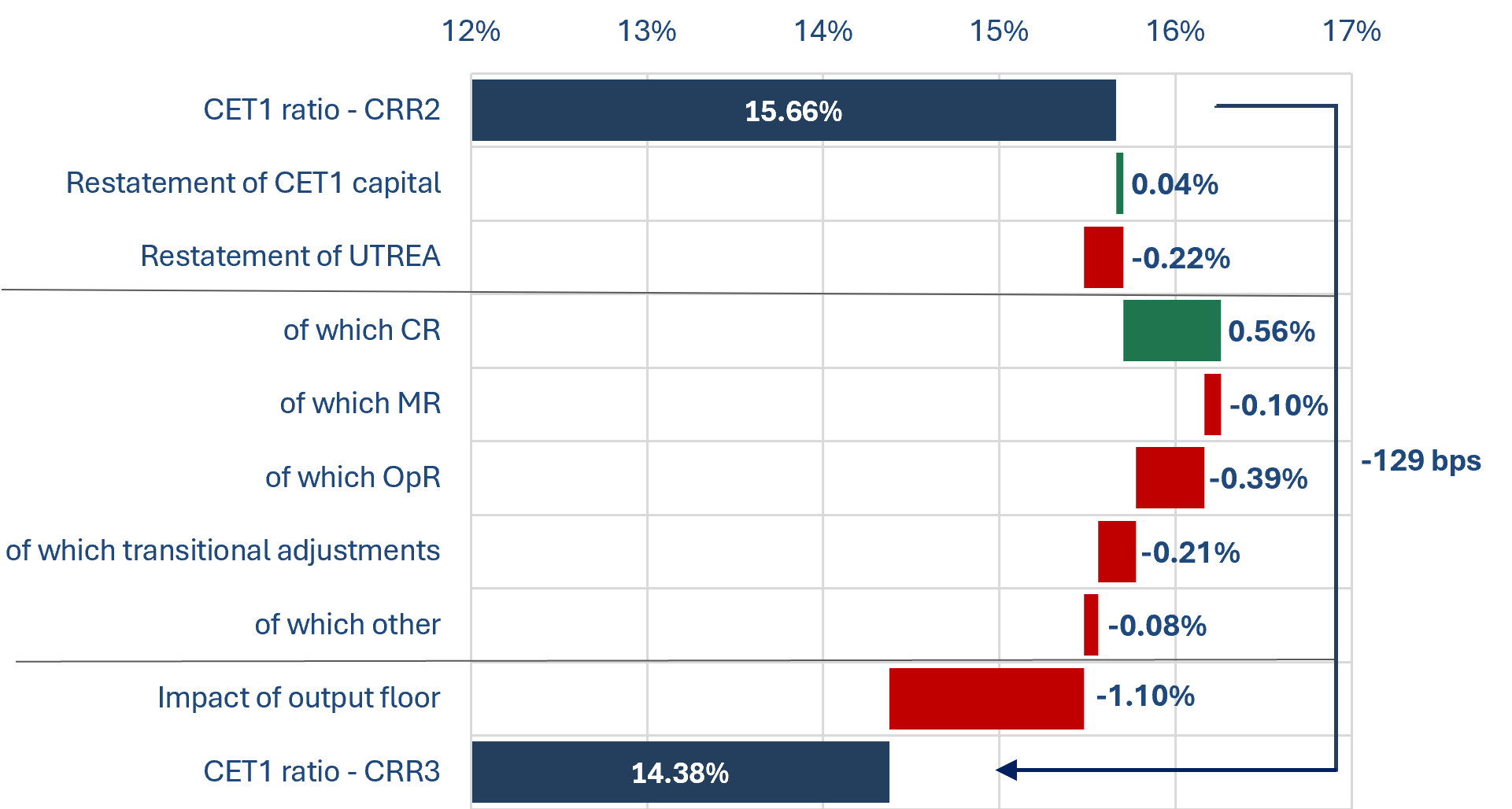

The implementation of the new Capital Requirements Regulation (CRR3) impacts banks’ regulatory capital ratios differently over time, due to transitional arrangements that progressively phase-in the new rules. Full CRR3 implementation will occur in 2033, and banks still have room to adjust their balance sheets until then. The impact of the CRR3 rules on the EU banks’ aggregate CET1 ratio at year-end 2024 is negligible on a transitional basis. If it is calculated on a fully loaded basis, with the capital requirements phased-in by 2033, the aggregate capital ratio reduces by 129 bps on a fully loaded basis, coming mainly from the output floor. Still, in the adverse scenario the EU banking system remains above 11% fully loaded CET1 ratio, higher than in previous stress tests.

Under the baseline scenario banks continue to increase capital through retained earnings, reaching an aggregate CET1 capital ratio of 16.9% by end-2027. All banks meet their overall capital requirement (OCR) with an aggregate EUR 526 bn of CET1 capital in excess of the end-2027 requirements.

Strong performance of the EU banks in the 2025 EU-wide stress test is reassuring, nonetheless, this should not lead to complacency among banks or supervisors. Maintaining adequate capital remains essential to ensure that the EU banking system can continue to support the economy under adverse conditions and avoid becoming a source of amplification during crises.

Introduction

The EU-wide stress test is an essential tool used by Competent Authorities (CAs) to evaluate the resilience of EU banks to severe but plausible shocks, identify residual vulnerabilities, and inform the supervisory decision-making process for appropriate mitigation actions. This stress test also enables CAs to determine whether the capital accumulated by banks in recent years is sufficient to cover losses and support the economy during stressed periods. The EU-wide stress test is initiated and coordinated by the EBA and undertaken in cooperation with CAs, the European Central Bank (ECB) and the European Systemic Risk Board (ESRB)[3].

The 2025 exercise includes a sample of 64 banks[4], 51 of which are from the euro area, representing about 75% of the total assets of EU banks. The number of banks has decreased compared to the 2023 EU-wide stress test, while the total assets have increased by roughly 3%[5]. Banks are tested against a baseline scenario and a hypothetical adverse scenario that assumes a severe but plausible economic shock. The results of this forward-looking exercise depend on several factors, including the health of the banking system at the starting point, the severity of the adverse scenario, the methodological assumptions, and other specific circumstances. These factors are elaborated on in the following subsections.

Banking system landscape

Since the previous stress test, the EU banking sector has shown solid performance with improvements in profitability and capital[6]. This positive trend has been driven partly by the increase in interest rates, which has supported banks’ net interest income. Despite macroeconomic uncertainties, banks have expanded their asset base, especially in the past year.

In 2024, EU banks maintained near-historic high profitability levels, with profits growing in the past two years by approximately 10% annually and a return on equity of 10.5%, up from 10.3% in 2023 and 8.1% in 2022. Higher profitability was driven by peaking net interest income (NII), but also due to improvements in net fee and commission income (NFCI) and net trading income (NTI), while the cost base has been increasing at a slower pace, despite the inflationary pressures. On boosting NII, banks successfully passed on interest rate increases to new loans, while ample liquidity and a stable deposit base helped contain interest expenses. Similarly, banks managed to increase NFCI and NTI, the latter also on the rise not least amid several periods of elevated volatility.

Capital levels remained strong in 2024, with the CET1 capital ratio rising to 16%[7], supported by retained earnings and other reserves. Since 2022 the volume of CET1 capital rose by around EUR 170 bn, helping the banking sector to be better prepared to absorb shocks and continue operations during periods of financial distress, enhancing financial stability. Due to consistently robust capital buffers and strong profitability, banks’ dividend distributions and share repurchases continued to rise in nominal terms, reaching EUR 68 billion in 2023 and EUR 92 billion in 2024, while the payout ratios have been consistently above 50% in the past three years.

Figure 1: EU banks’ key performance indicators (%)

Source: EBA supervisory reporting data

Source: EBA supervisory reporting data

Source: EBA supervisory reporting data

Source: EBA supervisory reporting data

Source: EBA supervisory reporting data

Source: EBA supervisory reporting data

Banks boosted their assets by 1.1% in 2023 and 3.2% in 2024, primarily driven by a significant increase in outstanding loans and advances, debt securities (mainly sovereigns), and equity holdings. Banks have somewhat reduced cash balances for interest bearing assets. Since the previous stress test, interest rates have peaked and then steadily decreased, reviving household lending in 2024, also supported by the stabilisation in real estate markets. Banks also increased lending towards non-financial corporations (NFCs). Sectoral exposures showed mixed developments, with energy sector and financial and insurance activities exposures growing the most.

Asset quality has stayed good and stable. While it seems that credit quality shows some signs of deterioration (increase of stage 2 loans), at end of 2024, the NPL ratio stood at 1.9%, only marginally up compared to the last 2 years. In historical terms, the NPL ratio is on a significantly lower tail of the distribution. Asset quality may be supported by lately decreasing interest rates, strong employment rates and the stabilisation of real estate markets, yet downside risks may emerge because of geopolitical shocks and the elevated level of economic uncertainty.

The adverse scenario

The adverse scenario used in the 2025 EU-wide stress test is severe by historical standards. It incorporates a sharp deterioration in the global macro-financial environment, driven by an aggravation of geopolitical tensions, entrenched trade fragmentation, and persistent supply shocks. These shocks contribute to a prolonged contraction in global activity, sharp rises in energy and commodity prices, inflationary pressures, a significant tightening in financial conditions, and broad-based corrections in asset prices.

As communicated in January at the launch of the 2025 exercise, the design of the adverse scenario draws upon a subset of the main financial stability risks to which the EU banking sector is exposed, as identified by the ESRB General Board and the narrative of the adverse scenario also reflects the EBA’s and ECB’s assessment of key vulnerabilities within the EU and global economies, and the main downside risks. The adverse scenario is hypothetical, based on a set of severe but plausible assumptions meant to generate adequate stress across all EU countries.

Severity of the adverse scenario

The 2025 stress scenario assumes a simultaneous and prolonged recession across the EU and other advanced economies, driven by severe global disruptions. These disruptions are caused by escalating geopolitical tension, particularly in the Middle East, and a rise in protectionist trade policies worldwide, including tariffs. This leads to higher energy prices and supply chain disruptions giving rise to supply-side inflationary pressures that are partially mitigated by depressed demand. Soaring macroeconomic uncertainty trade barriers generate a persistent and drastic decline in global and EU trade volumes, particularly affecting export-oriented economies and trade-intensive sectors and industries highly reliant on global value chains.

In the EU, real GDP is projected to fall by 6.3% between 2024 and 2027, with the sharpest contractions occurring in 2025 and 2026. Compared to the baseline projection, the adverse scenario implies a 10.4% deviation in EU real GDP by 2027, primarily driven by foreign factors but also reflecting the impact of domestic factors. Foreign shocks include the surge in commodity prices and the strong reduction in external trade. Domestic factors mainly reflect uncertainty, negative confidence effects and financial shocks. Tighter financing conditions, vulnerabilities in the non-bank financial sector and a sharp deterioration in financial market sentiment amplify adverse market dynamics. The adverse scenario assumes a strong and widespread increase in unemployment across the EU, with an average rise of 5.8 percentage points across the EU, peaking above levels seen during the GFC[8]. The projected unemployment is broadly in line with the increases featured in the previous exercise and is generally higher than in previous EBA adverse scenarios. The impact is more acute in economies with greater pre-existing labour market conditions or dependence on global trade. Trade-intensive sectors and industries highly reliant on global value chains are characterised by a stronger decline in production.

Contrary to the adverse scenario in the previous stress test, which implied the persistence of high inflation over the whole horizon, this year’s adverse scenario features a milder and more temporary increase in inflation. Similarly, in response to the inflation shock, market expectations for short-term risk-free interest rates rise modestly, with the one-year euro swap rate increasing to 3.3% in 2025 before decreasing to 3.0% in 2027, which is lower compared to the assumed increase in rates in the 2023 EU-wide stress test. The slope of the term structure of market rates under the adverse scenario is slightly inverted, with the yield curve flattening, while long term rates peak at around 4.8% (comparable to GFC levels) driven by reinforced sovereign debt sustainability concerns. In terms of GDP cumulative growth, the severity of the 2025 EBA adverse scenario is slightly higher than that of the 2023 exercise and materially higher when compared with previous exercises.

Figure 2: 2025 EU-wide stress test adverse scenario in comparison to previous EU-wide stress test scenarios, GFC and recent developments (in %)

Source: ECB and ESRB calculations (ECB, EC, Eurostat and Bloomberg data)

Source: ECB and ESRB calculations (ECB, EC, Eurostat and Bloomberg data)

Note: GFC peak-to-trough is computed as the max-to-min deviation in yearly indexed data during the period 2007-2010. 2025 peak-to-trough (“This year”) is computed as the min-max deviation in daily indexed data from 1 January 2025 to 25 June 2025 for equity prices, while other variables use the 2025 EC May 2025 forecasts. GFC peak is computed as the highest value in yearly rates during the period 2008-2010. 2025 peak is computed as the highest 2025 value for financial variables (LT rate, ST rate), while 2025 EC May 2025 forecasts are used for real variables (HICP inflation, unemployment).

The adverse scenario includes a severe and synchronised correction in global financial markets. EU equity prices fall sharply—by 50% in 2025, with only a modest recovery over the following two years. The tightening in financial conditions and deteriorating risk sentiment contribute to a significant fall in real estate prices, particularly in the commercial real estate (CRE) segment. CRE prices drop by 29.5% in three years, reflecting both cyclical weakness and ongoing structural shifts in post-pandemic demand, notably in the office segment. Residential real estate (RRE) prices also decline, albeit more moderately, with a fall by 15.7% by 2027. The slightly lower shock to RRE prices compared to the 2023 exercise is a result of lower pre-existing vulnerabilities in the residential real estate market in Europe.

While some elements of the adverse scenario have begun to materialise—such as the renewed imposition of trade tariffs by the U.S. administration and signs of re-escalating geopolitical tensions in the Middle East—economic activity in the EU and globally has remained relatively resilient. EU real GDP growth has slowed down but not contracted sharply, and inflation has not reached the elevated levels assumed under the adverse scenario but has rather been decreasing overall. Asset prices have also shown more stability than envisaged in the stress test. As such, the 2025 adverse scenario remains considerably more severe than the current outlook, serving as a rigorous test of the EU banking sector’s resilience to an extreme yet plausible downside event.

New features introduced in the 2025 EU-wide stress test

The methodology has undergone some important changes compared to the 2023 stress test. These changes were needed to integrate the Capital Requirements Regulation (CRR3) and to enhance key methodological aspects of net interest income (NII), market risk, operational risk and administrative expenses projections.

A revised scope was implemented for net interest income (NII) and projections have been centralised[9]. The change is in line with the work of the EBA on the future changes to the EU-wide stress test[10]. The centralisation of NII projections increases the comparability of results and decreases compliance costs for both banks and supervisors. Nevertheless, the stress test continues to provide useful insights about banks’ exposure to interest rates in adverse scenarios.

The revised methodology provides binding formulas to calculate the changes in asset and liability interest rates over the scenario horizon. Up to the 2023 EU-wide stress test, banks’ bottom-up input was often similar to the existing methodological constraints, highlighting that the methodology was already an effective instrument to assess NII projections under an adverse scenario. Therefore, banks only need to provide starting points as projections are produced automatically. This change standardises the application of the methodology while it allows for targeted bottom-up input from banks to allow capturing banks’ specificities[11].

For market risk, a more risk-sensitive approach has been introduced. Furthermore, proportionality has been enhanced by considering three types of banks based on the magnitude of their market risk exposures[12]. Concerning risk sensitivity, a new floor on held-for-trading gains and losses, based on the advanced standardised approach (ASA) risk exposure amount (REA) components, has been introduced. Additionally, the cap on the projections of client revenues from market making activity, has been revised to rely solely on historical client revenues. Finally, a more comprehensive approach has been designed for counterparty credit risk assessment, increasing the number of assumed defaulting counterparties from two to three.

In operational risk, the calibration of the floors defining minimum losses in the projections has been adjusted. It considers broader, including more recent, historical information on operational and conduct risk losses. As a result, for the adverse scenario the stress factor used has been reduced in the calibration of the floor for non-material and other operational risk, while it has been increased for the non-binding floor for material conduct risk projections. These floors may influence the projections in the adverse and baseline scenario.

Finally, a new template was introduced for administrative expenses to request more granular projections from banks with a breakdown by type of expenses with a geographical dimension[13]. These disaggregated projections of expenses enable authorities to better check and analyse how the inflation forecasts are reflected in this main component of banks’ profit and loss (P&L) statements.

Stress test and the new regulatory framework

The stress test is performed taking into account the EU banking package, (CRR3 and CRD VI), which entered into application as of 1 January 2025. Accordingly, banks had to restate their starting position of end-2024 to the CRR3[14]. While this decision seeks alignment with the newly introduced regulatory landscape, it is recalled the stress test remains a risk exercise.

The new regulation is introduced gradually through transitional arrangements. The report focuses on applicable capital ratios, considering all the applicable transitionals specified in the CRR3. These transitional arrangements allow institutions to adjust to the new rules over time. They progressively phase-in certain requirements, which will become stricter step by step until the full CRR3 rules are in place by 2033.

As the CRR3 is implemented over an extended timeline of eight years, institutions have room to continue adjusting their policies and portfolios towards full CRR3 implementation. For transparency, the report provides information on the capital ratios that would result from the phase-out of all the temporary arrangements embedded in the regulation until 2033 (“fully loaded capital ratios” or “capital ratios under 2033 rules”). However, the stress test results do not reflect future potential actions that banks may undertake to adapt to the new framework. This stems from the methodological “static balance sheet assumption” of the stress test, which does not allow to anticipate ex-ante any future changes in the balance sheet composition. In addition, there are different time horizons at stake, as the stress test focuses on the 2025-2027 period, while the transitional arrangements introduced by the CRR3 last until 2033. Hence, reported “fully loaded capital ratios” may evolve going forward for banks that take action in adapting to the full CRR3, while this is not reflected the 2025 EU-wide stress test.

|

Box 1: Restatement from CRR2 to CRR3

Box 1: Restatement from CRR2 to CRR3

In general, the CET1 capital ratio on a “fully loaded” basis is lower compared to the applicable transitional basis (see next section: Main findings). This is mainly due to the increase in risk-exposure amounts (REA) associated with the removal of the transitional arrangements, which mechanically lowers the capital ratio. Further, on a fully loaded basis REA is adjusted upwards compared to the transitional basis, as the transitional arrangements are lifted. This affects both the starting point and the projections of the stress test. This is compounded with a REA which set to increase at the end of the adverse scenario due to the macro-economic shock. Hence, capital depletion, which compares the starting and end-point capital ratios, tends to be lower on a fully loaded basis than on a transitional basis[15].

Main findings

Overview of aggregate results

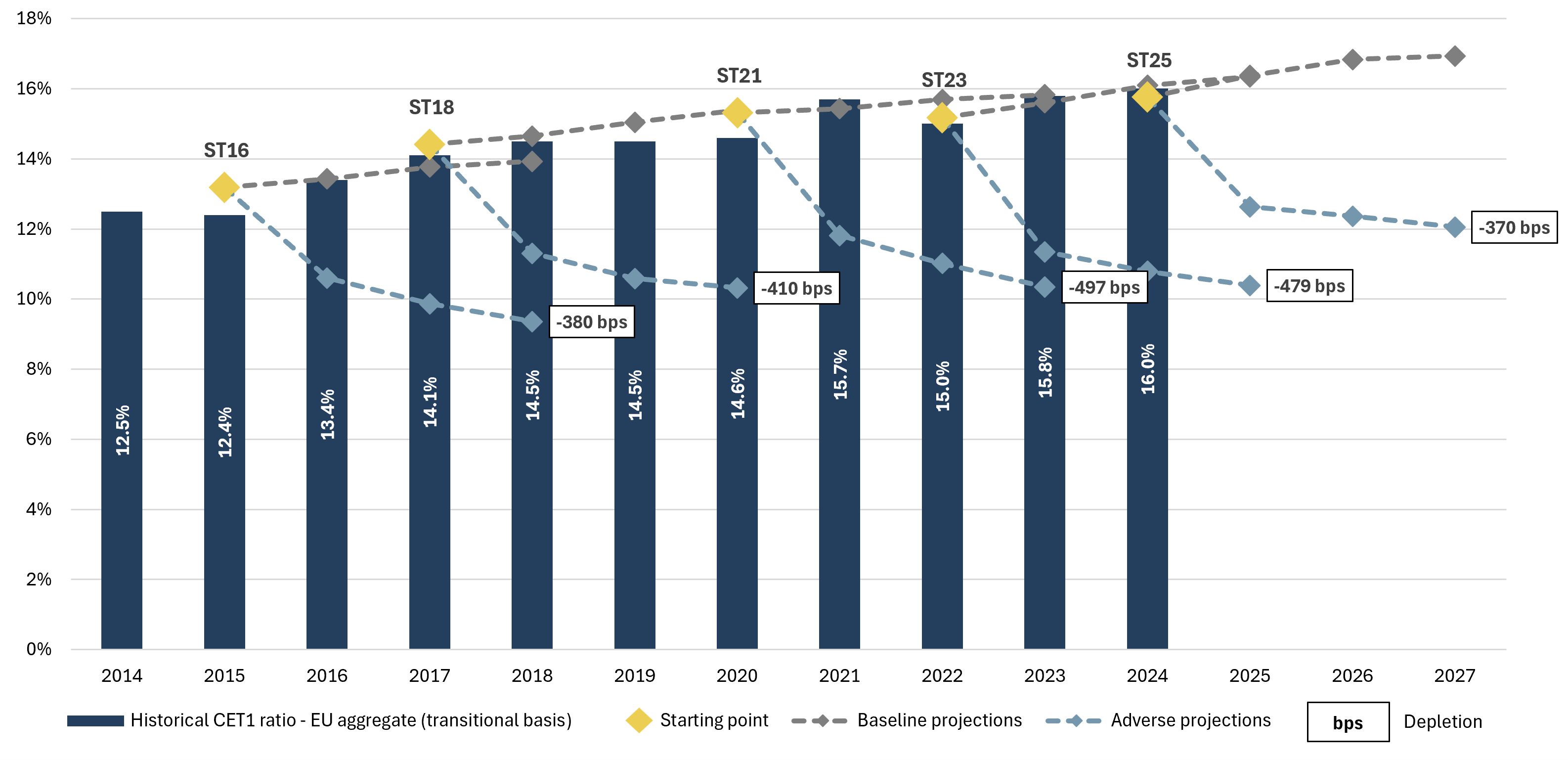

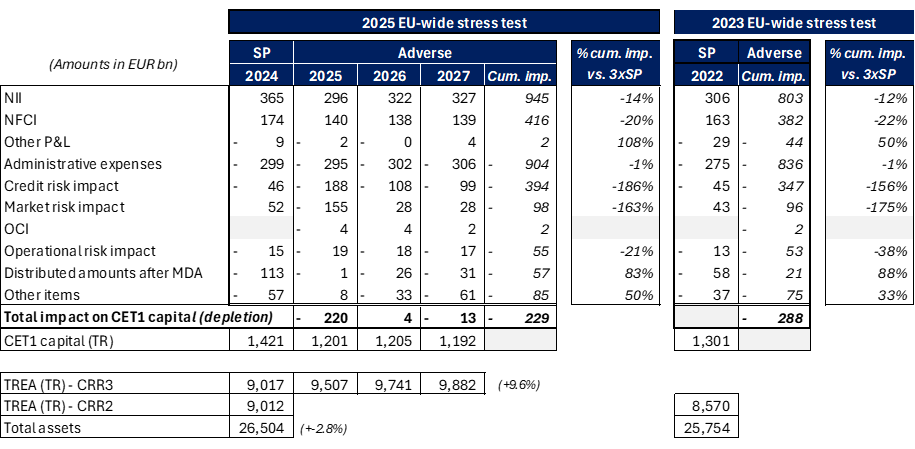

Banks participating in the 2025 EU-wide stress test reported an aggregate 15.8% CET1 ratio at the beginning of the exercise (under CRR3 rules)[16]. The aggregate CET1 capital ratio depletion amounts to 370 bps[17] at the end of the stress test horizon under the adverse scenario (Figure 5). This results in a 12.1% aggregate CET1 ratio at the end of the adverse scenario. The median CET1 ratio reaches 13.0% and the inter-quartile range becomes 11.0%-15.5% at the end of 2027 (Figure 6, left). The depletion is lower compared to the 2023 exercise, when the CET1 ratio dropped by 479 bps, mostly because banks entered the 2025 exercise with stronger starting points and an improved ability to generate income, as explained in more details in the next sections.

On average, the maximum depletion of the CET1 ratio under the adverse scenario occurs in the third year of the horizon (2027). This also holds at individual level for most banks in the sample (33 banks). However, for 25 banks the “peak-to-trough” depletion occurs during the first year of the horizon and for 6 banks in the second year (Annex I). This notably depends on (i) how banks are affected by the market risk shock, which is concentrated in the first year, (ii) how fast a recovery of income sources and credit losses is projected and (iii) the path of the projected total risk exposure amount over the 3-year horizon.

Source: 2025 EU-wide stress test data and EBA calculations

Note: This chart shows the change in basis points (bps) of the aggregate transitional CET1 ratio over all three years of the horizon under the adverse scenario compared to the end-2024 starting point restated under CRR3 rules.

Under the adverse scenario, no bank breaches its CET1 total SREP capital requirement (TSCR)[18] and banks in the sample collectively have EUR 554 bn of CET1 capital in excess of their TSCR requirements[19].

Banks start the exercise with a 5.77% aggregate leverage ratio (LR)[20] which decreases to 4.92% as of end-2027, under the adverse scenario. The median leverage ratio reaches 5.32% at the end of the horizon and the inter-quartile range becomes 4.46%-6.80% (Figure 6, right). Hence both starting and end points of this ratio remain on average far above the regulatory minimum. One bank would fall below its Tier 1 total SREP leverage ratio requirement (TSLRR, i.e. 3% plus applicable pillar 2 requirement).

Under the adverse scenario, there are 17 banks breaching their MDA trigger and/or LR-MDA trigger during at least one year of the horizon. These banks need to adjust their distributed amounts (e.g. reduce some variable remuneration, restrict dividend payments, etc.), which overall has a +43 bps impact on the aggregate projected end-2027 CET1 ratio.

Source: 2025 EU-wide stress test data and EBA calculations

Source: 2025 EU-wide stress test data and EBA calculations

Note: boxplots show minimum, 1st quartile, median, 3rd quartile, maximum and aggregate ratio.

|

Individual results

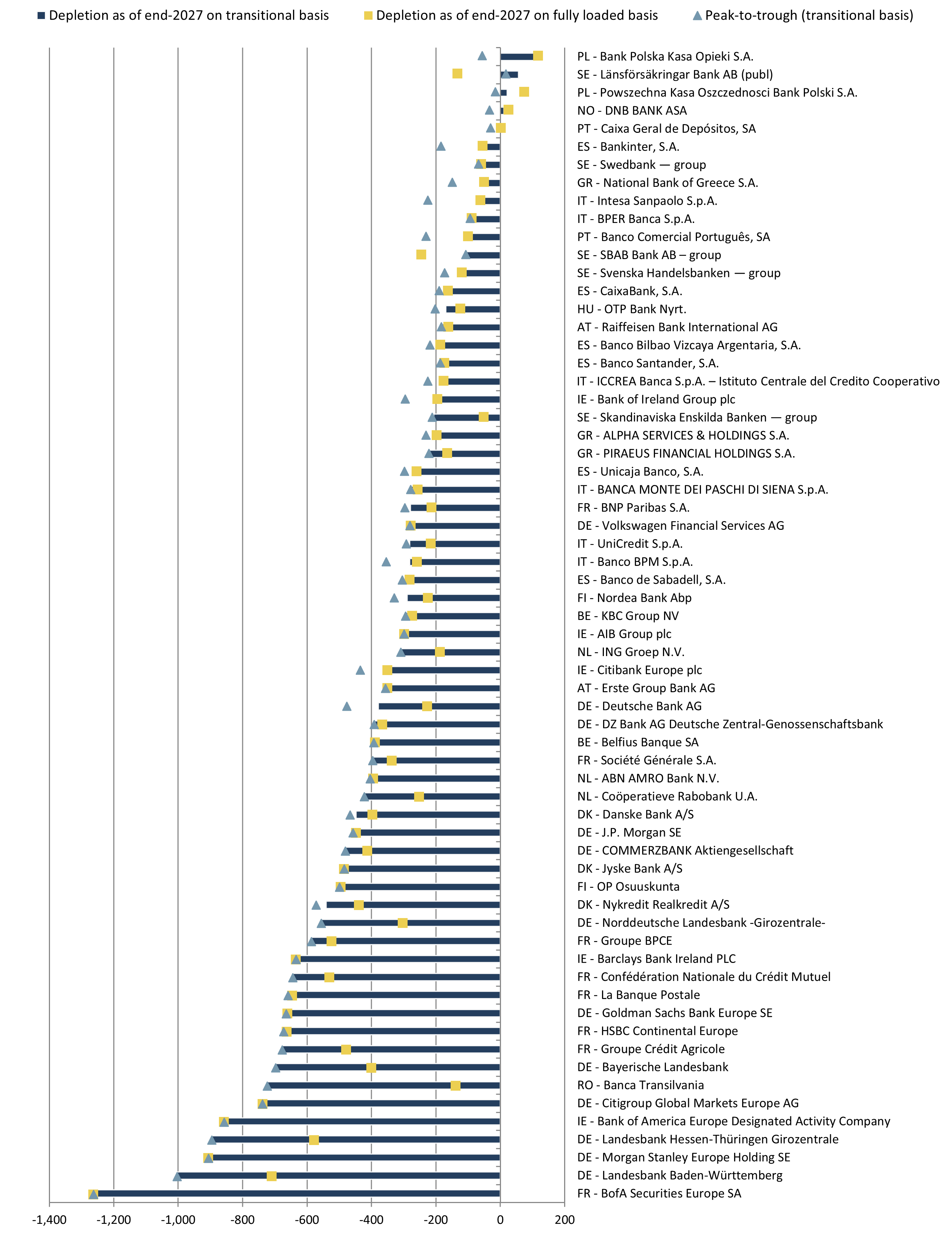

Figure 10: Bank-level CET1 ratio depletion under the adverse scenario (in bps)

Source: 2025 EU-wide stress test data and EBA calculations [DOWNLOAD DATA]

Note: This chart shows the change in the CET1 ratio (depletion) from the end-2024 starting point (restated under CRR3 rules) to the end-2027 projected ratio under the adverse scenario. This depletion as of end-2027 is shown on transitional basis (blue bar) and fully loaded basis (yellow square). Grey triangle represents for each bank the “peak-to-trough” on a transitional basis, i.e. the maximum depletion (on transitional basis) over the 3 years of the horizon, which does not always occur in 2027 for some banks.

The impact of the adverse scenario on the CET1 ratio ranges from +106 bps to -1,263 bps, as shown in Figure 10 which presents for each bank the CET1 ratio depletion implied by the adverse scenario[22]. This depletion of CET1 ratio is measured between the end-2024 starting point and the end of the horizon in 2027, however the maximum depletion does not necessary occur in 2027 for all banks. Therefore Figure 10 also displays for each bank the "peak-to-trough", which shows negative impact except for one bank.

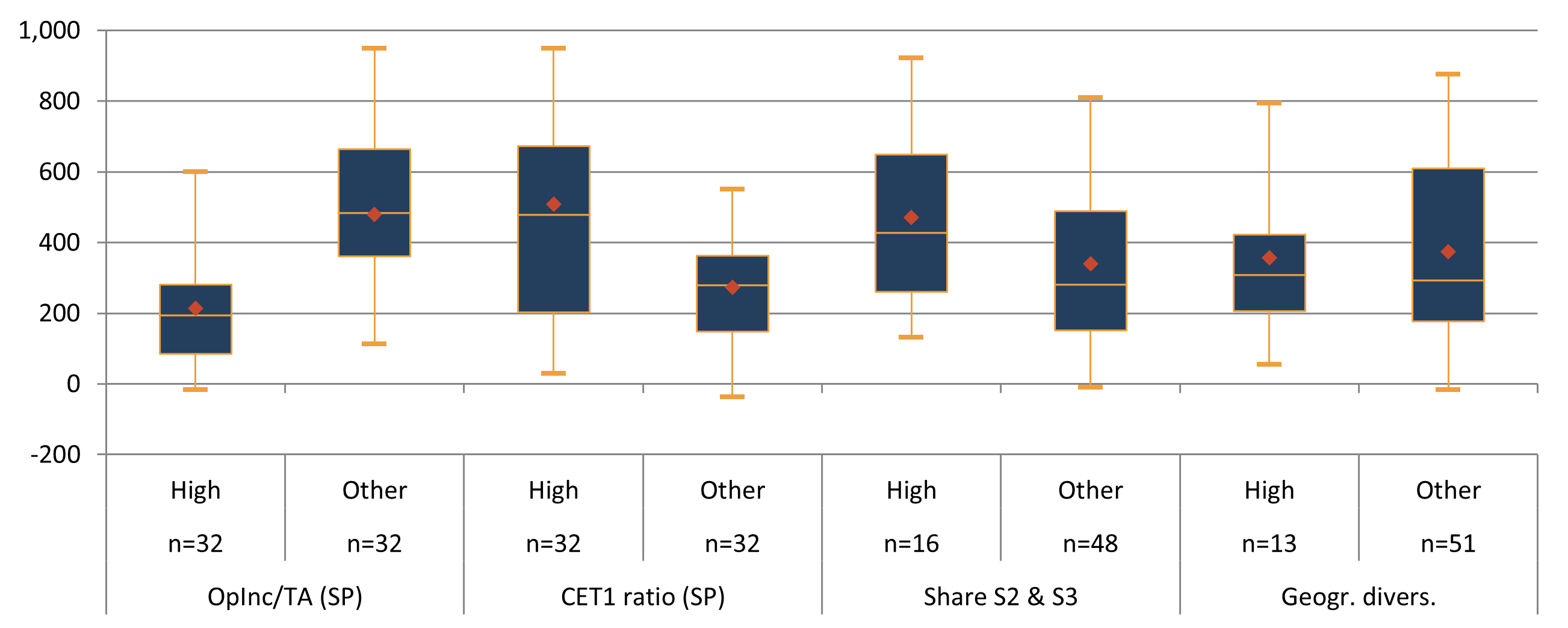

The magnitude of the CET1 ratio depletion varies across banks according to certain characteristics (Figure 11). Banks that have a high level of net operating income at the start of the exercise tend to experience lower depletion in the stress test. This is because this strong income generation capacity helps them to better withstand the shocks stipulated under the adverse scenario. Banks with higher starting point CET1 ratio usually have larger depletion, since for some banks this additional initial capitalisation might cover ex-ante some risks that materialise during the adverse scenario. Additionally, banks that have more assets in stage 2 or stage 3 have more depletion, as this can generate larger credit risk losses over the horizon. Finally, geographically more diversified banks tend to have a depletion more centred around the median (more limited dispersion), which indicates that geographical diversification helps them to avoid the largest depletions.

Figure 11: Distribution of three-year CET1 ratio depletion under the adverse scenario for several clusters of banks (in bps)

Source: 2025 EU-wide stress test data and EBA calculations [DOWNLOAD DATA]

Note: Boxplots show 5th percentile, 1st quartile, median, 3rd quartile, 95th percentile and weighted average. “OpInc/TA (SP)” splits the sample between banks having starting point (SP) of net operating income (OpInc), scaled by total assets (TA), above or below the median value. Similarly, “CET1 ratio (SP)” splits the sample between banks above/below the median CET1 ratio as of end-2024 (CRR3-restated). “Share of S2 & S3” isolates the first quartile of banks with larger share of exposures respectively classified as stage 2 or stage 3 under IFRS9 at end-2024 starting point. “Geographic diversification” is based on the number of NII country-currency pairs reported in the stress test data: banks with more than 20 pairs are classified as highly diversified.

Key drivers of the aggregate results

Under the adverse scenario, net earnings[23] contribute to an increase of the CET1 ratio by 509 bps. This is offset by credit risk, market risk and operational risk losses, which respectively account for -437 bps, -108 bps and -61 bps impact (Figure 12). Projections of distributed amounts – after MDA-related restrictions – over the three years reduce further the aggregate CET1 ratio by -64 bps (compared to -24 bps in the last stress test). This highlights the improved profitability of banks which raised their dividend payout. During the 2023 EU-wide stress test, the median projected payout ratio in profitable years under the adverse scenario was 32% compared to 50% in this exercise. Other items, which include taxes, reduce the CET1 ratio by -95 bps. Finally, banks’ CET1 ratios are impacted not only by the capital depletion, on the numerator, but also by the increase of the risk exposure amount (REA) – denominator of the CET1 ratio –, with an aggregate impact of -116 bps.

Figure 12: Main components of CET1 ratio change from 2024 to 2027 under the adverse scenario (in % of TREA at end-2024 restated under CRR3 rules)

Source: 2025 EU-wide stress test data and EBA calculations [DOWNLOAD DATA]

Note: Due to rounding effects, totals may not add up to the sum of components.

Aggregate CET1 capital as of end-2024 restated under CRR3 amounts to EUR 1,421 bn[24]. This is much higher than the starting point of the previous stress test (EUR 1,301 bn of CET1 capital under CRR2 as of end-2022) and shows the improvement of EU banks’ capital positions over the last two years (Table 1). Under the adverse scenario, banks end up with an aggregate EUR 1,192 bn of CET1 capital as of end-2027, resulting in an absolute depletion of CET1 capital of EUR 229 bn. In comparison, during the 2023 EU-wide stress test, banks ended the exercise with an aggregate CET1 capital of EUR 1,013 bn and a depletion over a three-year horizon of EUR 288 bn. This relatively milder depletion of CET1 capital compared to the last exercise is mostly driven by the resilience of the main income components - NII and NFCI. On the other hand, the projected depletion of CET1 capital related to administrative expenses, market and operational risks remain larger or of similar scale compared to the previous stress test. It should also be noted that although credit risks losses were similar at the beginning of both exercises, banks recognised higher credit losses during this year’s exercise.

Table 1: Evolution of aggregate CET1 capital under the adverse scenario (in EUR bn)

Source: 2025 and 2023 EU-wide stress tests data and EBA calculations [DOWNLOAD DATA]

Note: This table shows the 2024 starting point (SP) of the main drivers of the yearly change in CET1 capital. The year-by-year impact of the adverse scenario on these components is presented in columns “2025”, “2026” and “2027”, as well as the cumulative impact (“Cum. imp.”) over the 3-year horizon. This 3-year cumulative impact of the adverse scenario is then compared to 3 times the absolute value of the initial starting point level in columns “% cum. imp. vs. 3xSP” (this implies for instance that the generated EUR 945 bn of NII over the 3 years of the horizon are 14% lower than if the EUR 365 bn starting point had stayed constant over this period). For the sake of comparison, the last three columns show for the previous (2023) EU-wide stress test: the 2022 starting point, the cumulative impact of the adverse scenario and the relative comparison of this cumulative impact versus 3 times the starting point absolute value. The two figures in brackets shows the growth rate of total risk exposure amounts (TREA) under CRR3 rules on transitional (TR) basis from end-2024 to end-2027, and the change in total assets from end-2022 to end-2024, respectively.

Drivers of capital depletion

Banks generated EUR 181 bn of aggregate profits (after tax) in 2024. This substantially higher profitability at the start of the exercise acts as a first safety net – on top of accumulated capital - and helps banks absorb projected losses over the horizon and mitigate the impact on capital. Figure 13 shows the evolution of the main profit and loss (P&L) components under the adverse scenario, while annex IV provides a more detailed breakdown of the aggregated P&L statement.

This strong aggregate profit in 2024 then turns into a net loss of EUR 114 bn in 2025, when most of the impacts of the adverse scenario occur. This is mainly driven by the projected spike in credit risk impairments (from EUR 46 bn in 2024 to EUR 188 bn in 2025), the reduction in net interest income and net fee and commission income, as well as net trading income turning negative in the first year of the horizon. The last two years of the stress test horizon then show a partial and gradual recovery with a net profit of EUR 42 bn in 2026 and EUR 54 bn in 2027. The cumulative profit or loss for the three years under the adverse scenario amounts to a net loss of EUR 18 bn. Assuming that the 2024 profitability level had stayed constant over this three-year horizon, this would imply that the adverse scenario has removed a total of EUR 562 bn of profit compared to a no-change situation[25].

Source: 2025 EU-wide stress test data and EBA calculations

Net income

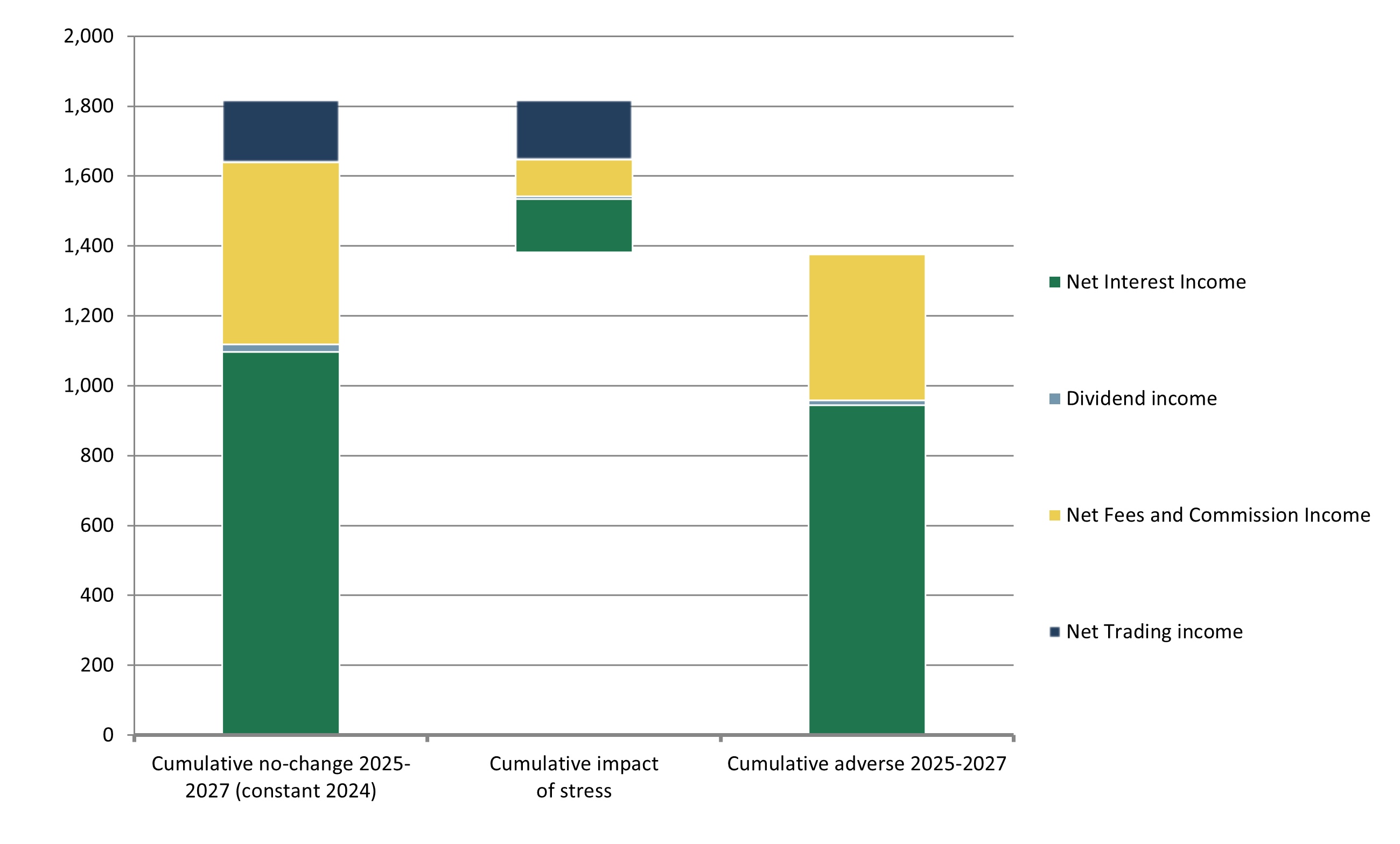

The adverse scenario has decreased banks’ aggregate net income by EUR 436 bn over the three years compared to a situation where 2024 starting points would have stayed constant. Figure 14 compares the cumulative projected P&L contribution of banks’ main sources of income[26] to their hypothetical “no-change” contribution (i.e. keeping constant the net income of 2024 over the three years of the stress test). The negative impacts resulting from the application of the adverse scenario are EUR 171 bn on NTI, EUR 152 bn on NII, EUR 105 bn on NFCI and EUR 8 bn on dividend income, summing up to EUR 436 bn of lost income over three years due to stress.

Figure 14: Cumulative impact of the main sources of income over 2025-27 under the adverse scenario, compared to the hypothetical no-change contributions to P&L (in EUR bn)

Source: 2025 EU-wide stress test data and EBA calculations [DOWNLOAD DATA]

Note: The first stacked bar “Cumulative no-change 2025-2027 (constant 2024)” represents a hypothetical situation where the observed levels of incomes in 2024 would remain constant over the horizon. These amounts then equal three times the starting points. The third bar “Cumulative adverse 2025-2027” shows the amounts projected under the adverse scenario over the three years. The second bar in-between “Cumulative impact of stress” is the absolute difference between the two situations, comparing the projections under the adverse scenario versus the hypothetical no-change situation, measuring the extent to which the adverse scenario results in a decline of banks’ sources of income.

Net interest income

In the adverse scenario, NII provides a significant cushion for absorbing losses. The cumulative NII amounts to EUR 945 bn, over the three years adverse scenario horizon (Figure 15). During 2025, which is the year of the adverse scenario with the largest decline in aggregate NII, aggregate NII declines by 18.8% compared to the starting point and 24.4% relatively to the baseline scenario projection for the same year. The relative decline compared to the starting point and the baseline scenario is like that recorded in the 2023 stress test.

Source: 2025 EU-wide stress test data and EBA calculations

Note: The chart shows the aggregate NII for banks in the 2025 EU-wide stress test sample for each year of the baseline and the adverse scenarios. The 2024 aggregate NII is the starting point which is common for both scenarios.

Aggregate NII varies significantly across banks over the adverse scenario. Differences are explained by the starting point and the adverse scenario path of interest rates (Figure 16). Banks must reprice their assets and liabilities in line with the hypothetical interest rate paths. Nevertheless, the exact impact of the adverse scenario on each bank is not only a function of the path of interest rates, but also each bank’s balance sheet structure and business model.

Source: 2025 EU-wide stress test data and EBA calculations

Note: The vertical bars measure the three-year contribution of NII to banks’ capital. Each bar is calculated as the sum of NII over the three-year horizon scaled by total REA as of end 2024, restated for the application of CRR3 rules. The horizontal bar shows the same metric calculated for the whole 2025 EU-wide stress test sample.

The difference in the maturity profile of assets and liabilities drives differences across banks. A large share of banks' assets and liabilities reprice over the scenario horizon (Figure 17, left). Overall, the share of liabilities repricing over the scenario is higher than that of assets because of their shorter maturity schedule compared to assets. As assets reprice over the remaining scenario horizon, NII recovers from the initial decline. As the yield curve is inverted in the adverse scenario, assets reprice at lower interest rates compared to the starting point, resulting in lower total NII at the end of the scenario horizon. The average yield change for assets is generally lower than for liabilities, leading to a reduction of the net interest margin and therefore the net interest income (Figure 17, right).

Source: 2025 EU-wide stress test data and EBA calculations

Source: 2025 EU-wide stress test data and EBA calculations

Note: The left chart is calculated as the share of assets (liabilities) which reprice over the three-year scenario over total assets (liabilities) at the end 2024 (starting point of the stress test). The calculation considers fixed rate assets (liabilities) which mature and floating rate assets (liabilities) which are subject to index rate reset. The calculations are at the bank level and the distributions are shown separately for assets and liabilities. The boxplot shows interquartile range, median, the 5th and 95th percentiles. The red dot and connecting line show the mean. The right chart shows on the vertical axis the change in the effective interest rate (EIR), which is the average interest income (expense), on assets (liabilities) between the end of the three-year adverse scenario horizon and the starting point (end 2024). The horizontal axis shows the assets (liabilities) repricing over the three-year adverse scenario horizon as a share of the assets (liabilities) at end 2024. The EIR calculations do not include derivative positions.

The type of banks’ assets and liabilities also plays an important role in how the scenario impacts banks' NII. Interest income from loans and advances and interest expense from deposits are the main contributors to banks' NII (Figure 18). On aggregate, loans and advances represent 86% of banks’ assets (excluding derivatives), out of which 55% are loans to households and non-financial corporations and the remaining are other loans, such as interbank loans to credit institutions and central bank assets. Deposits to households and non-financial corporations and debt securities issued are 57% and 21.5% of banks’ liabilities (excluding derivatives), respectively. Other deposits from credit institutions and repurchase agreements (repo) correspond to around 20% of liabilities (excluding derivatives). The behaviour of different asset and liability items influences how the scenario affects the aggregate NII projections.

Source: 2025 EU-wide stress test data and EBA calculations

Note: The chart is calculated as the aggregate interest income or interest expense related to each balance sheet item. Each bar shows the three years interest income or expense over the adverse scenario horizon. For derivatives and other assets and liabilities, interest income and expenses are presented on a net basis. Loans HH&NFC includes interest income from loans and advances to households and non-financial corporations. The Loans Other category includes loans and advances to Central Banks and Credit Institutions. Deposits HH&NFC includes interest expense on deposits from households and non-financial corporations. The Deposits Other category includes deposits from Central Banks and Credit Institutions. The impact of the cap refers to the NII cap calculated in accordance with paragraphs 404 and 405 of the 2025 EU-wide stress test methodological note. The income from Held-for-Trading (HfT) instruments refers to NII calculated in accordance with Section 4.5 of the 2025 EU-wide stress test methodological note.

Banks which focus more on retail business show higher NII resilience compared to other banks due to their reliance on households and non-financial corporations’ overnight deposits. Funding costs from overnight deposits from households and non-financial corporations increase less compared to funding costs from other liabilities. As a result, retail focused banks project higher NII contribution compared to banks more focused on wholesale and market activities. Overnight deposits from non-financial corporations and households tend to have a lower interest expense at the starting point, and they are less impacted by changes in interest rates compared to other liabilities over the adverse scenario horizon. On the other hand, the interest earned on loans to households and non-financial corporations increases less than the income from other assets (Figure 19).

Source: 2025 EU-wide stress test data and EBA calculations

Note: The chart shows the median increase in the interest rate (effective interest rate or EIR) of interest earning assets and liabilities, excluding derivative positions. Each bar represents the median cumulative change of the EIR over the three-year adverse scenario horizon separately for loans and deposits related to households and non-financial corporations and other non-derivative assets.

|

Net fee and commission income and dividend income

After net interest income, net fee and commission income (NFCI) is the second largest income source for banks, totalling EUR 174 bn in 2024. In the same period, the sum of NFCI and dividend income (EUR 7.4 bn) amounted to EUR 181 bn, which is higher compared to the last stress test when it totalled EUR 168 bn in 2022.

Under the adverse scenario, NFCI drops from EUR 174 bn to EUR 140 bn in 2025 (-19.5%) and remains close to this depleted level in 2026 and 2027 with EUR 138 bn and EUR 139 bn, respectively. Over this three-year period, this implies a cumulative reduction of EUR 105 bn compared to a situation where the unstressed 2024 level had stayed constant over the horizon (Figure 14). Hence, the stressed NFCI projections contribute to an increase of the aggregate CET1 ratio by 462 bps (Figure 12), while a constant 2024 level of NFCI over the 3 years would have increased the CET1 ratio by 578 bps.

Dividend income reduces from EUR 7.4 bn in 2024 to EUR 5.9, 4.0 and 4.2 bn respectively over the three years of the horizon, resulting in a total cumulated loss of income of EUR 8.0 bn under the adverse scenario compared to a no-change[27] situation (Figure 14).

|

Expenses

Banks in the sample report an aggregate amount of expenses equal to EUR 397 bn in 2024[30]. Projections of these expenses are subject to a methodological floor. This means that projections cannot fall below the 2024 level, subject to some “one-off” adjustments as explained below.

Banks may request adjusting some of their floors on expenses for some non-recurrent exceptional events that affect the starting point level and would no longer materialise over the three years of the horizon. These so-called “one-off” adjustment applications are reviewed by competent authorities and must be approved by the EBA Board of Supervisors. Banks submitted 71 one-off applications, of which 39 were accepted, resulting in an overall impact of +17 bps on the aggregate CET1 ratio[31]. The median impact of the accepted one-off cases on the bank-level CET1 ratio is +22 bps.

Banks project expenses gradually increasing over the three years of the horizon. The cumulative expenses projected over the three years under the adverse scenario equal EUR 1,197 bn, which is EUR 36 bn higher than if banks had projected expenses equal to the 2024 floor adjusted for one-off events. This means that banks partly factor the inflation forecast of the adverse scenario into these aggregate projections. An analysis of the projections of expenses broken-down by type of expenses and geography has also been conducted to measure to which extent they correlate with the detailed country-level inflation rates of the scenarios.

On average a one percentage point increase in inflation would result in a 0.80 percentage point increase of total administrative expenses under the baseline scenario. This observed pass-through rate of inflation to the growth of expenses is rather homogeneous across all types of expenses under the baseline scenario.

Under the adverse scenario, the overall projected pass-through rate of inflation would drop to 0.42 since under a macroeconomic turmoil banks would try to reduce their cost increase[32]. The pass-through rate of inflation would generally be reduced on fixed remuneration expenses compared to the baseline scenario and it would even turn negative for variable remuneration expenses, as banks would reduce them to maintain a stable total staff expenditure (which accounts for 63% of total administrative expenses). On the other hand, for non-staff related expenses (37% of total), like IT costs or real estate and leasing expenses, the inflation pass-through rate remains close to 0.80 under the adverse scenario, since those expenses are harder to compress in the short-run, but a reduction of the pass-through is observed on more flexible expenses such as consulting, advertising and marketing costs. All these observed effects derived from the analysis of the granular projections seem consistent with expectations and the ability of banks to provide projections of expenses reflecting the inflation component of the scenarios.

Credit risk

Aggregate credit risk losses over the adverse scenario amount to EUR 394 bn EUR, with the largest impact during the first year (Figure 21, left). In line with previous exercises, this is explained by the time profile of the scenario, where the hardest impact is recorded in the first year. This is coupled with the stress test assumption that banks know in advance the path of the macro projections, hence they are able to reflect the full impact of the scenario on the calculation of LGD/loss rates and lifetime expected credit losses[33].

Credit risk losses represent 1.9% of total exposures at the end of 2024 and result in a capital depletion of 437 bps, with significant dispersion across participating banks, ranging from a negative effect of 828 bps to a negligible impact of 10 bps (Figure 21, right).

Source: 2025 EU-wide stress test data and EBA calculations

Source: 2025 EU-wide stress test data and EBA calculations

Note: The left chart displays the aggregated credit risk losses for all the institutions participating in the 2025 EU-wide stress test over the 2025-2027 stress test horizon under the adverse scenario. The right chart shows the CET1 ratio depletion that results from credit risk losses under the adverse scenario. This is displayed at individual bank level, together with the sample average.

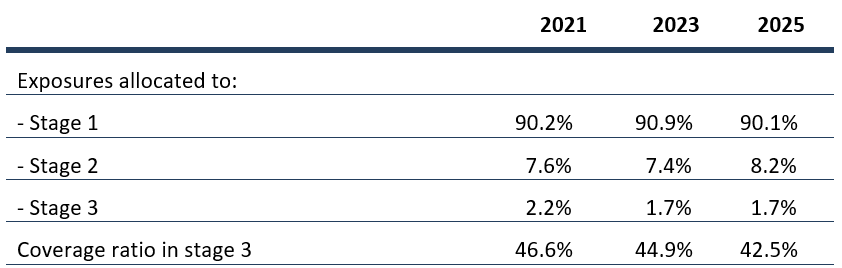

Credit risk losses are more pronounced than in the 2023 EU-wide stress test. Despite losses being similar at the starting point under both exercises, cumulative losses over the stress test horizon rise to EUR 394 bn compared to EUR 347 bn in the 2023 exercise, i.e. an increase in impairments of around 15%. Factors explaining this difference are the scenario severity and the credit quality at the starting point of the exercise, where the share of stage 3 exposures remains broadly stable compared to the 2023 stress test, albeit the share of stage 2 exposures has been ticking up and the coverage ratio of non-performing loans has continued to slowly decrease (Table 3).

Table 3: Credit quality metrics at the starting point of the 2021, 2023 and 2025 EU-wide stress test exercises

Source: EU-wide stress test data, EBA calculations [DOWNLOAD DATA]

Note: The figures in this table are after restatements and correspond to the beginning of the adverse scenario.

Management overlays continue to cushion credit risk losses, amounting to EUR 18.4 bn (EUR 25.0 bn in the 2023 exercise) or 8.1% of total provisions (10.2% in 2023). Their use is heterogeneous, with around 25% of banks not reporting any management overlays. Around 85% of management overlays are allocated to performing exposures (mainly stage 2 exposures). Management overlays are consumed entirely over the first year of the stress test horizon and reduce credit losses accordingly.

Credit risk losses vary depending on the underlying portfolio banks are exposed to. On aggregate, the share of stage 2 and stage 3 exposures increases from 8.2% and 1.7% at the beginning of the exercise to 13.7% and 6.0% at the end of the adverse scenario, respectively. The coverage ratio decreases in that period from 42.5% to 38.8%. Retail displays the higher projected loss rates[34] (Figure 22), reflecting the riskier nature of consumer loans and credit cards. Albeit retail represent a modest share of total exposures, at below 10%, it concentrates almost 30% of projected credit risk losses. The second higher projected credit risk losses stem from SMEs, followed by corporate real estate, which may be backed by either commercial or residential real estate.

Commercial real estate (CRE) shows a notable increase in the share of stage 3 exposures over the stress test horizon, rising on aggregate level from 4% at the starting point to 12.7% at the end of the adverse scenario[35]. This deterioration is more pronounced compared to the 2023 EU-wide stress test, where the share of stage 3 exposures evolved from 3.2% to 10.3% over the adverse scenario, highlighting the increased vulnerabilities in CRE. Further, the share of stage 2 is projected to increase from 17.5% at the starting point to 23.2% at the end of the adverse scenario, a weakening in credit quality that adds further pressure to CRE exposures.

Source: 2025 EU-wide stress test data and EBA calculations

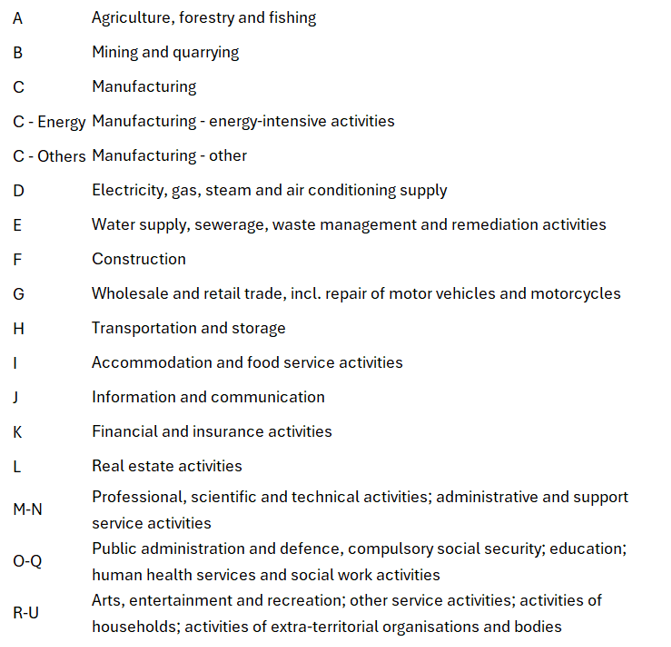

Note: The portfolios are displayed ordered by the loss rate, which is defined as the cumulative projected losses over the adverse scenario, relative to the exposure value (performing and non-performing) at the starting point of the exercise (end-2024). Relative size refers to the ratio of the exposure value of the portfolio relative to total exposures. Relative losses refer to the projected losses of the portfolio over the scenario, relative to projected total losses over the scenario. The portfolios are defined as follows, based on the underlying SA/IRB regulatory exposure classes, where the stress test data are reported: “Public sector” refers to central banks, central governments, regional governments or local authorities, public sector entities, multilateral development banks and international organisations; “Other” refers to Collective Investment Undertakings, securitisations, subordinated debt exposures, covered bods, claims on institutions and corporates with a short-term credit assessment and other exposures and non-credit obligation assets; “Residential real estate” refers to retail residential estate as defined in the IRB and residential real estate as defined in the SA; “Corporate” excludes exposures secured by real estate and SMEs; “Corporate real estate” refers to the IRB corporate exposures secured by real estate (where the underlying assets may be commercial or residential real estate), together with SA commercial real estate; “Retail” excludes SMEs and refers to IRB retail excluding residential real estate and to SA retail, which excludes real estate; “SMEs” refers to retail and corporate SMEs.

Credit losses by sector of economic activity

The sectoral analysis of non-financial corporations (NFCs) credit losses helps to understand how the narrative of the scenario is translated into banks’ credit risk loss projections[36]. Credit losses from NFCs exposures account for around half of total credit losses over the adverse scenario[37]. At the end of 2024, exposures to four sectors of economic activity account for almost 60% of all credit risk exposures to NFCs (Figure 23). Most exposures to NFCs were towards firms operating in the real estate (L) and manufacturing sectors (C), followed by firms operating in the wholesale and retail trade (G) and financial services sectors (K). The sectoral exposure allocation is barely unchanged compared to the starting point of the 2023 EU-wide stress test.

Source: 2025 EU-wide stress test data and EBA calculations |

|

Some shifts have occurred in the underlying sectoral credit quality since the starting point of the 2023 EU-wide stress test. Credit quality continues to vary across sectors at the starting point of the stress test (Figure 24). The accommodation and food services (I) sector continues to record the highest share of stage 3 exposures compared to other sectors. However, asset quality for this sector has significantly improved compared to the starting point of the 2023 EU-wide stress test (end 2022), when firms in the accommodation and food services (I) sector had only started to recover after the COVID-19 pandemic lockdowns. Exposures towards firms in sectors which are vulnerable to the adverse scenario narrative, such as agriculture (A), mining and quarrying (B), manufacturing (C) and transport and storage (H) also show similar or somewhat improved asset quality compared to end 2022. On the other hand, exposures towards firms with activities in the wholesale and retail trade (G) sector, which is also vulnerable to the adverse scenario narrative, show a slight increase in the share of stage 2 and stage 3 exposures between end 2022 and end 2024.

Source: 2025 EU-wide stress test data and EBA calculations

Overall, the impact of the scenario is heterogeneous on the different sectors of economic activity. The impact of the adverse scenario on NPE and loss rates varies significantly across sectors (Figure 25). The adverse scenario loss rates correlate to the increase of NPE as banks adjust their loan loss allowances to cover the inflow of new NPEs[38].

Source: 2025 EU-wide stress test data and EBA calculations

Note: The NPE (stage 3) cumulative change is the ratio of the cumulative increase in the NPE (stage 3) exposures over the adverse scenario horizon divided by performing exposures at the starting point. The loss rate is calculated as the change in the stock of provisions between the end of the adverse scenario horizon and the starting point divided by total exposure (performing and non-performing) at the starting point.

The projections reflect the scenario narrative on the sectoral break-down of corporate credit losses. NPE increases and loss rates over the adverse scenario are, on aggregate, higher for those sectors which are more vulnerable to the adverse scenario narrative and are therefore impacted more compared to other sectors (Figure 26). These sectors represent 39% of banks’ total NFC exposures. The impact on the manufacturing (C) sector is mostly driven by the scenario impact on energy intensive activities which are more exposed to geopolitical risks and energy price increases materialising over the scenario horizon. On the other hand, sectors which are less trade intensive, and less export oriented such as water supply, sewage, and waste management (E) or professional, scientific and technical activities (M-N), record lower loss rates and smaller increases in the NPE ratio over the adverse scenario.

Source: 2025 EU-wide stress test data and EBA calculations

Note: The NPE (stage 3) cumulative change is the ratio of the cumulative increase in the NPE (stage 3) exposures over the adverse scenario horizon divided by performing exposures at the starting point. The loss rate is calculated as the change in the stock of provisions between the end of the adverse scenario horizon and the starting point divided by total exposure (performing and non-performing) at the starting point. The chart shows the two metrics over the adverse scenario for two groups of sectors. As vulnerable sectors are marked the five sectors which record on average across EU countries the largest negative deviations in cumulative GDP growth deviation from the starting point in the adverse scenario. These sectors, ordered in terms of cumulative growth from the starting point are the Manufacturing (C), Transportation and storage (H), Mining and quarrying (B), Agriculture, forestry and fishing (A), and Wholesale and retail trade (G).

Apart from the scenario, losses also reflect portfolio characteristics. Sectoral exposures with the highest NPE ratios at the starting point tend to record a larger increase of NPEs and higher loss rates over the adverse scenario (Figure 27). Thus, vulnerabilities at the starting point can magnify the effect of the adverse scenario.

Source: 2025 EU-wide stress test data and EBA calculations

Note: The NPE (stage 3) cumulative change is the ratio of the cumulative increase in the NPE (stage 3) exposures over the adverse scenario horizon divided by performing exposures at the starting point. The loss rate is calculated as the change in the stock of provisions between the end of the adverse scenario horizon and the starting point divided by total exposure (performing and non-performing) at the starting point. High NPE sectors are defined as follows. For all country and sector combinations reported by banks in the stress test sample the aggregate NPE ratio is calculated as the share of aggregate stage 3 exposure to the aggregate total exposure for this country and sector segment at end 2024. As high NPE segments are flagged the segments, at the country and sector level, which record aggregate NPE ratio above the 75th percentile.

The sectoral break-down of corporate credit loss projections provides valuable insights and allows a targeted assessment of potential vulnerabilities in banks’ NFC exposures. In addition, the sectoral breakdowns requirements encourage banks to continue developing their capabilities for collecting, aggregating, and analysing granular data for their borrowers to analyse novel risks. In fact, insights from the 2025 EU-wide stress test data reveal that banks have made progress in differentiating the impact of the adverse scenario narrative across sectors. Projections show a higher sensitivity to the adverse macroeconomic scenario compared to the 2023 EU-wide stress test.

Nevertheless, banks’ modelling efforts should continue to advance. The additional information provided with the sectoral projections shows that banks make limited use of models or sectoral sensitivities to project PD and LGD parameters. The number of banks which employ models for PD or LGD varies across sectors, and the use of models is less pronounced for the LGD parameters. On average, 15 banks per sector (out of 64 banks in the sample) model PD parameters for on average more than 50% of their exposures per sector, while only on average 12 banks per sector report the use of statistical models for the LGD for on average more than 50% of their exposures per sector (Figure 28). The limited use of models can be observed across sectors regardless of their size or credit quality.

Source: 2025 EU-wide stress test data and EBA calculations

Note: The chart shows the banks in the stress test sample which model on average at least 50% of the exposures of each sector on average across countries of exposure. For each bank the average modelling share is calculated by sector by averaging the share of exposures to which models are employed across countries of exposure. This calculation is performed separately for the PD and LGD models. A bank is marked as having models for a given sector if the resulted average modelling share across countries is at least 50%.

The quality of projections matters for understanding sectoral vulnerabilities to various scenario narratives. The submitted projections reveal that the banks which make a greater use of models for PD and LGD parameters tend to project, on aggregate, higher loss rates for the vulnerable sectors (Figure 29). Hence, banks should continue their efforts towards improving their modelling capabilities. In deploying efforts to improve sectoral projections, institutions are invited to take a sequential approach, where the roll-over of models should be implemented by first prioritising those sectors where they hold the largest share of exposures, or with weaker credit quality.

Source: 2025 EU-wide stress test data and EBA calculations

Note: The chart shows the projected loss rates over the adverse scenario for two groups of sectors and banks. Vulnerable sectors are marked the five sectors which record on average across EU countries the largest negative deviations in cumulative GDP growth deviation from the starting point in the adverse scenario. These sectors, ordered in terms of cumulative growth from the starting point are the Manufacturing (C), Transportation and storage (H), Mining and quarrying (B), Agriculture, forestry and fishing (A), and Wholesale and retail trade (G). Banks with models are these banks which use statistical models for projecting sectoral PD and LGD for at least 50% of their exposures, on average.

Market risk

Market risk instruments are assessed under the assumption that all adverse market movements occur immediately, with no recovery over time (instantaneous shock). In addition to valuation impacts on the fair value of financial instruments, the methodology considers client-driven income[39], which comes from bank’s capacity to generate revenues through market making activity. Losses on financial instruments held at fair value are not only recognised in banks’ P&L statements but also in capital, through other comprehensive income (OCI).

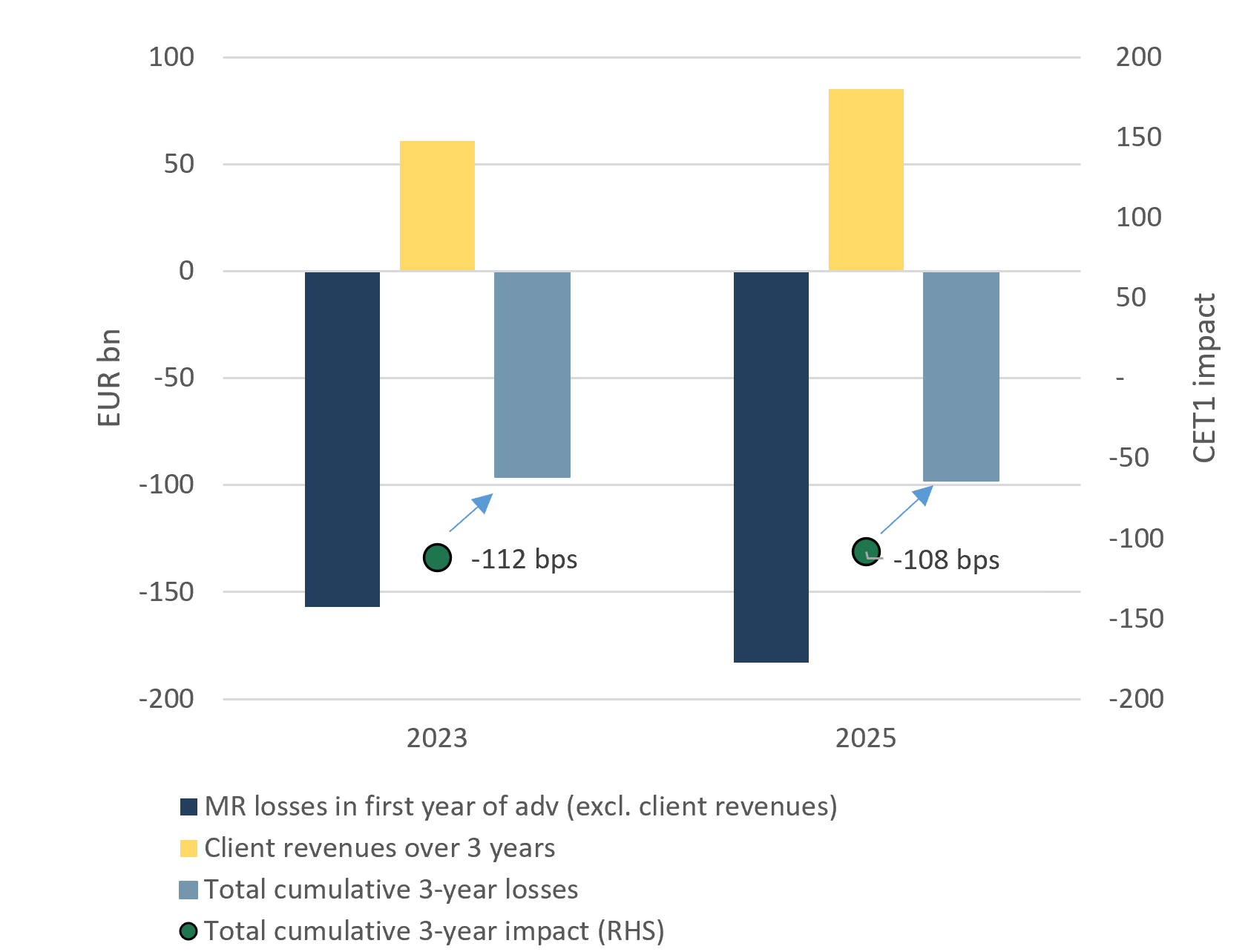

Market risk immediate losses to positions valued at fair value, i.e., those stemming from an instantaneous shock in the first year of the adverse scenario, total EUR 183 bn (-203 bps impact on the aggregate CET1 ratio). Banks’ ability to generate income on market risk activities even under crisis periods, for example as fees on market making or trading activities on behalf of external clients, is also considered in the exercise. When accounting for the positive contribution of these revenues in the three years of the adverse scenario, cumulative 3-year losses reach EUR 98 bn, corresponding to a CET1 capital depletion of 108 bps.

Compared to the 2023 stress test, immediate losses are 16% higher in the 2025 exercise. However, the total 3-year cumulative impact in the two exercises is almost the same (-112 bps in 2023 vs -108 bps in 2025), as shown in Figure 30. This is due to the higher positive contribution of client revenues in 2025, accounting for +95 bps impact on CET1 capital on a cumulative basis (compared to +71 bps in the previous stress test), driven by smaller market risk shocks in the adverse scenario[40] in 2025 and by some methodological changes[41].

Figure 30: Evolution of market risk losses and income contribution in the 2023 and 2025 EU-wide stress test (EUR bn) and related impact on CET1 ratio (bps) under the adverse scenario (RHS)

Source: 2025 and 2023 EU-wide stress test data and EBA calculations [DOWNLOAD DATA]

Note: The bars in the chart show respectively the market risk immediate losses (i.e., those occurring in the first year of the adverse scenario), the income contribution (client revenues) and the total market risk cumulative losses over the 3 years of the adverse scenario. The dot shows the impact on CET1 ratio (bps) of the total market risk cumulative losses (i.e., last bar) over the 3 years of the adverse scenario.

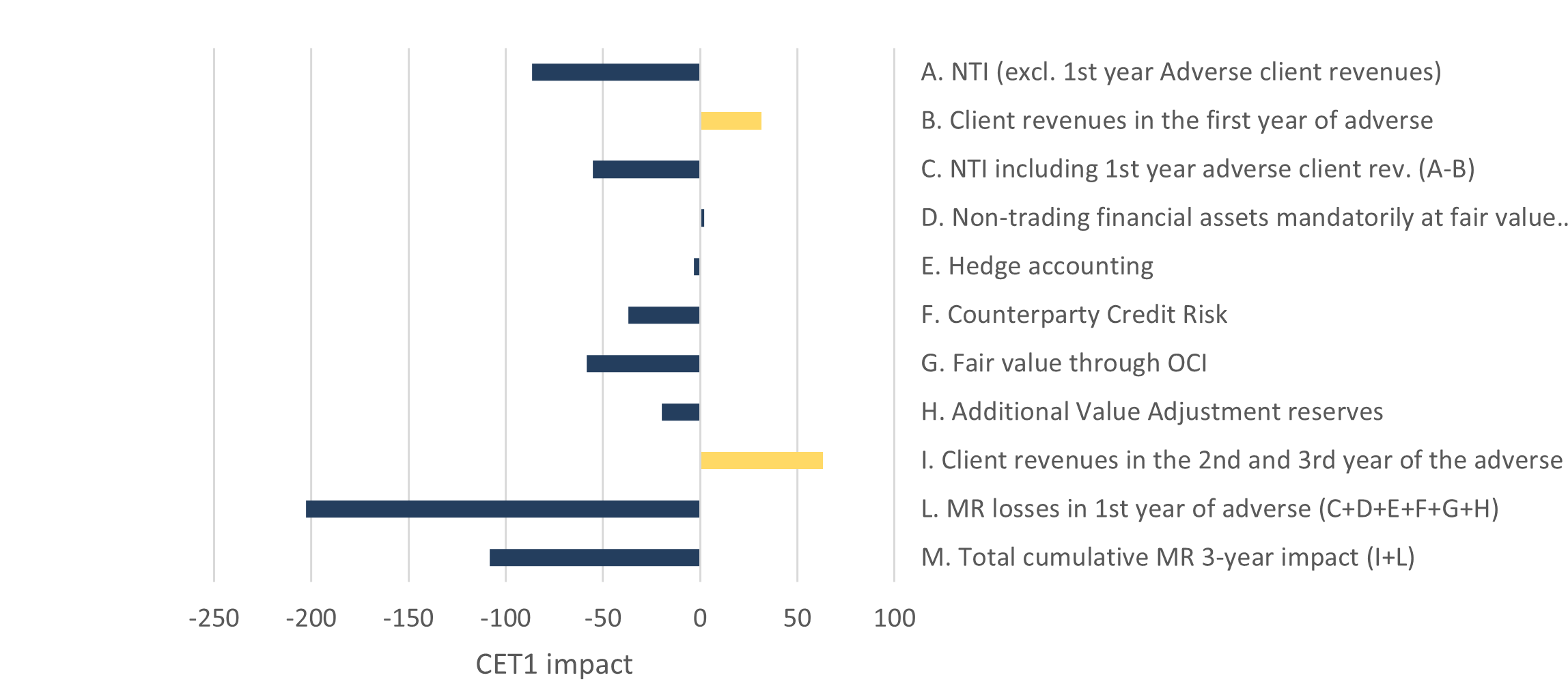

Most of the market risk losses (Figure 31) steam from net trading income (NTI)[42] (EUR 78 bn losses without client revenues, -86 bps impact on the aggregate CET1 ratio), from instruments recognised at fair value through other comprehensive income (FVOCI) (EUR 52 bn losses, -58 bps) and from counterparty credit risk (CCR) (EUR 33 bn losses, -37 bps).

Figure 31: Contribution to capital ratio of main market risk items (bps)

Source: 2025 EU-wide stress test data and EBA calculations [DOWNLOAD DATA]

Note: The chart shows the impact on the CET1 ratio (bps) for each component of the market risk methodology, under the adverse scenario. It starts from the first year NTI impact, with and without client revenues (C and A) and it adds the different components (D, E, F, G and H) to compute the impact on CET1 ratio in the first year of the adverse scenario (L). Finally, it shows the cumulative 3-year impact on CET1 ratio (M) by adding the client revenues impact from the second and third year of the adverse scenario to the first-year losses (L). The positive contribution of income components (I and B) is shown in yellow.

Banks with significant market risk exposures (Comprehensive Approach Advanced – CA-adv)[43] report higher immediate losses than the others (i.e., Comprehensive Approach – CA banks, and Trading Exemption – TE banks) in the first year of the adverse scenario. The main drivers of these losses are counterparty credit risk (CCR), additional value adjustment (AVA) reserves[44], and instruments valued at fair value through profit or loss (FVPL). However, CA-adv banks’ strong income generation from market-making activities, enables them to offset up to 80% of total losses—significantly more than other banks (Figure 32). Banks with moderate market risk exposure (CA) and banks with marginal market risk exposure (TE banks) mitigate immediate losses by 33% and 5% respectively. For TE banks, the main driver of losses is OCI, largely driven by their exposure to debt securities (see also Box 5).

Source: 2025 EU-wide stress test data and EBA calculations

Note: The chart shows the share of immediate market risk losses (i.e., those materialising in the first year of the adverse scenario) for each bank exposure cluster (TE, CA and CA-adv) as defined in the market risk stress test methodology and for the full sample (‘all banks’). It also shows the income from client revenues over the 3-year of the adverse scenario as a share of immediate market risk losses.

Overall, under the 3-year adverse scenario, the cumulative CET1 capital depletion varies notably across banks (Figure 33). While banks with moderate (CA) and low (TE) market risk exposures see reductions of 131 bps and 112 bps respectively, banks with high market risk exposures (CA-adv) experience the smallest impact, with a depletion of 60 bps. The capacity to generate client revenues also explains the greater dispersion in the three-year cumulative impact among CA-adv banks. While some still experience substantial losses, others are able to fully counteract the adverse shocks and even report positive results over the horizon—leading to a wide distribution of outcomes.

Source: 2025 EU-wide stress test data and EBA calculations

Note: the boxplots show the 5th,25th, 50th (median), 75th,95th percentile and the weighted average (red-dotted line) of the cumulative CET1 impact at bank level. The percentiles are computed for each bank exposure cluster (TE, CA and CA-adv) as defined in the market risk stress test methodology ad for the full sample (‘all banks’). For the weighted average, banks’ total REA (transitional) at the end of 2024, restated under CRR3 rules, were used as weights.

When examining risk factors’ contribution to market risk losses, credit spreads are the main driver, accounting for nearly 45% of losses. Their impact is even more pronounced for banks with relatively higher market risk exposures, where they reach nearly 60%. In contrast, for the other banks (TE and CA), losses are more evenly distributed. Shocks for interest rates, equity prices and funds have similar contribution to market risk losses on aggregate (Figure 34).

Source: 2025 EU-wide stress test data and EBA calculations

Note: Risk factors’ contribution to market risk losses on Held-for-trading (HfT), hedge accounting, FVOCI and FVPL positions in the first year of the adverse scenario. The computation is done for each bank exposure cluster (TE, CA and CA-adv) as defined in the market risk stress test methodology and for the full sample (‘all banks’).

|

Operational risk

The total operational risk losses under the adverse scenario amounts to EUR 54.8 bn, with a negative impact on EU banks’ aggregate CET1 capital ratio of 61 bps. These overall losses are above historical levels and in line with the previous stress test, where losses stood at EUR 53 bn (-62 bps in terms of capital impact). Operational risk assesses financial losses arising from banks' (mis)conduct, such as providing services to sanctioned entities, and other operational risks, like for example the failure of payment systems.

The losses are projected to be quite evenly distributed across the three-year horizon, with the highest losses of EUR 19.5 bn anticipated in the first year (Figure 36). These losses are primarily driven by other operational risk losses, which increase significantly compared to conduct risk losses. The total losses are above average historical figures, however, in the past three years, total operational risk losses were mainly driven by material conduct risk cases instead, with total reported levels of EUR 9.3 bn in 2024.

Banks expect losses coming from material conduct issues to decrease in the near future. It should be noted that material conduct losses are non-uniform in nature and lack a common systemic link, with losses varying significantly over time and, therefore, are difficult to estimate. Throughout the adverse scenario of this stress test, according to banks' projections, these losses amount to EUR 20.3 bn, which is slightly below the losses in the past three years. On the other hand, the losses from smaller non-material cases that are easier to project amounted to EUR 10 bn for the 3-year horizon, significantly above the historical average.

Source: 2025 EU-wide stress test data and EBA calculations

Source: 2025 EU-wide stress test data and EBA calculations

Note: Both charts look at evolution of operational risk losses. 2018-2023 data represent the actual reported numbers, where years marked with a star (*) are based on the 2023 EU-wide stress test sample. All 2025-2027 numbers are projections. The left chart shows the composition of operational risk losses, distinguishing between material and non-material conduct, and other operational risk losses. The right chart compares the actual figures and projections in the baseline and adverse scenario, including those from the 2023 EU-wide stress test.

The higher other operational risk losses can be attributed to the narrative where, amid escalating geopolitical tensions, a marked increase in the number and frequency of cyberattacks would be expected creating operational vulnerabilities for banks. Other operational risk losses increase from EUR 4.4 bn in 2024 to projected EUR 8.4 bn in 2025, totalling EUR 24.5 bn across the three-year horizon of the exercise.

Learning from previous exercises and looking at the baseline scenario, banks generally project losses accurately for the first year, while larger discrepancies may occur in subsequent years, mainly due to the aforementioned difficulty to project the historically inconsistent material conduct risk losses (see 2023 projections in Figure 36, right chart).

Risk exposure amounts

The depletion in the aggregate CET1 ratio under the adverse scenario mostly results from the impact to banks’ CET1 capital of the stressed earnings and increased losses described in section 4 (i.e. a decrease in the numerator of the CET1 ratio), together with a projected increase in the denominator of the CET1 ratio, the total risk exposure amount (REA).

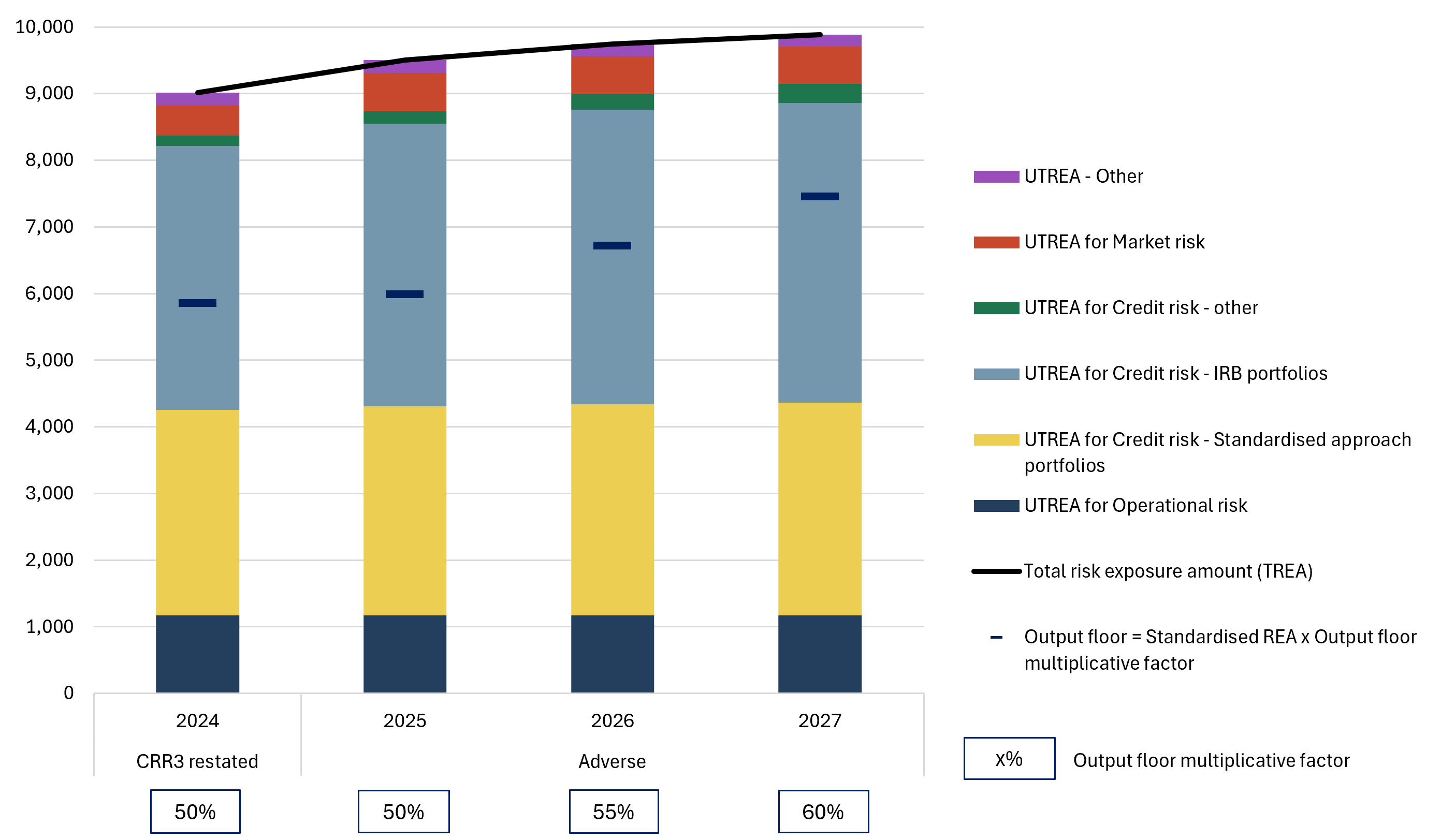

Total unfloored risk exposure amount (UTREA) measured under CRR3 amounts to EUR 9,017 bn at the start of the exercise (Figure 37). Over the three years of the horizon, the adverse scenario pushes the UTREA to EUR 9,882 bn, resulting in a 9.6% increase from the starting point. More than half of this increase is driven by the change in credit risk exposures for IRB portfolios (+ EUR 538 bn). The total unfloored market risk exposure amount increases by EUR 106 bn, while the operational risk exposure amount remains constant over the horizon because of the static balance sheet assumption.

The output floor does not bind any bank in the sample over the 3 years stress test horizon, on a transitional basis. Hence, no additional REA amount is attributable to the application of the output floor. This is explained by the progressive phase-in of the output floor, please refer to section 2.4. Under a fully loaded basis, with the implementation of the 72.5% multiplicative factor and the removal of all CRR3 transitional arrangements, the total risk exposure amount would be significantly larger since the output floor would in this case bind for several banks in the sample. This additional layer of REA due to the output floor would already bind at the end-2024 starting point (restated under CRR3 rules).

Figure 37: Evolution of unfloored total risk exposure amount (UTREA), output floor and total risk exposure amount (TREA) under the adverse scenario (in EUR bn)

Source: 2025 EU-wide stress test data and EBA calculations [DOWLOAD DATA]

Conclusions

The results of the 2025 EU-wide stress test indicate that the largest EU banks would be resilient to a severe but plausible hypothetical stress scenario and would have the capacity to continue to support the EU economy in stressed times. The scenario incorporates a sharp deterioration in the global macro-financial environment, driven by escalating geopolitical conflicts, particularly in the Middle East, and a rise in protectionist trade policies worldwide, including tariffs. The scenario remains relevant, and it is substantially more severe than the recent macroeconomic developments.

The EU banking sector has further improved in terms of profitability and capital ratios in the past two years, which has cushioned the impact of the severe scenario. While banks are more risk-sensitive to changes in the scenario demonstrating higher nominal losses, they have a better loss absorption capacity through income generation. For this stress test, starting point NII is at a high level and despite the sizeable impact of the scenario, it remains robust. Nevertheless, it is expected that, going forward, the loss absorption capacity coming from NII will decline as banks net interest margins will normalise from high levels. Stress tests over the past three cycles show that persistently low interest rates are more damaging to banks’ NII than sharp rate hikes[46].

Banks are more vulnerable in certain risk areas. Not surprisingly, the largest losses come from credit risk. However, in this year’s exercise they are notably higher compared to the 2023 exercise. Similarly, losses from market activities are much higher compared to the previous stress test, if it was not for banks’ client revenues generation capacity, which offset almost half of these losses. Higher nominal credit risk losses result mainly from banks’ less favourable starting points, especially higher stage 2 loans in credit risk.

Trade and energy intensive sectors are affected more by the scenario. This year’s adverse scenario assumes increasing energy and commodity prices, as well as, heightened trade tensions, which are reflected in increased trade barriers (tariffs). Such scenario has a more pronounced impact on economic sectors that are more energy-intense and use raw materials and commodities as input, as well as those sectors that depend significantly on international trade. For these sectors which are impacted more by the scenario, such as manufacturing and agriculture, loss rates are higher compared to other sectors. For more domestically focused exposures, asset quality is driven by the general downturn in economic activity and asset prices, like the real estate and construction sectors.